Please see below, an article from Tatton Investment Management, analysing the key factors currently affecting global investment markets. Received this morning – 08/12/2025

Waiting for a Santa Rally

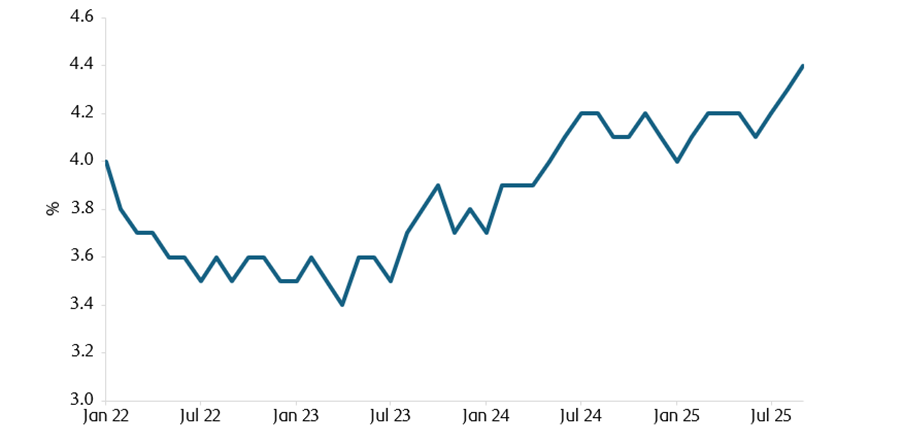

Capital markets felt slightly better last week, with incremental gains. Underlying these moves was a genuine improvement in the outlook. Increased expectations of a Federal Reserve rate cut for December – a near certainty after ADP’s weaker-than-expected employment figures – were a big part of that.

Former Fed governor Rob Kaplan has argued that the Fed should wait until January, since it is better to move too late than move in the wrong direction. We could still find out the labour market is tighter than expected, given the White House’s deportation drive and lack of skilled labour. The Fed is struggling with internal division (Miran cuts a lone dovish figure, but could be joined by Trump ally Kevin Hassett as Fed chair) and a mixed “K-shaped economy”, as discussed below.

US companies, particularly small and mid-cap, are already revising earnings upwards – prompting outperformance of smaller stocks this week. Investors are still worried about valuations. These are stretched almost everywhere relative to history, but after a long upward trend, historical comparisons might not be the best guide. The fundamentals are improving but retail investors still aren’t buying the dip. The cryptocurrency sell-off might have something to do with that, since crypto owners have often been marginal equity buyers. Institutional investors that feel schadenfreude at crypto sell-offs should bear in mind that billions in lost value will inevitably impact stocks too.

Many UK investors that moved to cash ahead of the budget still haven’t bought back into markets – perhaps due to negative budget perceptions in Britain. That’s at odds with the market reaction; UK yields are below pre-budget levels and stocks are holding up decently. Retail stockbrokers have are concerned that those sitting in cash could miss out on the next leg up in global stocks.

The ingredients for a Santa rally are still here, but it’s not happening yet. Thankfully, after such a strong run for most of 2025, it isn’t needed.

