Please see below the latest ‘Markets in Minute’ update from Brewin Dolphin, which covers their views on recent events in markets and was received late yesterday (12/12/2023) afternoon:

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below, Brooks Macdonald’s ‘Weekly Market Commentary’ which provides a brief analysis of the key factors currently affecting global investment markets. Received yesterday afternoon – 11/12/2023

Despite the US equity market now posting its 6th consecutive weekly gain, there should be no complacency ahead of this week which sees a Fed meeting, an ECB meeting and perhaps most importantly, a US CPI print.

Before we move onto this week, we should acknowledge the US employment report which was slightly stronger than markets were expecting on a headline level and saw the US unemployment rate fall to 3.7% versus the 3.9% expected. Average hourly earnings were also slightly stronger than expectations. Taken as a whole, the US jobs report pushed back against the soft-landing narrative and expectations for a near immediate loosening of policy. There was some good news on Friday however as the University of Michigan survey showed 1 year inflation surprising to the downside, coming in at 3.1% versus the 4.3% that was expected.

The jobs report is likely to dissuade the Fed from sounding too dovish this week and markets also reduced the implied number of interest rate cuts in 2024 as a result. The key question for Wednesday’s Fed meeting statement will be whether the Fed explicitly rebukes the market’s pricing of around 4½ 25bp interest rate cuts in 2024. With the jobs report in recent memory, the Fed is likely to strike a more cautious tone, saying that while rate rises are likely finished, this does not mean rate cuts are imminent. The tone of the statement and press conference will be key, as will the dot plot of interest rate expectations. The ECB and Bank of England will report on Thursday, with expectations of a pause in interest rates from both central banks.

Before we get to the trio of central banks, markets will need to contend with the US CPI release on Tuesday. The consensus expects there to be no month-on-month inflation at a headline level and 0.3% growth for Core CPI. The major difference between these two readings is the gas price which is down -8% since October and is excluded from the Core CPI reading. The two-day Federal Reserve meeting will already be underway when the CPI report lands but it is undoubtedly going to feed into their thinking if we see an upside or downside surprise.

Please continue to check our blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below ‘Monday Digest’ article received from Tatton this morning, which provides a global market update as we approach Christmas.

After a gangbusters November for global capital markets, December is also currently on a positive track with trading volumes higher than November’s averages generally, suggesting quite a bit of capital is being put to work by investors.

Global bond yields have fallen yet again (meaning bond prices have risen), driven by fears of slowing global growth. Economic data has been mildly soft, while energy and commodities have been weak. European bonds outperformed following dovish noises from members of the European Central Bank (ECB).

Economic data showed soft (but not awful) purchasing manager survey indices, offset somewhat by US mixed employment data. In the US, the job agency ADP’s November employment report weakened but Friday’s US employment report surprised economists by showing 199,000 jobs were added in November, a reasonable level of job creation paired with a very surprising fall in the unemployment rate, down to 3.7% from October’s 3.9%. Still, rate expectations have fallen because the policy setters at the US Federal Reserve (Fed) appear be more focused on inflation declines than worrying about what level of unemployment is too low for comfort. Nevertheless, bond investors had expected the US unemployment rate to worsen to 4% at least and November’s data does not support the case for any rate cuts without some other factor impinging.

But it seems bonds and equities are taking more of a cue from commodities and energy.

Equities ended the week back up to recent highs, with the US ‘Magnificent Seven’ bouncing back from fears about their exposure to softer consumer demand. Stocks had seen softness despite falling bond yields, as investors started to worry that earnings prospects may be challenged, with oil sending quite a weak growth signal.

Last week, we said how OPEC’s inability to act as bloc had led to ineffective supply cuts. Since then we have seen more oil price falls, and in addition, global industrial metals and agricultural prices moved down. They are less volatile than energy prices (mainly because energy stores are always relatively low compared to ongoing use) so the lesser decline is still significant. Commodity prices are still higher than they were 2021 but the decline from mid-2022 is clear. In the past 15 years, the biggest demand swing has emanated from China and there are all sorts of signals that the world’s second-largest economy is not providing the growth leadership that the largest economy in the world has given us.

