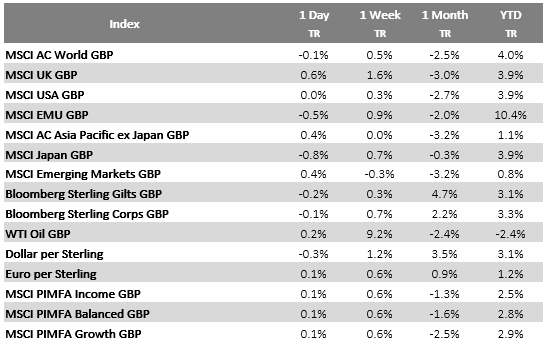

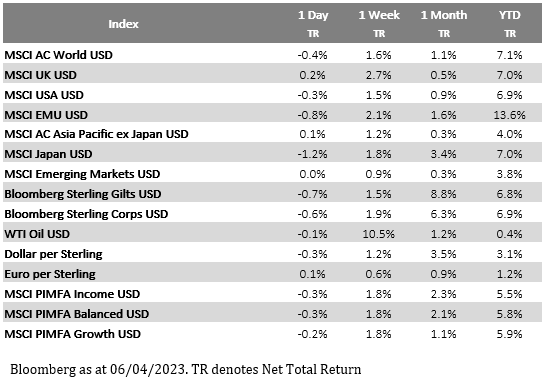

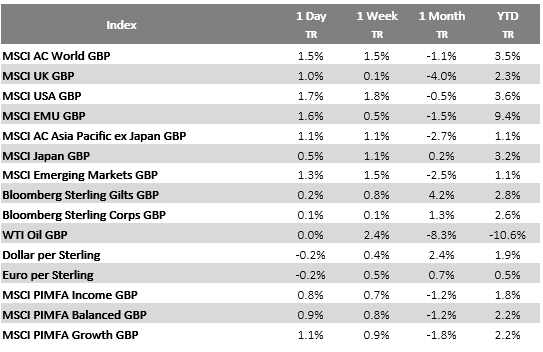

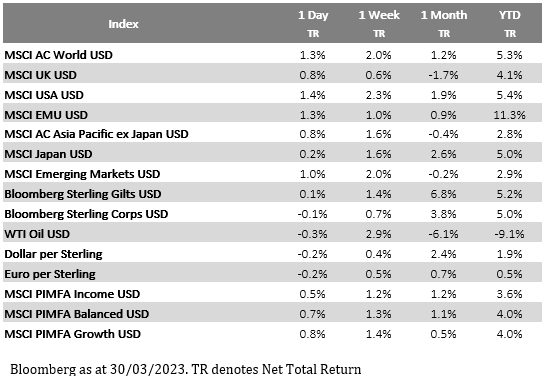

Please see below and article received from EPIC Investment Partners this morning (12/04/2023), which summarises their views on the International Monetary Fund (IMF) recently revised forecasts for the UK economy and predictions for other global economies:

The Daily Update: IMF Growth Forecasts

Yesterday (11/04) the International Monetary Fund (IMF) upgraded its outlook for the UK economy, saying it now believes Britain is on track to contract by 0.3% this year, half the 0.6% decline the IMF forecast in January, then expand by 1% in 2024. However, that’s where the good news ends for Blighty, as the IMF believes we will still be the worst-performing large economy on the planet this year. Only Germany will be the other advanced nation to see negative growth this year, and that is by just 0.1%.

So much for Chancellor Jeremy Hunt’s view that the “the declinists are wrong, and the optimists are right” about the UK’s economic prospects. Not that he sees anything wrong in that statement. “Thanks to the steps we have taken, the OBR says the UK will avoid recession, and our IMF growth forecasts have been upgraded by more than any other G7 country,” he said. As they say, torture the statistics long enough and eventually they’ll confess.

Overall, the IMF downgraded its forecast for global growth by a small margin of 0.1% from its 2.9% projection in January, lower than the 3.4% seen last year, with a slight recovery next year to 3%. However, there is a 25% chance that global growth will fall below 2% for the first time since the 2008-09 global financial crisis, more than double the normal odds.

The Fund’s chief economist Pierre-Olivier Gourinchas said the global economy was at risk of a hard landing, pointing to governments and central banks being behind the curve on getting the inflation genie back in the bottle whilst avoiding slamming the brakes on growth and employment. “We are entering a perilous phase during which economic growth remains low by historical standards and financial risks have risen, yet inflation has not yet decisively turned the corner”, he said.

Advanced economies are now projected to grow by 1.3% this year and 1.4% in 2024. Within the G7, the US leads the way with an expansion of 1.6% in 2023 and 1.1% in 2024. Canada is eyed at 1.5% for both this year and next, with Japan following with estimates of 1.3% and 1% respectively. After growing 3.5% last year, the EU is viewed as growing 0.8% and 1.4%.

Away from the G7, emerging markets and developing economies are forecast to grow 3.9% this year after a growth of 4% last year and 4.2% next year. China’s forecast came in at 5.2% and 4.5% with India leading the way at 5.9% and 6.3%. Russia’s economy contracted 2.1% last year, however the IMF believes it will recover most of that contraction with 0.7% growth this year and 1.3% in 2023.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Carl Mitchell – Dip PFS

Independent Financial Adviser

12/04/2023