Please see article below from Legal & General’s asset allocation team – received 07/09/2020

Techastrophe or Techantrum?

This week we focus on technology stocks, given the recent drama, but also stand back from the hurly-burly and reflect on how far expectations for a vaccine have come since COVID-19 hit in the spring. We also touch on the recent change in tack from the European Central Bank (ECB) where the drumbeats of verbal intervention have started, and inflation data have – once again – been dire.

As with all Key Beliefs emails, this email represents solely the investment views of LGIM’s Asset Allocation team.

Shaken, not stirred

In an impeccably timed blog published last Thursday, Lars asked whether now is the time to start taking profits on technology stocks. Investors across the world obviously took note and decided that the short-term answer was an overwhelming ‘yes’, with the Nasdaq down around 10% in just two days. In recent months, we’ve seen record after record broken by technology stocks.

Nigel Masding on the Active Equity team produced some eye-popping statistics this week, looking at year-to-date returns for the MSCI World, which sum this up nicely. Until the end of August, the index of 1,718 stocks had generated a return of +5.7%. Just four stocks contributed enough on their own to push the index into positive territory and to deliver this return: Apple, Amazon, Microsoft* and Tesla*. An index composed of the other 1,714 stocks is still underwater (source: Bloomberg).

With that in mind, are we seeing the tech bubble pop or is this just a short technical correction? We favour the latter interpretation. There was no apparent news flow that was a convincing catalyst for the move and the overall pattern of performance within equities was not consistent with a risk-off environment or of particular virus concerns. Still, there were a few hints of pretty irrational behaviour in the immediate run-up to Thursday, with high-profile stock splits seemingly responsible for driving tech names higher last Monday and Tuesday.

We have long-held two guiding principles for assessing when the time might be right to exit technology stocks: excessive valuations and excessive bullishness. In our opinion, neither signal has turned red yet. Outperformance has been driven by a step-change in earnings rather than by valuations. On sentiment, it is impossible to argue that tech is a particularly unpopular sector, but we don’t see signs of excessive bullishness either. For context, we’ve been tactically positive on technology stocks (relative to the broader market) since early 2018.

In the week in which a new trailer for the latest Bond film was released, our conviction in that trade is shaken, not stirred.

Vaccination vacillation

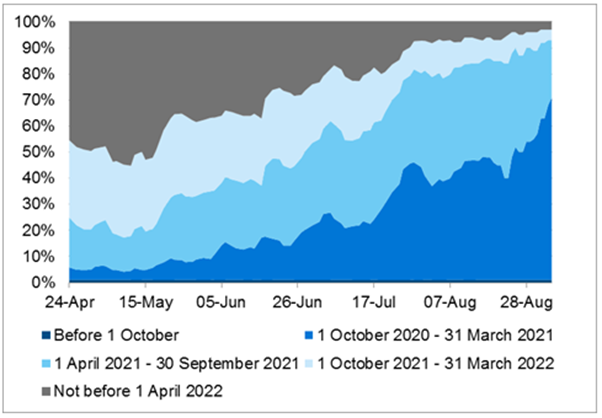

In the late 18th century, Edward Jenner pioneered the world’s first inoculation by intentionally infecting an eight year old boy with cowpox. Medical trials have evolved somewhat since then, but the word vaccine still derives from the Latin for cow. And it is hopes of a vaccine breakthrough that have continued to drive the bull market in equities and credit over recent months. This week saw the Centre for Disease Control (CDC) in the US issue advice to State governors to prepare for potential vaccine distribution as early as 1 November. The chart below, from Professor Philip Tetlock’s Good Judgement Project, shows the extraordinary change in expectations around the timeline to that vaccine. The chance of a vaccine being widely available by March next year is now seen as more likely than not, having been almost inconceivable only a few months ago.

Good Judgement Project: When will enough doses of FDA-approved COVID-19 vaccine(s) to inoculate 25 million people be distributed in the United States?

Source: LGIM, Good Judgement Project, 4 September 2020. There is no guarantee that any forecasts made will come to pass.

In the meantime, Jason Shoup of LGIM America raises the intriguing possibility of a breakthrough in testing technology. If cheap (<$5), rapid (<15 min), saliva-based (i.e. no nose swab), and self-administered coronavirus tests become widely available, it would allow a rapid normalisation in sectors where social distancing is difficult/impossible. The US government have called the development of a vaccine “Operation Warp Speed”. Not to be outdone, the UK government dubbed the development of rapid testing technology “Operation Moonshot”.

Financial markets will be willing to forgive signs of an economic stumble in the short term, provided that the medium-term outlook continues to look reassuring. With COVID-19 cases rising fairly rapidly across large parts of Europe again, these breakthroughs cannot come soon enough.

EUR-eka moment in FX markets

In the last few years, one of the most consistently poorly performing investment strategies has been following currency momentum. The kind of sustained multi-year currency trends that characterised the 1990s and 2000s have become a thing of the past as central banks deploy verbal (and the threat of actual) intervention to manage exchange rates within relatively narrow corridors. This change in landscape has become so extreme that anti-momentum currency trades have been started to become consistent winners. The post-COVID-19 currency markets have been dominated by a lurch lower in the US dollar that threatened to break that pattern: on a broad trade-weighted basis, the dollar index is down around 10% since the March highs with the Federal Reserve’s framework review providing the latest catalyst.

This week brought the first serious pushback against that trend from the ECB. Philip Lane, the central bank’s chief economist said the “euro-dollar rate does matter”. Sternly worded stuff, indeed! More revealing, a number of his colleagues on the Governing Council, under the veil of anonymity provided by an FT article, followed up with even stronger comments: the strengthening of the euro is a “growing concern” and “worrisome”. These kind of comments hark back to the days when Jean-Claude Trichet, former ECB president, used to bemoan “brutal” FX moves.

The market seems to have taken this as an indication that 1.20 is some kind of line-in-the-sand for the single currency. For that to be effective, the ECB will soon need to back up words with action. The ECB is obviously heavily constrained in its ability to cut interest rates further, but we anticipate an extension of the quantitative easing programme to be announced in the next few months. That won’t be a big surprise to the market, but should help to keep a lid on government funding costs in the periphery and tame the recent burst of euro strength, in our view.

The urgency of addressing the situation will have been underlined by some exceptionally weak European inflation data this week. European headline inflation dropped back below zero for the first time since 2016. On a core basis, HICP inflation dropped to the lowest level on record at just 0.4%. There are exceptional circumstances associated with the timing of summer sales, but these are the kind of numbers that will bring an inflation-targeting central banker out in a cold sweat. With the ECB looking dangerously like Old Mother Hubbard (with a bare policy cupboard) we think that staying short European inflation is a strategy likely to benefit from a consistent fundamental tailwind. *For illustrative purposes only. The above information does not constitute a recommendation to buy or sell any security.

A useful article from Legal & General’s Asset Allocation team with a focus on technology stocks, a vaccine for COVID-19 and the recent change in tack from the European Central Bank.

Please continue to check back for out latest updates and blog posts.

Charlotte Ennis

08/09/2020