With COP28 coming to a close at the weekend, the discussions have been neither a help nor a hindrance to asset and commodity prices, nor perhaps should they be, although COP28 president Sultan Al Jaber took the opportunity to swing the debate towards responsible fossil fuel policies. Ultimately, progress on dealing with emissions will be in the enactment of detailed policy, so perhaps this is good news. The conference also turned its attention to the loss of the natural world, which many think is a good refocusing.

Moody’s weighs in to add to the Chinese gloom November was the continuation of a miserable year in Chinese markets, where economic and policy disappointments have been the defining feature. At the time of writing, the CSI is down 12.5% year-to-date in renminbi terms, while the Hang Seng has dropped a painful 18.3%. Weaker-than-expected growth and trade – compared to admittedly high expectations – has been the root of China’s issues for some time. The government has repeatedly tried to counteract this with various support schemes or political pronouncements – to varying degrees of success.

Last week brought another headache for Beijing, after ratings agency Moody’s cut China’s credit outlook to negative. Moody’s pessimism extends to both government and private banking debt – both of which are feeling the pressure from an extended property market downturn. Moody’s has only changed its outlook on Chinese credit, and a slight downgrade is unlikely to affect China’s medium-term borrowing capacity in a big way. That said, the news is clearly not a good thing for the Communist Party government and financial stress has been worsened by the exodus of foreign investors from Chinese markets this year.

The Chinese Politburo met last week to avow a significant fiscal push next year. Among the policies being swung into action, the People’s Bank of China (PBOC) has introduced something that looks very much like quantitative easing (QE), or the buying of bonds. This policy can work in different ways but one of its possible implications is that financial market liquidity improves, which can then feed through into rises in risk asset prices. The lack of foreign equity buyers has generated much comment but the similar lack of domestic equity buyers has also been notable.

Chinese consumers are feeling pessimistic to, and for good reason: 8.5 million of them (around 1% of the total working-age population) have defaulted on debt payments since the start of the pandemic and been blacklisted by authorities. As well as severely constraining China’s domestic demand – a side of the economy Beijing avowedly wants to foster – struggling consumers cannot pay taxes, hence reducing the government’s funds and worsening its fiscal metrics. All of this puts the Party in a precarious position.

This weakness is surely one of the main reasons China has been so conciliatory toward the west in recent months. It is hard to see President Xi’s meeting with President Biden last month – his first visit to the US since early 2017 – as anything other than a big peace offering. Trade tensions between the world’s two largest economies may well continue, but they are likely to be pushed much more by Biden than Xi. For the global economy at least, conciliation is a positive. But for China, its underlying weakness seems worryingly hard to address.

Please check in again with us soon for further relevant content and news.

Please see below article received from Brewin Dolphin yesterday evening, which looks to the future as we near the end of 2023.

After a year of interest rate hikes and renewed geopolitical uncertainty, Guy Foster, our Chief Strategist, discusses what the next 12 months could have in store for investors.

This time last year, economists were talking about the near inevitability of a recession in 2023. In the event, the economy proved more resilient than many expected. Now, forecasts are improving for 2024 as well. If anything, the last year has reminded many forecasters that predicting recessions is a task that has eluded the best-resourced central banks for decades.

So, what can we say about the possibility of a recession hitting in 2024?

Some conditions for a recession are already fulfilled. Economists believe that most developed economies are operating beyond their capacity. This jargon refers to the fact that demand currently exceeds supply. There are, for example, shortages of some of the things economies need to grow – the most obvious being skilled labour.

Under such circumstances, central banks have been trying to bring demand and supply back into balance. One such way has sought to reduce the demand by raising interest rates. The question is whether they are able to do so with enough finesse that they do not discourage spending so heavily that they inadvertently plunge the economy into a recession.

Typically, this has proven to be a task at which policymakers fail more often than they succeed.

For them to succeed, we would need to see a more gradual realignment of demand and supply in such a way that doesn’t cause a sharp increase in unemployment. Investors call this ideal scenario a ‘soft landing’ for the economy, making it distinct from the ‘hard landing’ of a recession.

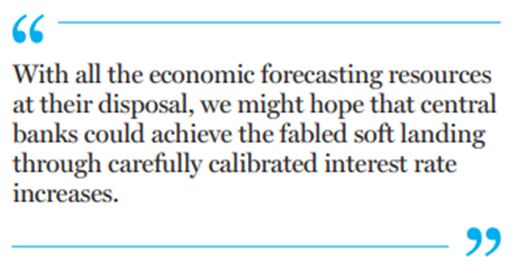

Will central banks achieve a soft landing?

