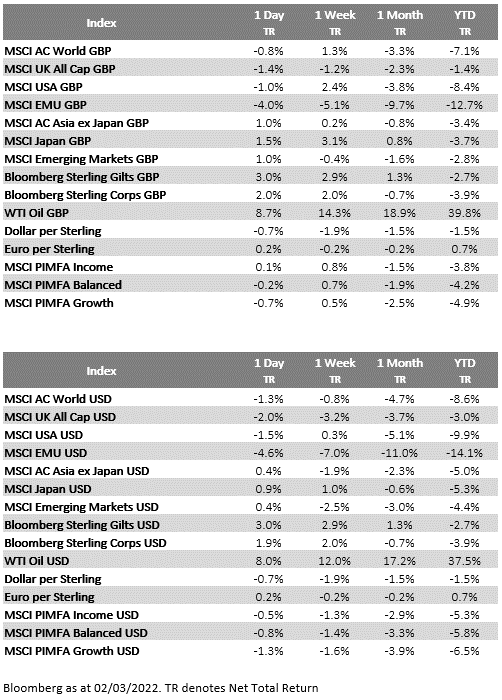

Please see article below from Invesco received late yesterday afternoon – 03/03/2022.

Henley European Equities Team Our thoughts on the Ukraine/Russia conflict – February 2022

• The immediate equity market reaction to the Russian invasion last Thursday was risk off.

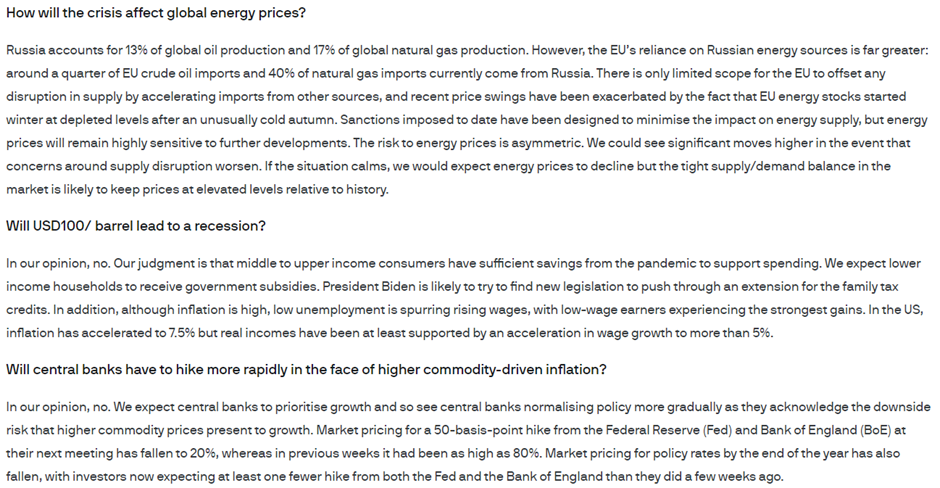

• There have clearly been inflationary shocks, and so we expect increasing pressure on the ECB to act.

• The introduction of new sanctions over the weekend, namely excluding several Russian banks from SWIFT and restricting the Russian Central bank access to some of their international reserves, has caused a fresh bout of volatility impacting the banking sector in Europe.

How the market responded to rising tensions last week

The immediate equity market reaction to the Russian invasion last Thursday was ‘risk off’. ‘Risk off’ meaning, understandably, selling business with direct exposure to Russia and pending sanctions. However, it also meant selling banks and cyclicals more generally.

When the market has been shocked in recent years: Brexit, Trump, Covid and now Putin, share price reactions are Pavlovian. Banks are financially leveraged and cyclically exposed, so they sell-off with ‘risk-off’, and then quickly the market backfills the fundamental rationale.

Yesterday, the explanation was the risk of slower growth but also less rate potential. And so, whilst banks sold off, long duration equities (‘Quality and Growth’) performed strongly. The risk of higher rates being off the table was fuelled by ECB member Holzmann being quoted as having said, “Ukraine conflict may delay stimulus exit”.

But what he actually said was, “It’s clear that we’re moving toward normalizing monetary policy, it’s possible however that the speed may now be somewhat delayed.” The context of which being that he gave a hawkish speech on Wednesday, and then was asked for an update in the wake of the shocking news of Thursday’s invasion.

What’s undisputable is that looking at the market behaviour, investors were clearly more emboldened post his comments to buy more duration equities as a result.

Is this the right reaction?

