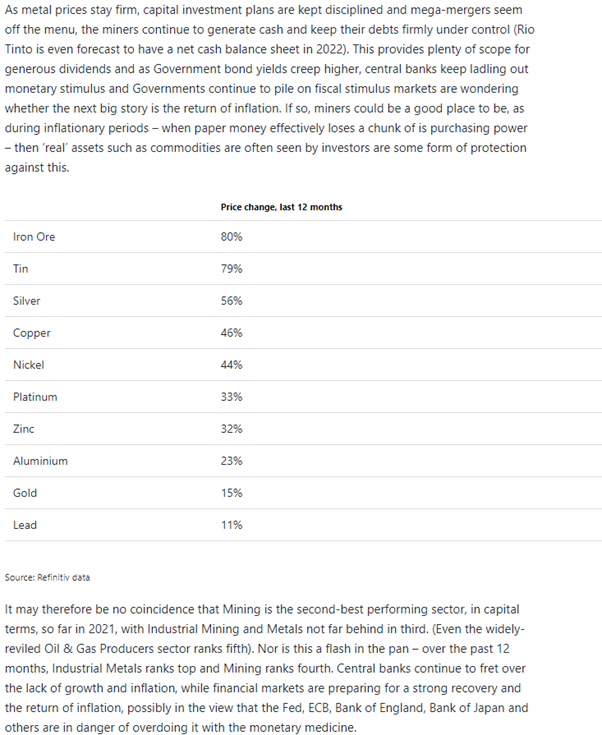

Please see below this weeks Invesco Investment Intelligence update – received this morning – 22/02/2021

Monday 22 February 2021 – update

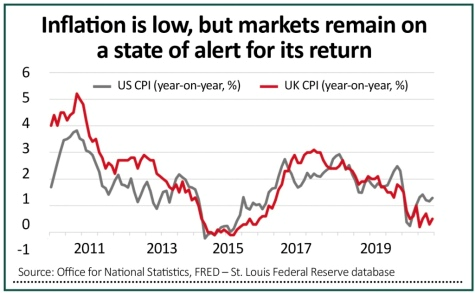

The diverging impact of virus containment measures on individual economies and the differing levels of fiscal stimulus was plain to see in US and UK January Retail Sales last week. The former exceeded expectations materially, growing 5.3%mom (see chart of the week), while the latter fell -8.2%mom, far worse than expected. With the vaccination rollout proceeding at a faster path in the UK (nearly 25% of the population have received a first shot compared to 12% in the US) and new cases, hospitalisations and deaths all declining sharply, the worst of the impact of the current lockdown may well be behind us, driving an easing of lockdown restrictions and some form of return to normality. Certainly, February’s Flash PMIs provided a more encouraging picture with the Composite rising from 42.6 to 49.8 on the back of a strong recovery in the dominant Services sector, hardest hit by recent lockdowns. Unfortunately, progress has been not as fast in other DMs, particularly Continental Europe (the weakening of the EZ’s Flash Services PMI reflected that) and prospects for EM look even less promising with vaccinations rates at just 0.1% across Africa and nearly 130 countries have yet to administer a single dose.

Money continues to flow into equity markets, but rising bond yields last week put a halt to progress in DM (-0.5%), which weighed on overall global returns (MSCI ACWI -0.4%). EM held up better and managed to eke out a small gain (0.1%). Weakness in DM was led by the US (-0.7%). YTD, EM (11.2%) have delivered more than double the return of DM (4.7%) and the region remains comfortably the most preferred market in the latest BofAML Global Fund Manager Survey. Small caps also declined (-0.5%), but here also performance diverged between DM (-0.7%) and EM (1.5%). They are up just under 10% YTD. At the sector level, commodity sectors made gains on rising oil and metals prices, with Energy (2.7%) ahead of Materials (1.3%), while Financials (1.8%) benefitted from rising bond yields and steeper yield curves. The reverse was true for defensive long duration sectors, such as HealthCare (-2.2%) and Consumer Staples (-1.2%), while IT (-1.2%) and Utilities (-1.8%) also underperformed. Against this backdrop Value (0.5%) was comfortably ahead of Growth (-1.2%), while Momentum (-1.8%) gave back some of its strong YTD outperformance. Despite a strengthening £, outperformance of the commodity and Financials sectors ensured that the UK outperformed (All Share 0.5%) on the back of a good relative week for large caps (FTSE 100 0.7%).

