Please see below ‘Markets in a Minute’ article from Brewin Dolphin commenting on the latest stock market movements. Received late yesterday afternoon – 11/07/2023.

Please check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see the below economic review of Q2 from Brewin Dolphin received last night:

Please continue to check out Blog content for advice and planning issues and the latest investment markets and economic updates from leading investment houses.

Please see below, a ‘Monday Digest’ from Tatton Investment Management discussing the key economic news from the past week. Received this morning – 19/06/2023:

Overview: Market conundrums amid volatile growth

Equity markets moved higher last week, despite central bank hawkishness. We had another 0.25% rate rise from the European Central Bank (ECB) and, although the US Federal Open markets Committee (FOMC) left rates unchanged, they gave us and through their ‘dots plot’ they gave us strong hints of at least another 0.25% hike in July. They also indicated their expectation for rates to stay higher for longer.

Since 23 March the date of the last FOMC meeting, the S&P 500 has gained 10%. The backdrop to that last meeting was the Silicon Valley Bank collapse, when many thought the financial system was close to a dangerous precipice, and that a rash of corporate bankruptcies were just moments away. We have made great strides since then. But the west’s continued growth is not assured, precisely because central banks still have more work to do to quell second-round inflation pressures from the self-enforcing dynamics of wage rises. The Fed and the ECB told us that last week, and this week, the Bank of England (BoE) will most certainly raise UK rates. Yet, as we said earlier, markets appear to be behaving as if growth is set to rise sharply, despite institutional investor sentiment surveys showing only a little improvement in confidence.

We noted how expensive equity markets had become in May and, since then, it has become more extreme. The S&P 500 is now 28% more expensive than our historical model of earnings and yields would suggest, a level that has not occurred in over 20 years. Such optimism is only justifiable if we are moving into a significantly higher real growth and inflation environment, as was the case during the second half of the 20th century. For this to happen, Oone would have to think that central banks will give up on constraining inflation to their targets through higher rates in the medium term, a judgement we think is still way too early to make now.

Have we already reached ‘peak oil’?

Oil prices took another step down in the early part of last week, as Brent crude, the international oil benchmark, dropped to just $71 per barrel (pb) during Monday trading and despite a slight mid-week recovery, prices ended the week below where they were a week ago. After peaking at more than $110pb in June 2022, oil demand has severely weakened and prices have consistently fallen, only occasionally punctuated by sputtering short-term relief rallies. Since the end of last year, Brent prices have been consistently lower than on the eve of Russia’s invasion. Weaker demand is the more important factor, though. Western economies have been slowing for some time. Lately, the biggest disappointment has been China, where which has continued to disappoint over the last few months. Both OPEC and the International Energy Agency (IEA) still expect Chinese oil demand to be a big factor in the second half of 2023, but many market analysts have their doubts.

Underlying the weak demand forecasts is a structural decoupling of economic activity from fossil fuels. While Beijing has pushed environmental policies for a long time, when China has most needed growth its policymakers have generally resorted to energy-intensive sources like industrial production. This year, policy support has been much more focused on less carbon-heavy sources. Moreover, this decoupling is happening across the world – with US and European policymakers pushing hard toward green investment.

On the one hand, you might think – as the IEA seem to suggest – that there is currently overinvestment in oil and gas, which will result in an oversupply when regulatory and societal changes kick in, and potentially an array of stranded assets which could be damaging for the financial system. On the other, you might just think markets do not believe net zero targets will actually be met. Environmental backsliding since the war in Ukraine started (particularly in the UK and Europe), as well as past failures to meet targets, back this up. Neither are comfortable scenarios to be in, but the latter would clearly be worse for the world. As well as the obvious environmental and social crises, extreme weather would likely destroy productive capacity. That is to say, over the long-term, oil demand will have to come down one way or the other – through choice or circumstance. Short-term upsides in the oil price might still be had, but the longer-term pessimism is now definitely in view.