With all the economic forecasting resources at their disposal, and plenty of practice, we might hope that central banks could achieve the fabled soft landing through carefully calibrated interest rate increases. The fact that inflation does seem to have peaked gives hope. But these interest rate increases do not take place in a vacuum. Often, it is the combination of the stress of higher interest rates and an external shock that tips the economy over the edge.

Examples of these shocks include the bankruptcy of Lehman Brothers and the collapse of a US housing bubble that prompted a global recession during 2008 and 2009; the collapse of the speculative bubble in technology stocks at the start of the millennium; and, in the early 1990s, the first Gulf War, which saw a sharp increase in oil prices.

So in terms of predicting whether the UK, the US or the world will enter a recession next year, we can say it is possible. In the end, however, it will likely depend upon whether the economy is subjected to some shocks which, by their nature, are unpredictable. It’s often appropriate to paraphrase former US defence secretary Donald Rumsfeld: “There are things we know we know, there are things we know we don’t know, and there are things we don’t know that we don’t know.” This is useful structure for considering the risk in economic forecasting.

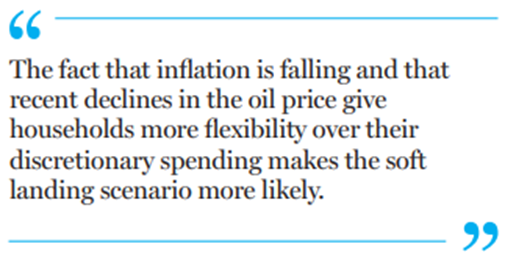

What ‘we know we know’ is that the labour market is tight and interest rates have increased substantially, which raises the risk of a recession. However, the fact that inflation is falling and that recent declines in the oil price give households more flexibility over their discretionary spending makes the soft landing scenario more likely.

The things that ‘we know we don’t know’ would include whether tensions in the Middle East could disrupt oil supply and cause a price spike of the kind that has shocked the economy into recessions in the past.

But above all, there are the things ‘we don’t know that we don’t know’. As with every year, we have to acknowledge that things could happen that will not have been predicted in this or any other outlook piece. And it is that uncertainty which has historically made the forecasting of recessions a very challenging task.

Beyond the likelihood of a potential recession, we should also consider the potential severity of one. The recession taking place as Covid struck was by far the deepest in modern times (fortunately, it was also the briefest). Prior to that, the recession accompanying the financial crisis was the deepest since the early 1900s. The bubble in real estate was symptomatic of very high levels of consumer indebtedness, which ultimately caused such a severe recession. Households then spent the following decade reducing their reliance on debt and, in aggregate, are in relatively robust financial health.

What impact could upcoming elections have?

The main concern for the coming year is not consumer indebtedness, but government indebtedness – both in terms of the risk that it could cause a shock and because of the constraints that it places governments under.

For many years, there has been anxiety over the seemingly inexorable march upwards in government debt to gross domestic product (GDP) ratios. GDP is a measure of the money that gets earned within an economy and, as such, represents an upper limit on the amount that can be used to derive government revenues (what can be taxed).

The outlook for public finances will be a further ‘known unknown’ because there are a lot of elections taking place during 2024. The two obvious ones will be a probable election in the UK (which could theoretically be held any time until January 2025) and November’s election in the US.

The UK endured a brush with fiscal mortality following the mini-budget of September 2022. Even prior to that, there was widespread acceptance by both major political parties that fiscal policy should be constrained by a robust fiscal framework with independent verification of government financial projections (from the Office for Budget Responsibility). Whilst both parties will attempt to thread the needle between appearing not to be neglectful of public services and giving hope that the historically high tax burden can be reduced, it seems unlikely that either will offer particularly bold policies to do so. Labour (which currently enjoys a commanding lead in the polls) has adopted a more centrist approach after an unsuccessful lurch to the left between 2015 and 2020. The nuance upon which the election will be fought will not be revealed until a date is set, but is likely to focus on distributional and social rather than major economic differences.

