Please see investment bulletin below from Brooks Macdonald received this afternoon – 04/02/2021

What has happened

After a volatile week where vaccine news varied and retail trades in specific stocks raised concerns of bubbles, global equities had a relatively quiet day. Risk sentiment was helped with growing expectations that former ECB President Draghi would succeed in forming a government and this heralded a significant outperformance from both Italian bonds and the Italian equities index.

Stimulus update

US Treasury yields continued their rally yesterday with the 10-year nudging up to 1.137% as expectations for stimulus increased and therefore expectations for, on the margin, higher inflation and higher interest rates down the line. President Biden told House Democrats that his concern was that the next round of stimulus would risk under-stimulating rather than over-stimulating the economy. This comes as Democrats have opened budget reconciliation measures to put pressure on Senate Republicans to revise their stimulus proposals. Biden’s comments suggest that should the Democrats be forced to the use the reconciliation process, knowing that this is probably their only chance for significant stimulus in 2021, they may increase the size of the stimulus. Despite the relatively quiet market at an index level, these comments helped support cyclical equities, which were previously out of favour due to the mixed COVID narrative, with Energy and Banks performing strongly.

European inflation

Inflation data from the Euro Area surprised to the upside yesterday with headline inflation up 0.9% year on year (vs 0.6% expected) and core inflation up 1.4% (against 0.9% expected). This brings an end to the deflationary period that the Euro area has been experiencing for more than half a year, but this data did support a pro-cyclical tilt to yesterday’s markets. This surprise pick-up in inflation led to the market revising expectations of future inflation levels with the 5y5y (expectations of 5-year average inflation levels in 5 years’ time) up to 1.38%, the highest level since the pandemic begun.

What does Brooks Macdonald think

We would be wary of reading an excessive amount into the inflation data from the Euro Area yesterday. There are some specific factors at play here such as the end of a temporary VAT cut in Germany and equally 0.9% headline inflation is not a particularly exciting number. Looking forward we see COVID as having created a significant output gap due to higher unemployment rates, indeed in some countries stimulus measures have masked the true level of unemployment. Until there is active competition for labour driven by fuller employment, wage inflation will remain subdued and that should calm expectations of a rapid and sustained rise in inflation above the ECB’s target.

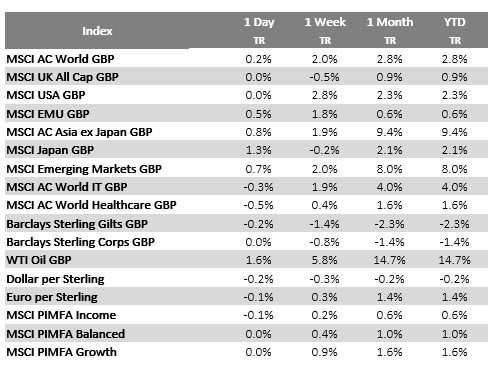

Source: Bloomberg as at 04/02/2021

Please continue to check back for our latest updates and blog posts.

Charlotte Ennis

04/02/2021