A new sovereign debt regime for emerging markets

The lack of an international bankruptcy regime has plagued developing nations ever since countries started borrowing. However, no international agency or group of countries or group of financial institutions has ever been able to agree a workable framework. Recognition of these troubles is one of the reasons for a pending New York state bill on sovereign debt workouts for emerging market countries (EMs), which was delayed last week. The bill is (unsurprisingly) controversial: defenders point to its ability to streamline lengthy repayment disputes while preventing debts from crushing poorer nations; critics say it will only worsen EM borrowing rates and open up a legal can of worms.

Both sides at least agree that some system of rules is needed for sovereign debt. The most controversial parts of the proposals, though, are measures which limit how much money investors can recoup when a nation defaults. The resulting framework would be very forgiving for borrowing nations – compared to what happens now, at least. Some have even pointed out that governments could unilaterally extend the maturity of their debt without penalty, allowing them to restructure debt repayments without ever officially going into default. That would arguably give issuing nations discretion to decide whether they are in default or not.

EMs are clearly struggling with foreign-denominated debts in the post-pandemic world. It is highly likely Pakistan will officially restructure its debt soon after agreeing terms with the IMF. Meanwhile, Ukraine will need a restructuring in due course. Unfortunately, it is hard to see how these lenient measures would do anything other than move the current problems around.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below article from Brooks Macdonald analysing the potential impact on global equities resulting from the US Federal Reserve’s recent decision to hold interest rates. Received today – 16/06/2023.

Please check out blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see this week’s Tatton Monday Digest discussing the key economic news from the past week:

Overview: disinflation sentiment cheers investors

Last week was another positive one for global stock markets, with the narrative of a soft economic landing in 2023 appearing to gather support. Stock market gains in June have been spreading to the mid and small cap market segments, rather than just for a handful of mega-caps. In the US, the mostly small cap Russell 2000 index has risen about 8%, versus 4% for the mega tech-heavy NASDAQ 100. Europe has also seen similar moves, suggesting investors are gaining confidence that the headwinds to growth are turning towards tailwinds, thereby preventing a recession.

Even emerging markets have started June in a more upbeat fashion, compared to a rather muted May. This should probably be seen as win, given the disappointment around China. The world’s second-largest economy – and by far the biggest component of MSCI’s EM index – has been struggling under the weight of expectation for months now. The anti-climax has induced another policy move by Chinese authorities, this time asking banks to reduce interest payments to depositors and to indicate a round of equity market support. There is plenty of liquidity in China, but depressed investor confidence has made valuations there very cheap, so we may be in for a sharp bounce in Chinese equities should the authorities succeed.

Further China policy easing will be another tailwind, and not just for China. However, until the inflation picture really improves in the developed world, central banks will still feel obligated to keep raising interest rates. Last week, both Canada and Australia surprised markets by both hiking rates another 0.25%. This week it could be the turn of the US Federal Reserve (Fed), with its Open Market Committee meeting on Wednesday. Markets have come to expect another rate rise, if not next week, then in July. For what it’s worth, we are not so sure. May’s payroll survey showed a sharp jump in the number of people employed but was quite downbeat in other areas, and the unemployment rate rose to 3.7%. Another factor that could stay the Fed’s hand is the resumption of US Treasury financing after the debt ceiling resolution. The Fed’s current account must be replenished – by issuing large amounts of short-term government debt at competitive rates – and that could drag money away from those rather stressed US regional banks. After March’s unnerving (and economy damaging) episode, another rate rise now risks worsening the situation and causing a second round of bank failures.

We wrote last week that optimists had gained the upper hand over the pessimists and last week’s market gains tell a similar story. It seems that while markets are never without their worries even the pessimists may find it difficult to be apocalyptic when the sun shines.

Japan’s new rising sun?