In the US, it seems likely that November’s election will be contested between president Joe Biden and former president Donald Trump. Neither seems likely to strike an austere tone on the public finances, and it is possible that the bond market could react should it appear likely that Trump will win. This is because as the Republican candidate, he has a greater chance of controlling the two houses of Congress, which set budgets, than his likely opponent. Control of the Senate, where only a third of seats are contested each election, seems very difficult for the Democrats to retain. If Congress is divided, then financial policies tend to be restrained by partisanship.

What is the overall outlook for investments?

Whilst many will look to the coming election season with dread, the bright news from an investment perspective is that US election years have historically produced quite good returns. Brighter still are the relatively high yields on bonds, which now promise better returns in future years than they had done for a decade or more. These yields reflect current high interest rates, which bring the likelihood of interest rate cuts over the coming year, either to prevent a recession or at least reduce its seriousness. These are tailwinds for the equity markets.

Please check in again with us shortly for further relevant content and market news.

Please see todays daily update from Epic Investment Partners received this morning:

A few days ago, we learned that Israeli Prime Minister Benjamin Netanyahu had suspended a junior cabinet member from meetings “until further notice.” This action was taken in response to a comment that seemed to imply the individual would not object to nuclear weapons being used on Gaza. Israel’s far-right Heritage Minister, Amihay Eliyahu, also suggested that displaced refugees could “relocate to Ireland or deserts,” and that the “individuals in Gaza should find a solution on their own.”

In light of this suspension, we decided to investigate the number of nuclear weapons that Israel – and indeed the rest of the world – currently possess. We obtained our data from Google Bard. In ascending order, North Korea has 10 nuclear weapons, followed by Israel with 90. Pakistan and India have approximately 165 and 150 respectively. France has 290, while the UK has 225. China has 280, although a recent Pentagon report estimates that China now has around 500 operational warheads. However, even when combined, these figures represent only about 10% of the total number of nuclear weapons that the US and Russia possess. The US has 5,428 weapons, while Russia has 5,977.

On a positive note, the total number of nuclear weapons worldwide is estimated to be ‘only’ around 13,000. While still a large number, this is a significant decrease from the peak of over 70,000 during the Cold War.

Thankfully, we don’t have a narcissistic maniac or someone old enough to be many people’s great (great?) grandad with their fingers on the proverbial big red button!

Please continue to check our blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below, Brooks Macdonald’s ‘Daily Investment Bulletin’ received this morning – 07/12/2023.

What has happened

Yesterday’s European and US trading session saw the bond market rally continue apace however this exuberance was then curtailed by comments from the Bank of Japan suggesting an imminent change to their interest rate policy.

Bond market rally

Ahead of the Bank of Japan comments, European and US markets were becoming increasingly optimistic around the probability of a soft-landing in the US. The ADP report of private payrolls came in below expectations, supporting the view that the US labour market was cooling. Oil prices also dipped, falling to a 5-month low as weaker global economic demand was priced in. The transmission mechanism between changes in the oil price and headline inflation is rapid, particularly in the United States, so this is further good news for the market’s aggressive pricing of interest rate cuts in 2024.

Bank of Japan

Deputy Governor Himono disturbed the calm within bond markets however, observing that the negative interest rate policy of the central bank had impacted households and that a move to a positive rate would be helpful to improve household interest income. Himono said that he expected ‘there would be a sufficient possibility of achieving a positive outcome from the exit, since a wide range of households and firms would benefit from the virtuous cycle between wages and prices.’ Governor Ueda added that he saw policy management becoming ‘even more challenging from the year-end and heading into next year’, suggesting that changes were afoot. Expectations are growing that the Bank of Japan may therefore abandon its negative interest rate policy as soon as the 15th December central bank meeting. Japanese 10-year bond yields underperformed sharply as a result, leading the Japanese equity index lower in sympathy.

What does Brooks Macdonald think

The Bank of Japan is one of the last bastions of the pre 2022 ultra-low interest rate policy. The recent Tokyo CPI numbers suggested that there was less urgency to abandon the central bank’s negative interest rate policy which has been in place to disincentivise cash savings and drive consumption, in order to kickstart a moderate amount of inflation. If the Bank of Japan was to remove this policy, it would have global implications as the Yen remains one of the few markets globally where borrowing costs remain very low.

Bloomberg as at 07/12/2023. TR denotes Net Total Return

Please continue to check our blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see the below article from Brewin Dolphin which covers their views on recent events in markets. Received late yesterday.

