Please see below article received from Evelyn Partners yesterday evening, which conveys their thoughts on yesterday’s US CPI inflation announcement.

What happened?

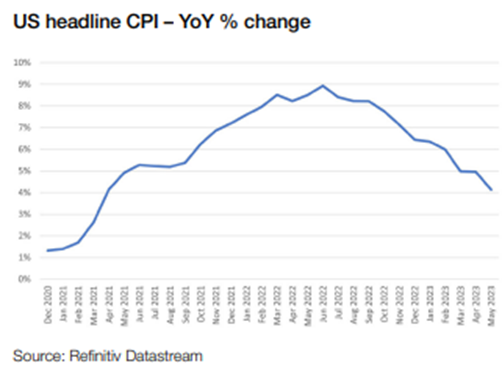

US August annual headline CPI inflation rose 3.7% (consensus: +3.6%), compared to 3.2% in July. In monthly terms, CPI rose 0.6% (consensus: +0.6%), compared to a gain of 0.2% in July.

August annual core inflation (excluding food and energy) rose 4.3% (consensus: +4.3%), versus 4.7% in July. In monthly terms, core CPI rose 0.3% (consensus: +0.2%), compared to a gain of 0.2% in July.

What does it mean?

August’s inflation report saw the monthly headline rate jump to 0.6%, its highest rate since June 2022. Much of this upward pricing pressure came from energy, with the monthly inflation rate for the sector accelerating to 5.6%. A significant driving factor of this was the recent surge in crude oil, which prompted gasoline prices at the pump to rise during August. The index for gasoline was the largest contributor to the monthly all items increase, accounting for over half the increase.

In a repeat of July, unfavourable base effects continued to put upward pressure on the annual headline rate, with a favourable 0.1% monthly reading from August 2022 dropping out of the annual comparison. In Contrast, the next two prints for September and October have more constructive starting points, so should allow room for the annual rate to begin to decelerate again from next month.

Core goods continues to remain soft with the annual rate for the sector now at 0.2%. Used cars and trucks were once again the main driver of this category with prices having fallen now for three consecutive months. However, core services remain stickier, but have been slowly decelerating. Shelter continues to put upward pressure on the index, accelerating 0.3% on the month.

Combining these core sectors paints a very promising picture for the overall core inflation rate which decelerated to 4.3% on an annual basis in August. Calculating core inflation in a 3-month annualised basis yields an encouraging 2.2%, which should instil the Fed with confidence that their battle against inflation is approaching its final stages.

Despite the labour market showing signs of easing, with non-farm payrolls adding less than 200k jobs in each of the last three months, persistent wage growth could prove problematic for this goldilocks inflation story. Average hourly earnings continue to remain resilient, gaining 4.3% for the year in August, which remains too high to be consistent with the Fed’s 2% inflation target. With real wage growth in positive territory, this could prompt an increase in consumption, rendering the Fed’s task of bringing inflation back to target more challenging.

Bottom Line

With two months of reassuring new data under their belts, the FOMC committee members should feel they have enough evidence of easing inflation and a softening labour market conditions to resist hiking at next week’s monetary policy meeting. However, with the US economy continuing to expand, it is likely the FOMC will be able to keep rates higher for longer, so rate cuts are likely not yet on the horizon.

Please check in again with us soon for further relevant content and news.

Chloe

14/09/2023