We believe this reaction may be short lived. Whilst there is a long list of unknowns resulting from Russian actions this week, one of the few likelihoods is yet more inflationary pressure. Our basic point is ‘transitory inflation’ becomes plain old inflation with longevity and actions in Eastern Europe have again pushed commodity prices higher.

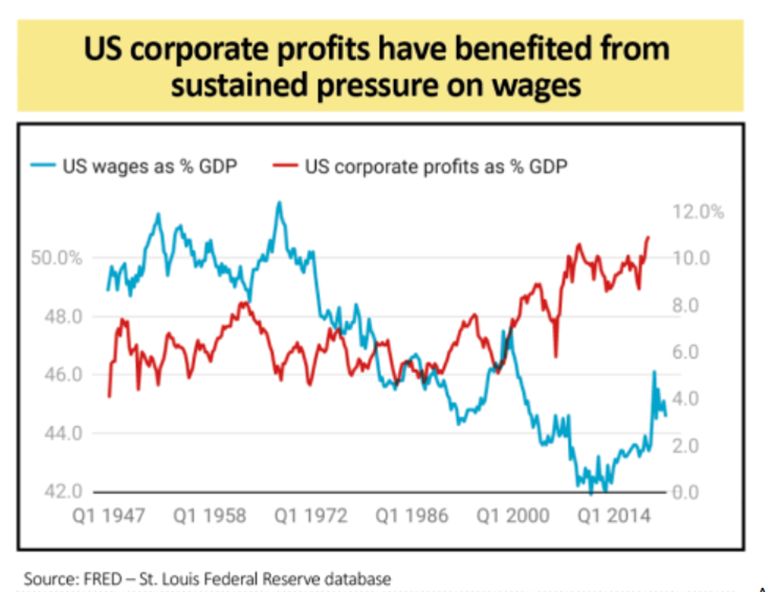

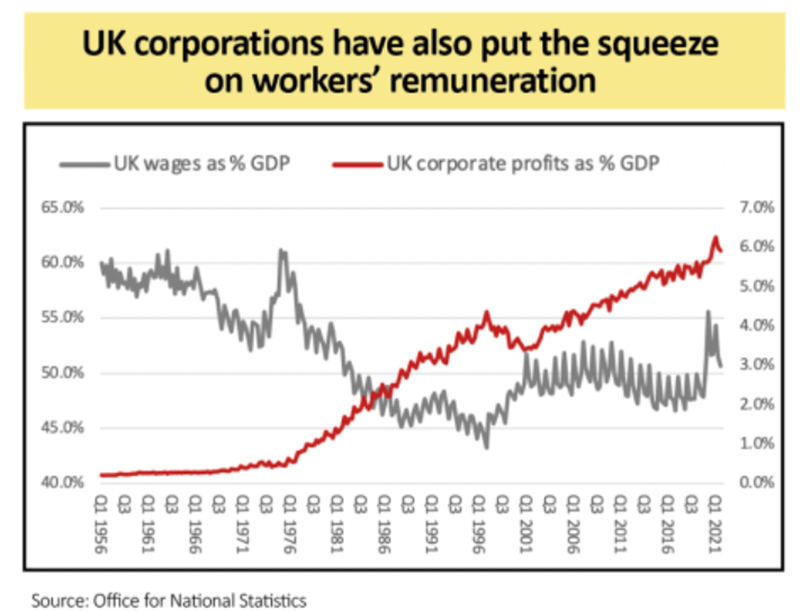

Ahead of the conflict ECB policy was set based on inflation returning to below trend (<2%) in 2023, however, to our minds the assumptions left no more room for inflationary shocks. Given our belief EU wages have upside risk to the ECB’s 3% (and now events in Ukraine), there have clearly been inflationary shocks. So, we expect increasing pressure on the ECB to act: European monetary policy remains a risk to the upside.

Need to think about duration and beta

As we’ve mentioned in previous comments, the impact of higher interest rates is a risk to the valuation of the more expensive parts of the market: European Quality.

Of course, the impact of the Ukraine crisis is also a threat to growth rates – and that impacts cyclicals. Hence, simply buying the ‘Value’ factor becomes more challenging after this week also. We believe the solution lies not in two dimensions of ‘Value vs Growth’, but rather the third dimension of ‘High vs Low Beta’. Whilst we remain nervous of the crowded positioning in high beta Quality (e.g. Technology, Payments, Luxury), where valuations are high, we think there are areas of defensiveness at reasonable valuations: Telecoms, Insurance, Food Retail, Big Pharma and Utilities.

We believe these are the areas to transfer risk to this week and note they sit within the Value factor buckets. Within cyclical value there remain some pockets of defensiveness to the specifics of this week through exposure to Oil and Resources. Where we are incrementally more cautious is consumer discretionary.