Stocks in the green as inflation cools

Most markets finished the week in the green as inflation cooled in the US and eurozone. The UK’s FTSE 100 added 0.9% as house prices continued to recover and the manufacturing sector showed signs of improvement in November. Germany’s Dax added 2.7% while pan-European Stoxx 600 gained 1.7% as eurozone inflation cooled in November. In the US, the S&P 500 added 1.0%, the Dow grew 2.6% and Nasdaq rose 0.5% as the Federal Reserve’s preferred inflation gauge showed the rate of inflation slowed in October. Meanwhile in Asia, Hong Kong’s Hang Seng dropped 4.0% while China’s Shanghai Composite ended the week flat amid ongoing concerns about China’s economic recovery.

Rising bond yields affect investor sentiment

US markets closed in the red on Monday (4 December) as investor sentiment was marred by Treasury bond yields rising to 4.29%. The increase raised concerns among investors that Fed rate cuts may be further away than initially thought. The S&P 500 lost 0.5% and the Nasdaq dropped 0.8%, while the Dow fell 0.5%.

European markets were mixed as investors awaited US jobs data, including job openings and non-farms payroll data. The Stoxx 600 lost 0.1% and the FTSE 100 lost 0.2%, while the Dax made a marginal rise.

Eurozone inflation cools

Inflation in the eurozone area cooled more than expected to an annualised 2.4% in November, down from 2.9% in October, according to Eurostat. Economists had predicted a more modest decline to 2.7%.

The main inflation driver – food, alcohol and tobacco – saw price growth weaken from 7.4% in October to 6.9% in November. Services and non-energy and industrial goods also fell to 4.0% and 2.9%, respectively, in November – down from 4.6% and 3.5%, respectively, in October. Energy prices continued to fall to -11.5%, down from -11.2% in October.

The core annual inflation rate, which excludes energy, food, alcohol and tobacco, fell to 3.6% in November, down from 4.2% in October.

Although the headline inflation rate is moving closer to the European Central Bank (ECB)’s target of 2.0%, it’s “too soon to declare victory over inflation”, said Joachim Nagel, president of the Bundesbank and a member of the ECB Governing Council, which sets the central bank’s rates.