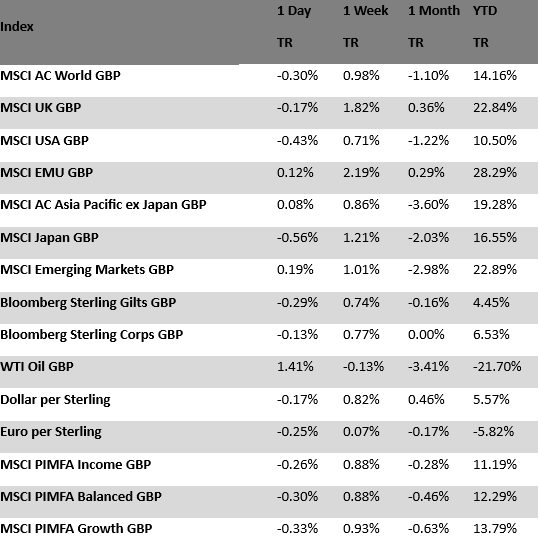

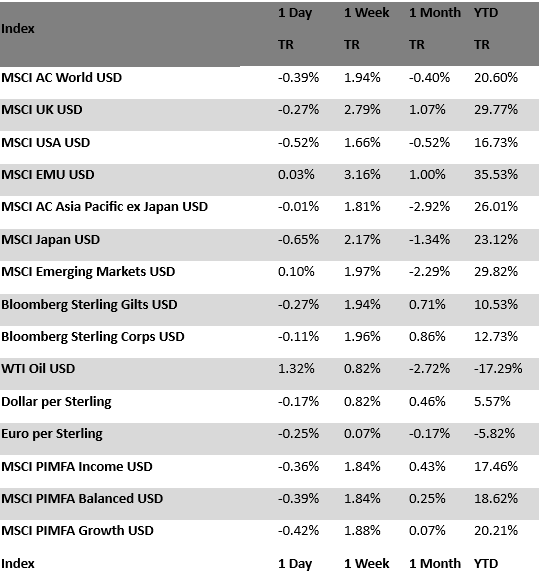

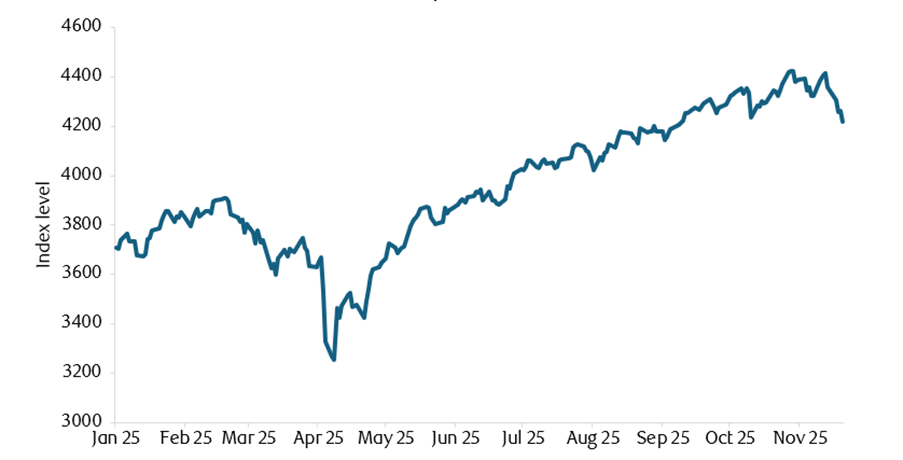

November Asset Returns Review

Global stocks were volatile in November but ended just 0.9% down in sterling terms. The longest US government shutdown ever ended midmonth – a relief for market liquidity, as it means money flowing back out of the Treasury General Account (TGA). US stocks recovered somewhat late November but still finished 0.6% down.

The lack of liquidity earlier in the month forced many retail investors to sell assets and crystallise profits from a strong post-April month. The sell-off was clearest in cryptocurrencies, but even Bitcoin stabilised into the end of the month. The Federal Reserve also helped by ending its quantitative tightening (QT) and signalling an interest rate cut in December. The Fed’s minutes suggested “strongly differing views”, but weak consumer data turned the balance dovish. The Bank of England and ECB also signalled lower rates.

That pushed down bond yields, with global bond prices (inverse of yields) gaining 0.2%. UK bond prices gained 0.1%, but with significant variation around the autumn budget (particularly the OBR’s accidental early release). There’s a disconnect between Britons’ negative view of the budget and positive reception from international investors: UK stocks gained, yields fell and sterling strengthened.

Nvidia posted strong Q3 earnings, calming AI bubble fears. They were replaced by fears of weak US consumer-focussed companies and the supposed “K-shaped economy”.

Japanese stocks lost 1.5% last month, yields rose and the yen weakened. This came after Prime Minister Takaichi’s tensions with China and pressure to loosen fiscal and monetary policy. But the Bank of Japan looks more likely to raise rates. China is keeping policy tight too, to strengthen the renminbi. Given Chinese weak economy, stocks fell 3.4%.

Overall, there was a notable role reversal from retail and institutional investors. Unlike earlier in the year, institutional investors are bullish while retail is nervous.

K-shaped economy

Everyone’s talking about the “K-shaped economy”. It’s the idea that most growth is coming from AI, while the rest of the economy languishes. You can see this in the stock outperformance of the ‘Magnificent Seven’ and the recent struggles of consumer-focussed US companies.

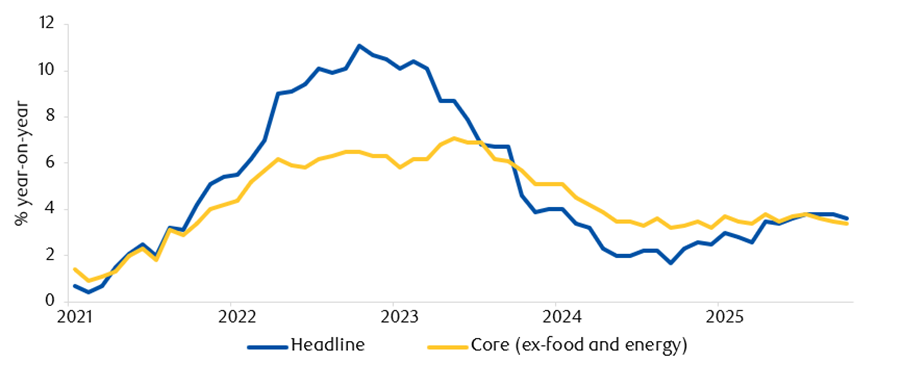

It’s not just about tech versus old industry; it’s also about improved spending power of high earners versus stagnation for lower earners. The FT questioned this aspect of the K-shaped economy (US wealth inequality hasn’t moved much in the last few years), but inflation affects lower income consumers differently – typically more – due what gets included in the headline price index. We suspect the popularity of the K-shaped narrative is that this disparity also ties into increasingly polarised politics.

It’s not just the US that’s K-shaped. Global manufacturing has struggled for years while global tech reaps the rewards of AI investment. The headache for monetary policymakers is that the struggling industries need lower rates, but that could overheat the debt cycle for tech companies. Trump’s tariffs are aimed at rebuilding that old industry. The AI capex race could bridge the divide itself, by dragging money from financial assets into the real economy. AI buildout requires significant infrastructure investment which we are already seeing – already benefitting energy companies, for example.

The AI capex race won’t magically fix political division and inequality (neither will tariffs) but in terms of the AI-v-others, the prospects are better. We’re already seeing a big infrastructure push, particularly in Europe, while AI-related profits are seemingly plateauing (at a high level) as tech competition intensifies.

The change of fortunes could also be helped by the recent role reversal from institutional and retail investors – the former now feeling more bullish than the latter. Institutional investors tend to prefer a bargain, which benefits lesser loved stocks. Markets, at least, might not stay so K-shaped.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Marcus Blenkinsop

8th December 2025