The need for a balanced portfolio

Our conclusion is we think balance is key. We think being heavily skewed to the red quartile is risky. Our debate is our weighting to the top half and how much events of this week mean we should move to the low beta side of the allocation.

How to think about banks given the financial sanctions introduced this weekend

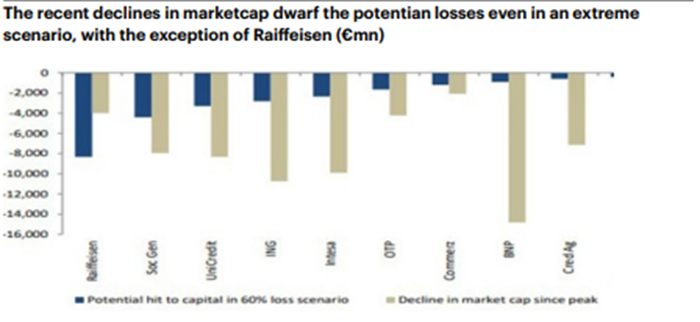

The introduction of new sanctions over the weekend, namely excluding several Russian banks from SWIFT and restricting the Russian Central bank access to some of their international reserves, has caused a fresh bout of volatility impacting the banking sector in particular. In the following paragraphs and charts we provide our thoughts on the market’s reaction.

The below chart is from financials specialist research house, Autonomous. They have used the Russian debt crisis in 98 as the basis for impacts when banks lost 60% of their exposures. Note since the late 90s, EU banks exposures to Russia are smaller with, for example, French banks 11% exposed vs 35%. We should also note that assuming 60% of assets are gone is a worse outcome vs walking away from the region – handing Russia back the keys to the assets. However, in this effectively worst-case scenario you can see how much market cap has already been destroyed vs exposure.

Another key point to think about with EU banks is they are long provisions today. Remember, due to the Covid uncertainty, EU banks provisioned their risks aggressively and thankfully because of the extreme fiscal and monetary measures taken, these provisions look overstated. That means banks have a stock of provisions they could be releasing – which can now be redeployed to Russian exposure and thereby absorbing losses for shareholders.

From the list above, the bank with largest risk to Russia is UniCredit. Whilst there is headline risk, we note UniCredit is holding 1yr of normalised provisions in precautionary provisions today (scope 1 & 2). In earnings terms Russia is c3-5% of group only and the assets are well capitalised (18.8% CET1 vs 10% required). Using a 1998 losses analysis means a loss of 90bps CET1 however, walk-away and that loss is estimated at -50bps only (given this would also reduce RWA). This compares to last reported CET1 of 14.1% and co target of 12.5-13% so they have the means to absorb a worst case scenario without fresh equity: this is not a repeat of the GFC.

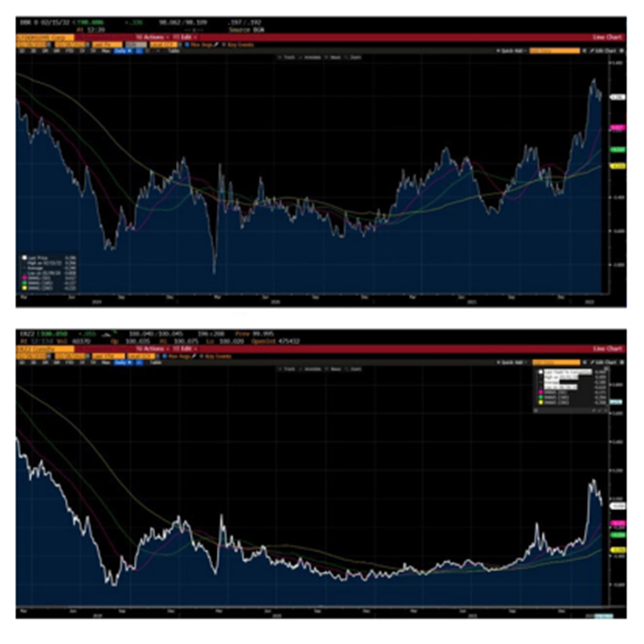

To that point it’s worth highlighting what’s happening in the debt markets vs equity. German 10Y bond yields have moved lower, but as per the chart below we’re at +20bps yield today vs -40/-60bps for much of 2021. Likewise the 3month Euribor (second below) is far from 2021 levels which is where the European banks have retrenched back to.

Please continue to check back for our latest blog posts and updates.

Charlotte Clarke

04/03/2022