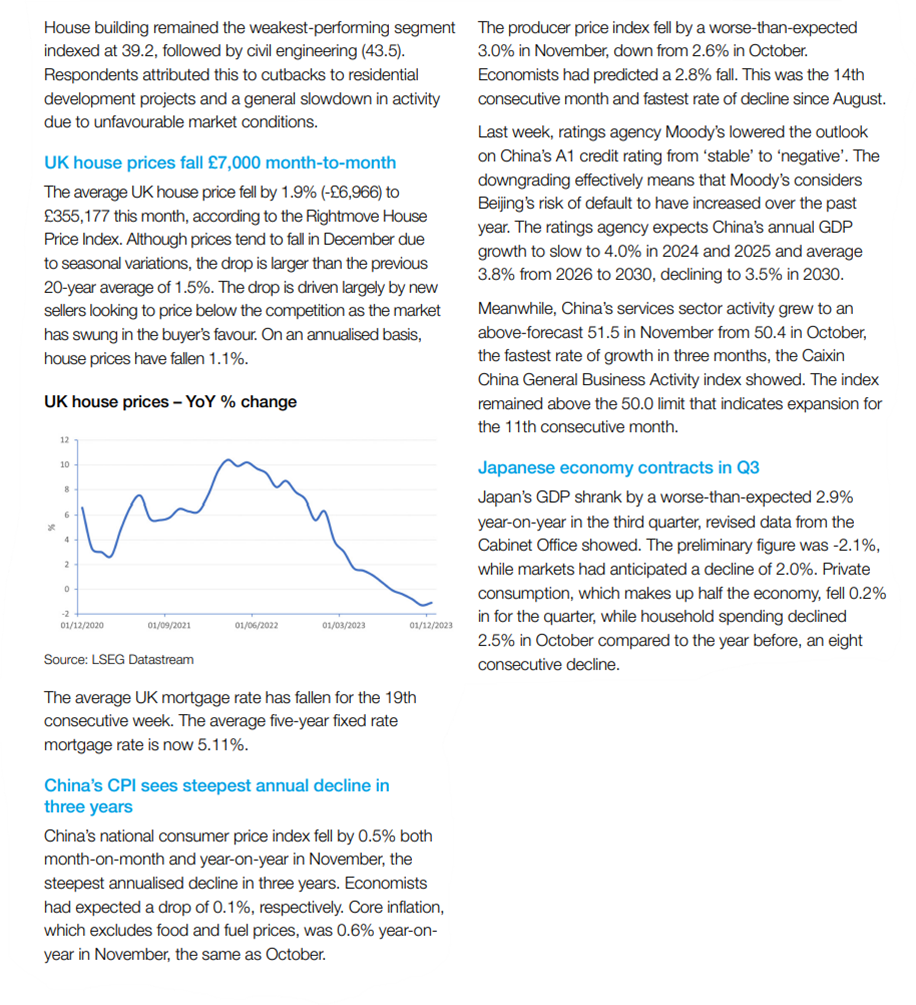

UK house price recovery continues

UK house prices rose 0.2% month-on-month in November, the third consecutive monthly increase. The average house price is now £258,557. On an annualised basis, price growth improved from -3.3% in October to -2.0% in November, the strongest result in nine months.

Falling interest rate expectations among investors have led to lower swap rates, which underpin mortgage pricing, said Robert Gardner, Nationwide’s chief economist. “If sustained, this will help to ease the affordability pressures that have been stifling housing market activity in recent quarters, where the number of mortgage approvals for house purchases has been running at c. 30% below pre[1]pandemic levels.”

OPEC+ agrees to voluntary production cuts

Members of the Organization of the Petroleum Exporting Countries (OPEC+) agreed on Thursday to voluntarily cut oil production by around 2.2 million barrels per day (bpd) in the first quarter of 2024. The decision, which aims to bolster the market, will see Saudi Arabia extend its existing voluntary cut of one million bpd until the end of the first quarter. Meanwhile, Russia will see its current voluntary export reduction deepen from 300,000 bpd to 500,000 bpd.

The announcement was followed by a drop in Brent crude oil prices, with the February contract declining 2.4% to $80.86.

Fed’s preferred inflation gauge rises

In the US, the core measure of the personal consumption expenditures (PCE) price index – which excludes food and energy and is the Fed’s preferred inflation gauge – rose 3.5% year-on-year in October, down from 3.7% in September, according to the US Commerce Department. Headline PCE increased by 3.0% in the 12 months to October, the smallest annualised gain since March 2021. It followed a 3.4% increase in September. On a monthly basis, headline PCE rose less than 0.1% in October, while core PCE increased 0.2%.

Consumer spending, which accounts for two thirds of the US economy, increased 0.2% in October after gaining 0.7% in September. Americans spent 0.4% more on services, including healthcare, housing and utilities, as well as international travel. This was partially offset by a 0.2% drop in spending on goods such as new light trucks, which was likely driven by shortages caused by now[1]ended strikes at a number of factories owned by General Motors, Ford, and Chrysler parent company Stellantis.

China PMI falls in November

China’s official manufacturing purchasing managers’ index (PMI) fell to 49.4 in November from 49.5 in October, the second consecutive monthly contraction. A level of 50.0 indicates growth. The non-manufacturing PMI fell short of economists’ expectations, dropping to 50.2 in November from 50.6 the month before.

Meanwhile, the Caixin/S&P Global manufacturing PMI, which focuses on smaller companies, showed Chinese manufacturing activity rose from 49.5 in October to 50.7 in November, exceeding economists’ predictions. New order growth reached the highest level since June.

Please check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see below, Brooks Macdonald’s ‘Daily Investment Bulletin’ which provides a brief analysis of the key factors currently affecting global markets. Received this morning – 05/12/2023

What has happened?

Monday saw some reversal in the market’s dovish pivot with the highly rate sensitive 2-year Treasury yield rising by almost 10bps on the day. A softer day for bond markets should be read within the context of the extremely strong rally during November and we have, for context, seen similar reversals as recently as Thursday last week. The US equity market suffered under this bond market move however, with the headline index down just over half a percent while technology underperformed, led by the Magnificent 7 mega cap tech stocks.

