Please see this week’s Tatton Monday Digest discussing the key economic news from the past week:

Overview: disinflation sentiment cheers investors

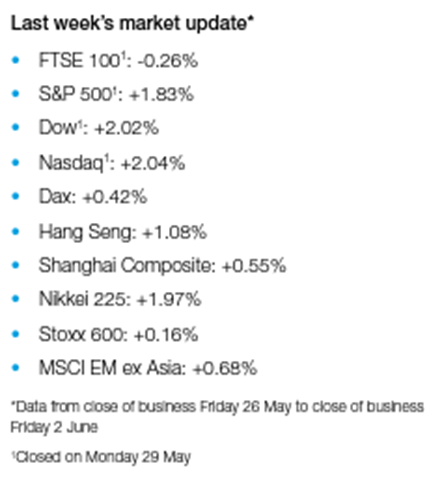

Last week was another positive one for global stock markets, with the narrative of a soft economic landing in 2023 appearing to gather support. Stock market gains in June have been spreading to the mid and small cap market segments, rather than just for a handful of mega-caps. In the US, the mostly small cap Russell 2000 index has risen about 8%, versus 4% for the mega tech-heavy NASDAQ 100. Europe has also seen similar moves, suggesting investors are gaining confidence that the headwinds to growth are turning towards tailwinds, thereby preventing a recession.

Even emerging markets have started June in a more upbeat fashion, compared to a rather muted May. This should probably be seen as win, given the disappointment around China. The world’s second-largest economy – and by far the biggest component of MSCI’s EM index – has been struggling under the weight of expectation for months now. The anti-climax has induced another policy move by Chinese authorities, this time asking banks to reduce interest payments to depositors and to indicate a round of equity market support. There is plenty of liquidity in China, but depressed investor confidence has made valuations there very cheap, so we may be in for a sharp bounce in Chinese equities should the authorities succeed.

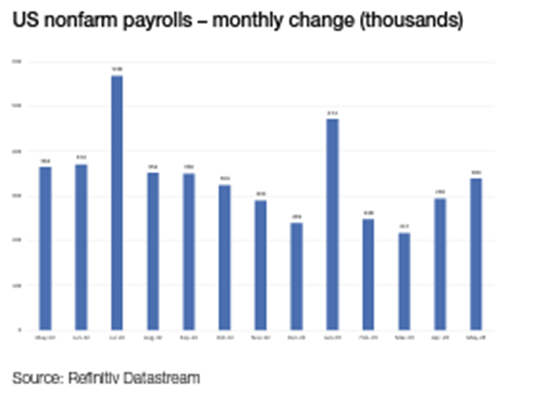

Further China policy easing will be another tailwind, and not just for China. However, until the inflation picture really improves in the developed world, central banks will still feel obligated to keep raising interest rates. Last week, both Canada and Australia surprised markets by both hiking rates another 0.25%. This week it could be the turn of the US Federal Reserve (Fed), with its Open Market Committee meeting on Wednesday. Markets have come to expect another rate rise, if not next week, then in July. For what it’s worth, we are not so sure. May’s payroll survey showed a sharp jump in the number of people employed but was quite downbeat in other areas, and the unemployment rate rose to 3.7%. Another factor that could stay the Fed’s hand is the resumption of US Treasury financing after the debt ceiling resolution. The Fed’s current account must be replenished – by issuing large amounts of short-term government debt at competitive rates – and that could drag money away from those rather stressed US regional banks. After March’s unnerving (and economy damaging) episode, another rate rise now risks worsening the situation and causing a second round of bank failures.

We wrote last week that optimists had gained the upper hand over the pessimists and last week’s market gains tell a similar story. It seems that while markets are never without their worries even the pessimists may find it difficult to be apocalyptic when the sun shines.

Japan’s new rising sun?

Japan is having a moment. Over the last three months, its stock market has been the best performer of all the headline regions we track. In the middle of May, the Topix returned to its highest level since 1989, and in June it has taken another leg up, rallying strongly last Monday and Tuesday in particular. Inflation, something that has been virtually absent in Japan for more than three decades, came in at 3.5% in April – coming down from the 40-year high of 4.3% in January. Many investors, both foreign and domestic, expect wage growth will follow. For these reasons and more, markets are more positive about Japan than they have been for a generation.

Celebrating inflation might sound odd, given western economies are still desperately fighting price increases. But deflation has been one of Japan’s biggest problems during its stagnant period, reinforcing savings habits and holding back investment and growth. Inflation has now been running above the Bank of Japan’s (BoJ) 2.0% target for 13 months. But while these sustained price pressures are extremely unusual in Japan, the 3.5% April figure is hardly a cause for concern. The comparative lack of runaway inflation allows the BoJ much more leeway than its global peers. Its interest rates have stayed anchored below 0%, in sharp contrast to the aggressive tightening seen in the US. Lately there have been signs of a rise in the BoJ’s balance sheet. For foreign investors, this has helped underpin the belief that Japan is a safe haven in a risky world.

Before getting carried away, we note Japan has generated similar hype in the past, only for market rallies to peter out when the economy inevitably disappoints. Current detractors say Japan’s inflation is mostly coming from global factors, rather than domestic price pressures, as well as its cyclical sensitivity. Ties with China have been a positive for Japan in the past, but China’s recently disappointing growth has turned this factor into a negative for now. Some have also argued Japanese profitability is only a consequence of the falling yen value, and not a sign of genuine underlying improvement. But this is an oversimplification, as the rise in profitability is not just linked to exporters, but is broad-based across the whole economy. With the home bias among Japanese consumers, we would not expect this if currency depreciation was the only factor at play.

One could just as well argue it is a positive that Japanese profits have kept up in dollar terms – something that was difficult in the past. Moreover, the fall in the yen will have secondary impacts on Japanese exporters, making their products more attractive. If this continues with domestic corporate improvements and economic optimism – as is the case at the moment – it will only strengthen the case for Japan as an investment destination. Japan always does best when it is outward facing and connected to the global economy. Thankfully, its policymakers now seem to recognise that fact.

Please check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Andrew Lloyd DipPFS

12/06/2023