Please see the below article from Invesco which we received late yesterday afternoon:

Key takeaways

- Investing in stocks which have the right ESG momentum behind them can be a positive way for our funds to potentially generate alpha

- We draw upon ESGintel, Invesco’s proprietary tool, which helps us to better understand how companies are addressing ESG issues

- Engaging with companies to understand corporate strategy today in order to assess how this could evolve in the future

Our focus as active fund managers is always on finding mispriced stocks and ESG integration underpins our investment process at every stage.

The incorporation of ESG into our investment process considers ESG factors as inputs into the wider investment process as part of a holistic consideration of the investment risk and opportunity, from valuation through investment process to engagement and monitoring.

The core aspects of our ESG philosophy include materiality; ESG momentum; and engagement.

- Materiality refers to the consideration of ESG issues that are financially material to the corporate or issuer we are analysing.

- The concept of ESG Momentum, or improving ESG performance over time, indicates the degree of improvement of various ESG metrics and factors and help fund managers identify upside in the future. We find that companies which are improving in terms of their ESG practices may enjoy favourable financial performance in the longer term.

- Engagement is part of our responsibility as active owners which we take very seriously, and we see engagement with companies as an opportunity to encourage continual improvement.

Dialogue with portfolio companies is a core part of the investment process for our investment team. As such, we often participate in board level dialogue and are instrumental in giving shareholder views on management, corporate strategy, transparency, and capital allocation as well as wider ESG aspects.

ESG integration is an ongoing strategic effort to systematically incorporate ESG Factors into fundamental analysis. The aim is to provide a 360-degree valuation of financial and non-financial materially relevant considerations and to help guide the portfolio strategy.

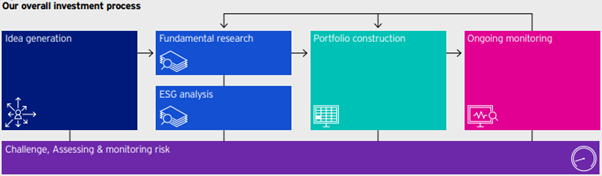

Our investment process has four stages. In this note we go through in detail how ESG is integrated into each stage of our process.

Idea Generation

Ideas come from many sources – our experienced FMs, other team members or investment floor colleagues, various company meetings, and by exploiting the intellectual capital of our sell side contacts. We see it as important to spread our nets as wide as possible when trying to come up with stock ideas which may find their way into our portfolios. We remain open minded as to the type of companies we will consider. This means not ruling out companies just because they happen to be unpopular at that time and vice versa.

ESG can create opportunities too – for example, the benefits of moving towards more sustainable sources of energy like wind, solar and hydroelectric power generation. This was one of the reasons we became interested in some of our utility holdings which are held across several portfolios. This highlights the importance of opportunities brought about by ESG and not just the risks. ESG can also influence the timing and scale of a mispricing being corrected in the market.

To be clear, at this early stage of the investment process we typically would not rule out companies with a sub-optimal ESG score. Investing in stocks which have the right ESG momentum behind them – by focussing on fundamentals and the broader investment landscape – can be a unique way for our funds to potentially generate alpha.

Fundamental Research & ESG Analysis

Research is at the core of what we do and is what the investment team spends most of its time doing. The key is to filter out those ideas which aren’t aligned with our investment philosophy and concentrating on those where we see the strongest investment case. Our fundamental analysis covers many drivers, for example, corporate strategy, market positioning, competitive dynamics, top-down fundamentals, financials, regulation, valuation, and, of course, ESG considerations, which guide our analysis throughout. The key drivers will differ according to each stock.

We use a variety of tools from different providers to measure ESG factors. In addition, at Invesco, we have developed ESGintel, Invesco’s proprietary tool built by our Global ESG research team in collaboration with our Technology Strategy Innovation and Planning (SIP) team. ESGintel provides fund managers with environmental, social and governance insights, metrics, data points and direction of change. In addition, ESGintel offers fund managers an internal rating on a company, a rating trend, and a rank against sector peers. The approach ensures a targeted focus on the issues that matter most for sustainable value creation and risk management.

This provides a holistic view on how a company’s value chain is impacted in different ways by various ESG topics, such as compensation and alignment, health and safety, and low carbon transition/ climate change.

We always try to meet with a company prior to investment. Based on our fundamental research, including any ESG findings, we focus on truly understanding the key drivers and, most importantly, the path to change. This helps us better understand corporate strategy today and how this could evolve in the future. Today, the subject of ESG is increasingly part of these discussions, led by us.