Japan is having a moment. Over the last three months, its stock market has been the best performer of all the headline regions we track. In the middle of May, the Topix returned to its highest level since 1989, and in June it has taken another leg up, rallying strongly last Monday and Tuesday in particular. Inflation, something that has been virtually absent in Japan for more than three decades, came in at 3.5% in April – coming down from the 40-year high of 4.3% in January. Many investors, both foreign and domestic, expect wage growth will follow. For these reasons and more, markets are more positive about Japan than they have been for a generation.

Celebrating inflation might sound odd, given western economies are still desperately fighting price increases. But deflation has been one of Japan’s biggest problems during its stagnant period, reinforcing savings habits and holding back investment and growth. Inflation has now been running above the Bank of Japan’s (BoJ) 2.0% target for 13 months. But while these sustained price pressures are extremely unusual in Japan, the 3.5% April figure is hardly a cause for concern. The comparative lack of runaway inflation allows the BoJ much more leeway than its global peers. Its interest rates have stayed anchored below 0%, in sharp contrast to the aggressive tightening seen in the US. Lately there have been signs of a rise in the BoJ’s balance sheet. For foreign investors, this has helped underpin the belief that Japan is a safe haven in a risky world.

Before getting carried away, we note Japan has generated similar hype in the past, only for market rallies to peter out when the economy inevitably disappoints. Current detractors say Japan’s inflation is mostly coming from global factors, rather than domestic price pressures, as well as its cyclical sensitivity. Ties with China have been a positive for Japan in the past, but China’s recently disappointing growth has turned this factor into a negative for now. Some have also argued Japanese profitability is only a consequence of the falling yen value, and not a sign of genuine underlying improvement. But this is an oversimplification, as the rise in profitability is not just linked to exporters, but is broad-based across the whole economy. With the home bias among Japanese consumers, we would not expect this if currency depreciation was the only factor at play.

One could just as well argue it is a positive that Japanese profits have kept up in dollar terms – something that was difficult in the past. Moreover, the fall in the yen will have secondary impacts on Japanese exporters, making their products more attractive. If this continues with domestic corporate improvements and economic optimism – as is the case at the moment – it will only strengthen the case for Japan as an investment destination. Japan always does best when it is outward facing and connected to the global economy. Thankfully, its policymakers now seem to recognise that fact.

Please check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see below article from Waverton investment management discussing financial markets over the last five years. Received today – 08/06/2023.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economics updates from leading investment houses.

Please see below, a ‘Monday Digest’ from Tatton Investment Management discussing the key economic news from the past week. Received this morning – 05/06/2023:

Overview: markets take good news in their stride

In last Tuesday’s digest, we suggested that with the absence of any good news, markets were likely overreacting to the relatively low probability of a US debt default. As it turned out, last week, not only did we get a resolution to the US debt ceiling brinkmanship, but also the welcome news that inflation pressures across Europe were declining faster than expected, while the US jobs market remains paradoxically both vibrant and at the same time showing signs of slowing down (with unemployment going back up). Unsurprisingly stock markets staged a brief relief rally on the debt ceiling resolution, but began wobbling again when Chinese, US and European manufacturing sentiment data showed sure signs of contraction.

On the back of this, bond yields stopped their ascent and declined over the course of the week on the expectation that manufacturing headwinds should persuade central bankers to stop hiking rates. The extraordinarily robust US job market figures on Friday did not appear to change this narrative for bonds, while equities took the strong economic news as outright positive for a change. This came despite expectations for the first rate cut being yet again pushed out further into the future – now only expected for January 2024 (Back in January this year it was implied for the middle of the year).

There is little doubt in our minds that higher rates and higher yields for longer will leave more collateral damage in their wake. But in all, last week was a good one for the optimists, who may well believe equities look more attractive versus bonds again. As to the already seriously expensive US stock market, those same optimists might argue this is mainly driven by companies that will shape our society’s future, and therefore justify the hefty premium. Pessimists, however, will point to the higher-for-longer risks emanating from high interest rates and lending costs eventually driving down demand (and profits), causing a recession-triggering debt default cycle. They might also point out that US tech firms will have to generate almighty profits to justify current valuation hype. Optimists are holding sway just now, but whether it stays this way over the coming weeks remains uncertain. Stay tuned.