Bond market moves

There was no specific catalyst for the weaker bond market, it likely represents another pause for breath after dizzying recent downward momentum in bond yields. This week sees a series of important data releases which will add or detract from the probability of a soft landing. Next week contains the Federal Reserve meeting which will see the release of the ‘dot plot’ of interest rate expectations. The dot plot will reveal the gap between the market and the Fed in regards to interest rate cuts in 2024. After previous pivots the Fed has delivered a ‘hawkish rebuke’ of the bond market’s pricing, whether the Fed determines the inflation backdrop warrants a similar pushback will govern market sentiment for December.

Economic data

Today sees the release of the ISM services index which will be an important barometer of US economic health after the manufacturing equivalent was poorer than expected. The JOLTS report will also be a focus of the market, in part due to the proximity of the US employment report on Friday but also due to the ratio of job openings to layoffs remaining at tight levels. In September there were 1.5 job vacancies for each unemployed person, this compares to 1.2 before the pandemic, so jobs remain plentiful.

What does Brooks Macdonald think?

Early this morning, the release of the Tokyo inflation rate surprised to the downside, with headline inflation rising by just 2.6% year-on-year compared to 3% expected. Core CPI also came in one tenth of a percentage point below economist expectations. The Bank of Japan is expected to remove its yield curve control policy, effectively a form of quantitative easing, in coming months however this exit may be pushed back if inflation starts to cool of its own accord.

Please continue to check our blog content for the latest markets and economic updates from leading investment houses.

Please see the below Tatton Investment Management Monday Digest article received this morning – 04/12/2023:

Overview: December brings a price shock reversal

Expectations are growing for Eurozone rate cuts in time for Easter. Speculation intensified followed the release of provisional European inflation data for November that surprised on the low side for the third month running. Overall consumer price inflation came in at 2.4% year-on-year in November, less than half the pace as recently as August. In the US, even though inflation is still between 3% and 4%, some central bankers are validating these ‘next move is down – earlier than thought’ expectations. US Federal Reserve (Fed) member Christopher Waller is noted for similar views to those of Fed Chair Jay Powell, so markets reacted quickly when he said diminishing inflation would naturally allow the Fed to cut rates. Clearly, it is no longer too soon to talk of cuts.

Looking at the changing inflation picture, by far the weakest area of pricing power is now in goods and energy. OPEC+ finally met last week via videoconference, and a cut of 900,000 barrels per day (bpd) was announced. An OPEC+ statement said Russia, the United Arab Emirates (UAE), Kuwait and Iraq made a “voluntary” pledge, while Saudi Arabia would continue its unilateral one million bpd cut until April 2024. Most of the OPEC+ problems are driven by potential global oversupply, with US shale gas extraction increasing and new oil fields opening in in Brazil (which has been invited to join OPEC+). Meanwhile, Saudi Arabia is trying to bring Iran back into the fold as well. Iran is talking about production rising to 4 million bpd next year, a level they’ve not approached in 20 years.

The fall back in energy prices might signal growth worries, but lower energy prices are at the same time a growth spur for the wider economy. The right price is one which stabilises the supply/demand balance, and we should be grateful we are in a period where prices are moving gradually and bearably. This suggests that while we may be experiencing weaker growth now, the likelihood is that costs will be cut naturally and we are in the final stages of a welcome return to normality.

UK inflation exceptionalism

The Bank of England (BoE) continues its expectation management programme. Last Tuesday, Jonathan Haskel, an external member of its Monetary Policy Committee (MPC), told a Warwick University crowd that rates will “have to be held higher and longer than many seem to be expecting”. This came after similar warnings in recent weeks from BoE Chief Economist Huw Pill and Governor Andrew Bailey. The BoE’s Deputy Governor Dave Ramsden warned last week that UK inflation is becoming more “home-grown”, and repeated the messaging that wage growth was driving UK-specific price pressures. That is why, despite the fallback in energy and other input prices globally, Britain’s inflation “is going to be really difficult to squeeze out of the system”.

The BoE and other economists worry Britain’s supply side problems may stem from a combination of pandemic hangovers and Brexit frictions that imposed extra costs on goods and labour relative to our largest trading partner just before the global economy entered an unprecedented period of supply bottlenecks. In this light, UK-specific inflation pressures are unsurprising – as is the BoE’s focus on wage growth from a structurally tighter labour market.