Portfolio Construction

We aim to create a well-diversified portfolio of active positions that reflect our assessment of the potential upside for each stock weighted against our assessment of the risks. Sustainability and ESG factors will be assessed alongside other fundamental drivers of valuation. The impact of any new purchases will need to be considered at a fund level. How will it affect the shape of the portfolio having regard to fund objectives, existing positions, overall size of the fund, liquidity and conviction?

We do not seek out stocks which score well on internal or third party research simply to reduce portfolio risk. We ask the question, “Why does the idea deserve a place in the portfolio?” We ask this because there is a competition for capital, a new idea will require something else to be sold or reduced so that it can be included.

Ongoing Monitoring

Our fund managers and analysts continuously monitor how the stocks are performing as well as considering possible replacements. Are the investment cases strengthening or weakening? Are their valuations reflecting the companies’ prospects appropriately? Is the company performing from an ESG perspective and are the valuations fairly reflecting the progress being made or not? Are the anticipated key drivers playing out or not? These questions, and their answers, are all of equal importance to us.

How do we monitor our holdings from an ESG perspective? Again, the same resources used during the fundamental stage are available to us. Our regular meetings with the management teams of the companies we own provides an ideal platform to discuss key ESG issues, which will be researched in advance. We draw on our own knowledge as well as relevant analysis from our ESG team and data from our previously mentioned proprietary system ESGintel which allows us to monitor progress and improvement against sector peers. Outside of company management meetings we constantly discuss as a team all relevant ESG issues, either stimulated internally or from external sources.

Additional ESG analysis is carried out by the team, when warranted, on particular companies. Depending on the particular case this is often in conjunction with the ESG team. Such cases would be those that are more controversial, considered to be higher risk and viewed poorly by ESG providers, resulting in a valuation discount. We don’t just look at the specific issue considered to be higher risk either, for example the environmental risk of an oil company, but all areas of ESG. This means undertaking extensive analysis of social and governance policies and actions at the same time. We would note that this analysis is an ongoing process, typically involving multiple engagements with the company over a long period of time. All ESG discussions and interactions are written up – including our views and thoughts – with a section solely dedicated to ESG. Likewise, research undertaken by the ESG team is available to the entire Henley investment floor, and wider business. Further analysis could be warranted as a result of these discussions.

Challenge, Assessing & Monitoring Risk

In addition to the above, there are two more formal ways in which our funds are monitored:

There is a rigorous semi-annual review process which includes a meeting led by the ESG team to assess how our various portfolios are performing from an ESG perspective. This ensures a circular process for identifying flags and monitoring of improvements over time. These meetings are important in capturing issues that have developed and evolved whilst we have been shareholders. It is our responsibility to decide if it is appropriate, or not, to investigate these issues in more detail. We may ask the ESG team to assist in undertaking more analysis or discuss such issues with the company themselves or external brokers.

There is also the ‘CIO challenge’, a formal review meeting held between the Henley Investment Centre’s CIO and each fund manager. Prior to the meeting, the Investment Oversight Team prepare a detailed review of a portfolio managed by the fund manager. This review includes a full breakdown of the ESG performance using Sustainalytics and ISS data, such as the absolute ESG performance of the fund, relative performance to benchmarks, stocks exposed to severe controversies, top and bottom ESG performers, carbon intensity and trends. The ESG team review the ESG data and develop stock specific or thematic ESG questions. The ESG performance of the fund is discussed in the CIO challenge meeting, with the CIO using the data and the stock specific questions to analyse the fund manager’s level of ESG integration. The aim of these meetings is not to prevent a fund manager from holding any specific stock: rather, what matters is that the fund manager can evidence understanding of ESG issues and show that they have been taken into consideration when building the investment case.

Conclusion

The regulatory landscape is rapidly evolving, which increasingly compels organisations and investors alike to clearly demonstrate their awareness of ESG issues in their decisions. Landmark initiatives such as the European Union’s new Sustainable Finance Disclosure Regulation (SFDR) are at the forefront of this shift.

We believe that our approach is honest, coherent and pragmatic. The principles behind ESG deserve to be embedded in an investment framework which encourages positive change. Coupling this with a focus on valuation is, to our minds, the best way to deliver strong investment outcomes for our clients’ long term. This reinforces our fundamental belief that responsible investing demands a long-term view and that a stakeholder-centric culture of ownership and stewardship is at the heart of ESG integration.

This is a good article and insight into how Invesco integrate ESG into their investment process. We would expect more fund managers to start publishing their ESG process (if they haven’t already!).

Please keep an eye out for further ESG related content from us, along with our usual market commentary and blog updates.

Andrew Lloyd

11/03/2021