The Eurozone is still in an inflation fight

The good mood has excited some investors about Europe’s prospects. Inflation numbers are coming down even more quickly across the continent than had been expected. German inflation fell to 6.3% in May, below the forecast figure of 6.8% and substantially lower than the previous month’s 7.6%. France, meanwhile, saw annual price increases drop to a rate of 6%. For the Eurozone as a whole (6.1% year-on-year), inflation is back to levels seen at the beginning of last year. With some relief we can say that the worst of the European energy crisis is behind us, and surely not a moment too soon. Over time, this should also feed through into wider goods and services to help alleviate second-round price pressures. The European Central Bank (ECB) meeting last month delivered just a 0.25% hike, the smallest of this cycle and a signal that rates are approaching their peak. News that inflation is falling faster than expected increases these expectations, with some investors now predicting the ECB could stop raising rates as soon as July. In any case, the market is pricing in just another 50 basis points from here.

These are certainly encouraging signs, but we should not get ahead of ourselves. While falling energy prices should give the ECB confidence that there is not much more inflation to worry about in manufacturing, services, on the other hand, are showing much more persistent inflationary signs. Strong demand – a rebound from the winter cost-of-living contraction – has allowed service providers to up their prices, and higher wages are being passed on too. The wage factor is a particular concern for the ECB, which considers a cooled labour market the key to taming underlying inflationary pressures, over the long-term at least. In that respect, the signals policymakers really care about – the ‘sticky’ prices – are not as positive as one might imagine from the headline data. This is not to suggest the ECB will follow the BoE’s lead in nailing its hawkish colours to the mast, but merely to point out policymakers will probably be more cautious in believing the hype than some market participants. In particular, due to developments in services and wider labour market concerns, we expect the ECB therefore to sacrifice medium-term economic growth for the sake of continued inflation fighting.

UK’s housing market back under pressure

Britain’s housing market has fared reasonably well over the last year or so, all things considered. However, that resilience is being tested now. Figures released last week showed the number of homes sold in April was 25% lower than a year before, and 8% below the previous month’s figure. Rapid interest rate rises – and the fear of more ahead – are now clearly having a big impact. Earlier in the week, UK lenders pulled out of almost 800 mortgage deals. The number of residential mortgage deals fell by almost 7% in one week alone. Thin volumes often precede falling prices – sometimes sharply – and fewer mortgage offerings dampen the outlook further, almost certainly reducing demand for residential property. So far, the housing market has managed to escape the gloom engulfing most other parts of the UK economy. This is unlikely to remain the case for long.

To make matters worse, it is likely that the impact of rate rises on the housing market will increase over the rest of the year. Around 1.8 million households need to re-mortgage this year, and the majority of those have not yet done so. It is possible some are hoping rates will come down – or at least moderate – as the UK economy worsens. But all the latest communications from the Bank of England suggest they are still extremely concerned about lingering inflation, and are prepared to raise rates further if need be. When those households do re-mortgage, they could find themselves in an even worse situation. Given improved mortgage criteria checks, this should not lead to widespread distressed sales, but it will absorb discretionary spending ability, which will hurt the wider economy.