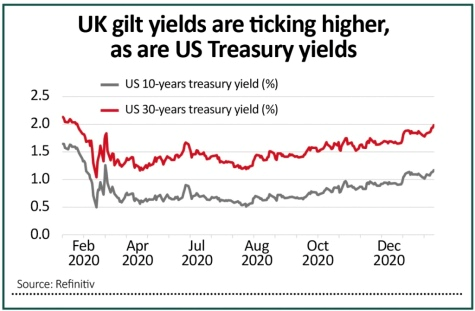

Upward momentum in government bond markets continued last week. The largest moves have been in the UST and Gilt markets, where the 10yr rose 15bp and 13bp respectively to their highest levels since last February (1.35% and 0.70% respectively). Yields are up 43bp and 50bp from their start of year levels and 85bp and 62bp from last year’s all-time lows. 10yr Bunds pushed higher too and after a 7bp rise to -0.31% are now up 26bp YTD and 53bp from their all-time lows. Even Italian BTPs, the star performer in recent weeks, saw yields rise 9bp. Unsurprisingly returns were negative with the Gilt index hit hardest due to its longer duration (12.4 years). IG suffered against a backdrop of higher government yields with weakness across the board, again led by longer duration £ markets (8.5 years). Globally spreads narrowed 3bp, but yields rose 6bp. HY continued to outperform in credit, as spreads narrowed 8bp and the YTM fell 2bp to an all-time low 4.6% (Yield to Worst is 4.05%).

The US$ was broadly flat on the week with the US$ Index down just 0.1%, leaving it up 0.5% YTD. Vaccination progress helped £ to its best week versus the US$ since mid-December, breaking through the $1.40 level for the first time since Q2 2018. It also gained against the Euro, moving above the €1.15 level for the first time since last March. Economically sensitive commodities continued to make gains. The Texas storm’s impact on US production helped push oil to new post-pandemic highs and it is now up 23% YTD. Copper, up 7.1% for the week, extended its surge to a new nine-year high amid warnings of a historic shortage as the global economy starts to recover. After its best year for a decade last year, Gold is off to its worst start in 30 years, falling further last week (-2.3%) and down just under 6% YTD. Rising UST yields aren’t helping as investors take profits and rotate into economically sensitive commodities. Even rising inflation expectations aren’t helping the metal.

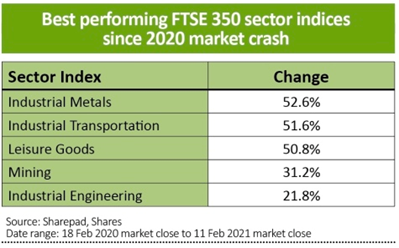

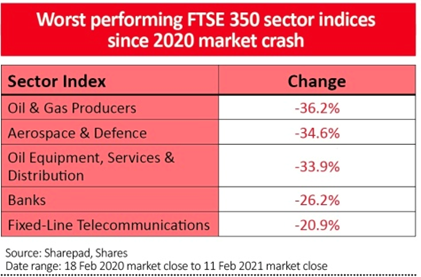

Market performance last week (%)

Past performance is not a guide to future returns. Sources: Datastream as at 21 February 2021. See important information for details of the indices used.1

YTD market performance (%)

Past performance is not a guide to future returns. Sources: Datastream as at 21 February 2021. See important information for details of the indices used.1

Chart of the week: US Retail Sales (mom%)

Past performance is not a guide to future returns. Source: Datastream as at 18 February 2021.

