Please see today’s Daily Investment Bulletin from Brooks Macdonald detailing their discussions on global markets:

What has happened?

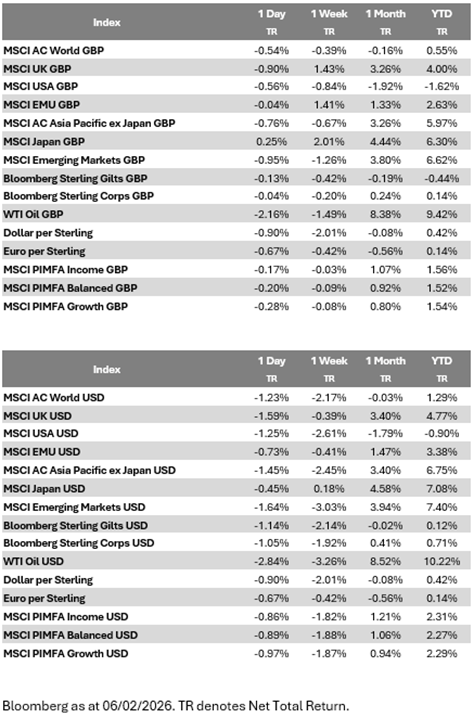

Risk assets continue to be under pressure due a tech-led sell-off combined with softer US. Software stocks led the move, with the S&P 500 software component down -5.01% (its seventh consecutive decline) and the broader S&P 500 falling -1.23% for a third straight session. Volatility rose, with the VIX up to a 2026 high of 21.77. The rout gathered further momentum after the close when Amazon flagged much higher capex (now expected to reach $200bn this year) and cut operating income guidance for the quarter, sending its shares down more than -10% in after hours trading. The weakness was not confined to tech: equal weighted S&P 500 and Europe’s STOXX 600 pulled back from recent record highs, and Bitcoin plunged -13.14% to a 15 month low of $63,083, roughly 50% below its October peak.

Data softening shifts Fed expectations

Yesterday’s US data releases reinforced a softer tone for the labour market. Weekly initial jobless claims rose to an eight week high of 231k (vs. 212k expected), and the JOLTS report showed job openings fell to 6.542m in December (vs. 7.25m expected), the lowest since 2020 and below consensus. Markets interpreted these signs of cooling as giving the Fed more room to ease, pushing the probability of additional cuts higher; the cuts priced by the December meeting rose by 10bps to 60bps. That repricing drove Treasury yields lower across the curve, with the 2 year yield down 10.3bps to 3.45% (its largest one day drop since August) and the 10 year yield down to 4.18%.

Both ECB and BoE pause rates

The ECB held the deposit rate at 2%, with President Lagarde describing inflation as in a “good place,” and markets continue to expect rates to be on hold this year with downside risk. In contrast, the Bank of England’s decision had dovish undertones: a narrow 5–4 vote to hold at 3.75%, language indicating rates are “likely to be reduced further,” and heightened political uncertainty around the Prime Minister weighed on sterling and pushed shorter-dated gilts lower. The 2 year gilt fell 5.6bps to 3.64%. Long end yields rose, leaving the 2s10s curve at its steepest since 2018.

What does Brooks Macdonald think?

The recent moves looked more like a rotation and a volatility repricing than the start of a broad market correction. Software and other high beta names have led the decline, but widening breadth or macro signals deterioration could alter the near term risk/reward. We remain cautious on positioning: expect elevated volatility around earnings and data releases, monitor whether labour market weakness persists, and watch how central bank communications evolve.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Andrew Lloyd

06/02/2026