Structural weaknesses in the UK’s housing supply prevent many building projects and means Britain’s ratio of homes to people is among the lowest in western Europe. This partially explains why prices have been able to grow so dramatically despite increasingly stretched affordability. But while structural imbalances may alleviate downward pressure on prices, they are hardly anything to be pleased about. Like many structural imbalances in the UK, they are ultimately a barrier to long-term prosperity and a sign of deep-rooted challenges. The housing market’s latest malaise is yet another example.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below an article published by Invesco earlier this week which covers their views on how the ongoing negotiations on the US debt ceiling continue to impact on markets and what the potential outcomes are:

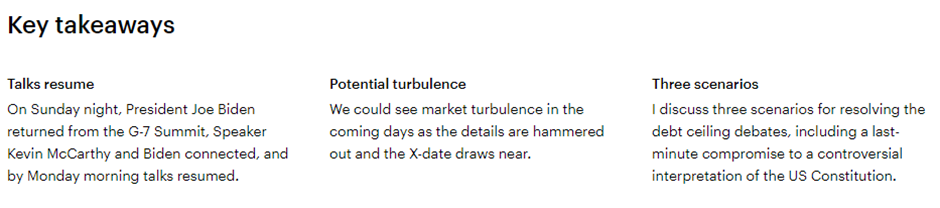

US debt ceiling negotiations are occupying an increasing amount of investor attention as we get closer to the “X-date” — the date that the US government is expected to run out of money to fully meet its financial obligations. Currently, the X-date is estimated to be June 1.

Late last week, the stock market moved from complacency to fervor around the debt ceiling situation – reports that the parties were getting closer to an agreement sent stocks higher. I was skeptical because there seemed to be such a significant gap between the Biden administration’s position and House Republicans’ position. Yes, Democrats and Republicans had agreed to a clawback of COVID-related stimulus that has not been spent yet. And yes, the Democrats had eased their position on work requirements for welfare-related benefits, saying they were open to some requirements. But that was the easy part. The far bigger issue is discretionary spending cuts, where the chasm between Democrats and Republicans is wide.

Both parties agreed to ringfence Social Security and Medicare with no cuts or even caps applied, and only focus on other types of discretionary spending. The Republicans’ bill, passed in April, would reduce discretionary spending to fiscal year (FY) 2022 levels and limit the growth of future spending to 1% annually over the next 10 years. The White House has proposed keeping spending at FY2023 levels into FY2024, but they want the defense discretionary spending to share in some of those cuts. And so my skepticism comes from the wide gap in bargaining positions: Republicans want 10 years of cuts on discretionary spending while Democrats want two years of caps.

And so it is no surprise to me that, in the last several days as the tough decisions on spending get hammered out, the negotiating parties have gotten more pessimistic. It’s just more realistic, in my opinion. And it suggests to me that we’ll see more market turbulence in coming days.

So where do we go from here?

Three scenarios for resolving the debt ceiling debate

Compromise. The most likely scenario is that the two parties arrive at a compromise. That probably wouldn’t happen until the 11th hour, as we have seen in past debt ceiling negotiations. And it will not be easy. In order to meet the X-date deadline, Speaker Kevin McCarthy says a negotiated draft bill must be received by the House Rules Committee by Wednesday the 24th, as it will not be able to receive a vote for 72 hours. After a Saturday vote, the Senate would then have four days to process the bill by regular order. There is a path in the which Senate can process the bill in a condensed timeframe, but that is a narrow strategy and less reliable.

One of the concessions McCarthy made in order to win enough votes to be elected Speaker of the House was restoring the ability for any single member to call for a “no confidence” vote on him. Such a vote would be unlikely to ever unseat McCarthy, but it injects one more possible headache into the negotiating process because there is no cooling off period after a “motion to vacate” vote, so another one can be called the following day, and so on. Suffice it to say it would be very disruptive.

Discharge petition. A second possible scenario is that Democrats utilize a discharge petition to raise the debt ceiling. This is not a layup, however. A discharge petition is a parliamentary procedure to bring a bill out of committee and to the floor for a vote without the committee’s approval to do so. This forces the House to take action on a bill even if the Speaker or the committee it originates from objects. On May 17, House Democratic leadership filed a discharge petition to move a bill for a clean debt ceiling increase out of committee, and 210 Democratic House members signed it. However, Democrats need 218 signatures to force a vote on the floor, which would require some Republicans to sign the petition — and thus far all Republican members of Congress have remained aligned with Speaker McCarthy. And even if Democrats could force a vote, the earliest date that could occur would be June 12 – almost two weeks after estimated X-date.