• The direct impact of fiscal stimulus on the US economy was clearly highlighted in last week’s surge in Retail Sales for January. The headline number rose 5.3%mom – the first monthly gain since September, the largest rise in seven months and beating consensus expectations of a 1.1%mom rise by a considerable margin. Only last May have expectations been beaten to such a degree. This leaves them 5.8% higher than a year ago (and remember that was compared to a pre-pandemic economy) and a far faster recovery than in previous cycles.

• What drove the strong rise in sales? There was a seasonal boost following weaker than normal holiday spending in December, while the easing of virus restrictions clearly played a role too. However, the general consensus is that the renewed income support from the $900bn end of year fiscal package has been the dominant factor as the income dispersion of the spending was mainly driven by lower-income groups, the main beneficiaries of that package and historically where the propensity to spend any stimulus is the greatest. In that package most Americans received payments of $600 (up to $75k income and then tapered to no payment at $99k) with eligible families also receiving $600 per dependent child. These payments were made in early January. Monthly unemployment payments were also boosted by $300 per week for 11 weeks.

• And this is not the end of support for US households and consumption. Biden’s $1.9trn “American Rescue Plan”, currently going through Congress, is likely to see further payments to individuals of up to $1400 and $400 per week in additional unemployment payments. On current expectations these are likely to be paid out from mid-March. And on top of that, with “excess” savings as a consequence of the pandemic estimated by Goldman Sachs to hit $2.4trn by the middle of the year, there should be a further boost to spending from this source as the economy returns to some sort of normalcy. Even if Goldman’s estimate that under 20% of that will be spent, partly down to a large proportion of those “excess” savings being held by higher income groups, who are far less likely to spend it, that would still be enough to contribute roughly 2% to GDP growth, although Goldman’s attach a high degree of uncertainty to this number.

• It’s perhaps no wonder that consensus expectations for consumer spending are higher in the US (5.2%) in 2021 compared to both the EZ (3.9%) and UK (4.3%), which in turn should underpin a stronger recovery in Real GDP.

Key economic data in the week ahead

• Not a lot on the data front this week, so focus may well be elsewhere: on progress of the upcoming US stimulus package, Powell’s testimony to the US Congress and developments on the virus front, where the PM will be announcing his roadmap for easing restrictions in England and the EU Council meets at the end of the week.

• In the US on Tuesday the Conference Board Consumer Confidence index for February is forecast marginally higher at 90 from 89.3, but remains close to post-pandemic lows and a long way below the 133-level seen last February. Last week’s Initial Jobless Claims were higher than expected at 861k, a sixth consecutive week of more than 800k despite a drop in coronavirus cases. Thursday’s reading is expected at 840k, a modest improvement. Friday’s Personal Income data for January is estimated to have had a strong boost from additional stimulus payments. Incomes are estimated to have increased 10%mom. Friday also sees PCE Inflation data released with the closely watched Core reading expected to show a 0.1%mom increase, leaving it at 1.4%yoy.

• In the UK the Unemployment rate is forecast to have increased to 5.1% at the end of December when data is released on Tuesday, up from 5% in November. This would be the highest level of unemployment since October 2015.

• In the EZ, Germany’s Ifo Business Confidence for February is released on Thursday. After last week’s Flash Composite PMI showed a marginal improvement, a similar outturn is expected with a rise to 90.5 from 90.1, led by future expectations rather than current conditions.

• In Japan Industrial Production and Retail Sales for January are published on Thursday. The former is forecast to show a rebound to 3.9%mom, leaving it down -5.4%yoy, while the latter is expected to see a -1.3%mom decline, leaving it down -2.6%yoy. The expansion of the state of emergency beyond Tokyo the main culprit there.

• In China the Loan Prime Rate, the reference point against which banks price loans, is set on Monday. It was last changed in April 2020 and is expected to remain unchanged at 3.85% and 4.65% for the 1-year and 5-year rate respectively.

Please continue to check back for our latest updates and blog posts.

Charlotte Ennis

22/02/2021