Tight labour markets would suggest interest rates indeed need to remain high. But one could actually argue this is a bigger problem for the US, where growth has stayed strong thanks to a seemingly unshakeable American consumer. In the UK, however, sentiment among both consumers and businesses remains dour. Indeed, despite the BoE’s laser focus on wage growth, for most of the last year headline wage growth figures have been below headline inflation – meaning cuts in real terms. The MPC knows the effect of longer-term rates (often tied to mortgages) on the fragile UK economy, and is likely trying to persuade where it cannot directly control. After all, expectation management is as much a part of monetary policy as interest rates.

Wind of change for renewables?

It has been a miserable year for investors in the renewable energy sector. Tighter oil supplies have pushed up the price of fossil fuels, increasing the short-term returns on oil and gas stocks. When you add in the tightest global monetary conditions in decades – which have hammered valuations for all long-duration assets – it is a recipe for disaster, since clean energy stocks are seen as longer-term investments. The S&P Global Clean Energy Index has fallen over 30% year-to-date. In fact, S&P’s Clean Energy Index achieved dizzying heights at the start of 2021, thanks to sharply rising energy costs and an expected political drive for the global green transition. But shifting macroeconomic factors pushed fossil fuel companies ahead, with clean stocks losing nearly 60% from the January 2021 peak.

Such a prolonged downturn has starved renewables of much-needed investment – particularly damaging for capital-intensive projects like building wind and solar farms. Project cancellations or modifications are happening everywhere you look across the industry (Vattenfall, Siemens Energy AG and Li-Cycle, to name three), with profitability and balance sheet concerns at the root of all of their announcements.

The solution – as energy analysts have argued for years – would be to properly align incentives so that short-term cyclical forces do not outweigh longer-term transitional needs. We have seen at least some progress on this front recently, and the green shoots of a cyclical recovery are also helping to shift the mood. These factors have helped change investor perceptions with the S&P Clean Index rising more than 7% in November. But cyclical moves can only do so much, particularly with markets and the underlying global economy in such a delicate position. For sentiment to swing back around fully, markets need to feel drive to longer-term structural change. The results of the UN COP28 summit will therefore be vital, but rumours that host nation United Arab Emirates plans to use the venue to promote deals for its national oil and gas companies are less than encouraging. Even if investors buy into the renewables story, it will make little difference if politicians are not willing to stand up and join in.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below article received from EPIC Investment Partners this morning, which provides an update on both US and UK markets.

Yesterday, Janet Yellen expressed confidence that the US economy will not require significant hikes from the current level to curb inflation, believing the economy is on a path towards achieving the Fed’s desired soft landing with the unemployment rate averting a sharp increase.

“Signs are very good that we’ll achieve a soft landing, with unemployment stabilising more or less where it is, or in the general vicinity,” Yellen stated, speaking to reporters following a speech at a lithium processing plant in North Carolina.

Yellen added she doesn’t believe the Federal Reserve will need to push as harshly in lowering inflation as it has done in past instances when price rises ran out of control. “Those recessions you’ve talked about were times when the Fed, similar to now, was tightening policy to bring down inflation, but found it necessary to tighten so much that they flipped the economy into a recession,” Yellen said. Adding: “Perhaps it was necessary in order to reduce inflation and expectations of inflation that became ingrained, but we don’t need that now.”

Helping cement that view were the PCE deflator figures, released yesterday. The Fed’s preferred metric for assessing progress on its inflation mandate showed core softening to 0.2%mom, in-line with expectations and below last month’s 0.3% print. Moreover, the measure eased from 3.7%yoy, in October, to 3.5%yoy last month, again in-line with the market consensus.

Here in the UK, we also see the housing market continuing to defy forecasts by some of a sharp correction. House prices climbed for a third straight month according to Nationwide, as a lack of properties and lower borrowing costs underpinned the market. House prices rose by 0.2% in November, against an expectation for a drop of 0.4%.

Following the release, Robert Gardner, the Nationwide’s Chief Economist, said: “There has been a significant change in market expectations for the future path of Bank Rate in recent months which, if sustained, could provide much needed support for housing market activity”.

House prices are roughly 5.5% lower from where they peaked in August 2022. Many had predicted a 10% fall this year with some outliers going for 20%, even 25% lower. The average cost of a house in the UK is now just over £258,500.

Please check in again with us shortly for further relevant content and news.