The 14th amendment. The third possible scenario is that the Biden administration invokes the 14th Amendment — an option they’ve been reluctant to use. The 14th Amendment of the US Constitution states that “the validity of the public debt of the United States, authorized by law…shall not be questioned,” which is widely interpreted to require the US government to meet its financial obligations. The idea here is that the White House and Treasury could decide to keep issuing debt in order to honor past obligations, no matter what happens with the debt ceiling. However, the US Constitution also allocates budgetary power to Congress, not the Executive Branch. Thus, using the 14th Amendment to keep issuing debt would certainly face a legal challenge from Republicans and could get caught in the courts for years. And so it seems the Biden administration is not interested in utilizing this to resolve the debt crisis unless the US arrives at the X-date without the debt ceiling being raised. Another interpretation of the 14th Amendment is that it rules out default, and since it’s part of the Constitution, it stands above the budget law — and this together with the need to maintain financial stability means that the Treasury would have to prioritize debt payments.

News around the world

While the US debt ceiling debate has captivated market observers, there have been plenty of notable developments around the world:

China. April economic data for China came in below expectations. For example, China retail sales rose 18.4% year over year, which was well below consensus.1 And manufacturing-related activity has been disappointing, although that is likely a reflection of the global economic slowdown. It seems that the Chinese economy is continuing to experience significant growth in services activity, but it is not generally as strong as expected. I continue to believe the China re-opening has very long legs – it’s just taking a breather.

Canada. Canada’s Consumer Price Index (CPI) print for April was higher than expected, and modestly higher than March. While it’s moving in the wrong direction, some of that increase can be attributed to the Bank of Canada’s rate hikes, which have driven up mortgage rates and increased the cost of shelter. More importantly, I continue to believe one print does not change the narrative. Canada is in a disinflationary trend; however, it is imperfect and lumpy. I don’t think it should force the Bank of Canada to abandon its conditional pause.

Japan. Japan also saw significant inflation in its most recent CPI print. The good news is that Japan is also experiencing strong growth, as first quarter gross domestic product came in well above expectations. It does beg the question of when the Bank of Japan will get less dovish.

Looking ahead

In terms of investment implications, we are getting conflicting reactions from the stock and bond market. The bond market is pricing in the risk of a technical default, with yields on T-bills maturing in early June rising dramatically. However, the stock market seems far more optimistic, and is not pricing in that risk; even the VIX is relatively low. My read is that the bond market usually errs on the side of greater pessimism while the stock market is often irrepressibly optimistic.

I think the bond market is the more accurate measure of risk right now, and that a brief technical default is a real possibility. Stock markets are likely to reflect that greater risk as we get closer to the X-date without an agreement in place. I just believe a technical default would likely be very brief, as it would provide the impetus for the parties to finally reach an agreement and end the standoff.

And so I have to say that I’m looking forward to reaching mid-June, a time when I feel confident that the debt ceiling impasse should be behind us, one way or another. Perhaps we should think of this spring’s debt ceiling crisis as just a financial form of allergy season: It’s going to get worse before it gets better, and we just need to ride it out until pollen counts go down and we can get back to normalcy. I think we’ll all be able to exhale by mid-June, although it will likely be an increasingly volatile market environment between now and then.

Once that drama recedes, I think all eyes will be back on central banks. I’m optimistic that the US Federal Reserve and the Bank of Canada will maintain conditional pauses, and that other Western developed central banks will draw closer to the end of their respective tightening cycles. I think markets will soon begin to discount an economic recovery, even though sentiment is very pessimistic right now.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below Brooks Macdonald’s Daily Investment Bulletin, received today – 18/05/2023.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.