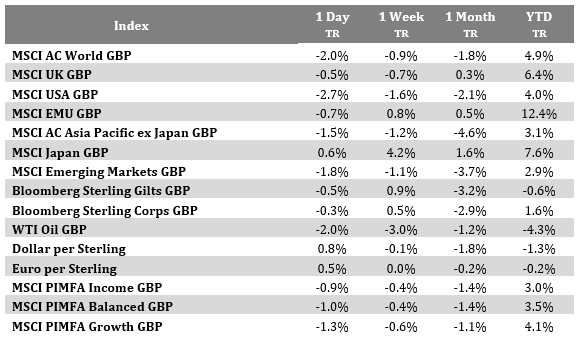

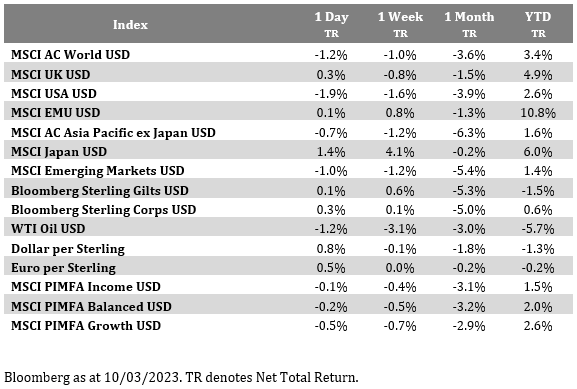

Please see below todays (10/03/2023) Daily Investment Bulletin from Brooks Macdonald:

What has happened?

Earlier on Friday, the Bank of Japan (BoJ)’s last meeting under outgoing Governor Kuroda was the epitome of a non-event. There was no change to its -0.1% interest rate, no change to the +/-50bp tolerance band around its 0% target for 10-year JGB yields, and nothing in the accompanying BoJ statement that would suggest an imminent end to yield-curve-control. Instead, market volatility has centred around falls in the US banks sector on Thursday, led by a -60.41% share-price fall in SVB (Silicon Valley Bank) Financial Group, a California-based firm specialising in funding to venture-capital-backed companies to the tech sector. The turmoil started late Wednesday when SVB Financial Group announced a $2.25bn share-sale to shore up capital after being hit by loses on its securities portfolio. Negative sentiment spread across the US bank sector yesterday, even including far-better-capitalised banks, with JP Morgan shares off -5.41% on the day. The SVB news was also seen driving a risk-off move in US Treasuries, with 2 year yields down -20bps to 4.87%, its biggest daily fall in over 2 months, and the ‘10-year less 2-year’ yield spread steepened up through -1%, closing at -97.3bps on Thursday. Closer to home, this morning, we’ve seen UK GDP for January come in at +0.3% month-on-month, better than the +0.1% market consensus expected.

US jobless claims gives some support to the bulls

Thursday saw US weekly Initial Jobless Claims data, which showed that claims had risen to 211,000 during the week ending Saturday 4th March. That was higher than market estimates for 195,000, and up from 190,000 the week before. It also marked the first time claims has come in above 200,000 since early January. Cutting the data another way, the week-on-week gain in claims of 21,000 was the biggest weekly gain in 5 months, since October last year. That said, whilst this is a pick-up in claims, it’s coming from a low base. For context, the US labour market remains tight, with the US JOLTS (Job Openings and Labor Turnover Survey) data out earlier in the week showing that there was still a ratio of 1.9 job openings for every 1 unemployed person in January – that’s down from 2.0 in December last year, but well above the circa 1.2 level before the pandemic.

US non-farm payrolls

Today sees the first instalment of a double-header of crucial data that could tip market expectations (and the Fed for that matter), either towards a 25bp or 50bp hike on 22 March. US non-farm payrolls are due at 1:30pm UK time, and the Bloomberg market consensus is looking for a month-on-month gain of 225,000 (which incidentally is up from an earlier 215,000 estimate at the start of this week). Meanwhile, the unemployment rate is expected to stay unchanged at a 53 year low of 3.4%. Within the release, average hourly earnings are expected to be up 0.3% month-on-month, the same as last month’s gain. After today, markets will be looking ahead to the US CPI (Consumer Price Index) print due next Tuesday.

What does Brooks Macdonald think

After a run of stronger economic data recently, markets are firmly in the mindset of ‘bad-news-is-good-news’. That’s to say, bad news for the economy translates as reducing the urgency of central banks to hike interest rates, and that would be good news for risk assets. So, will markets get some bad economic news today? To be fair, it all feels a bit US-centric right now in terms of the news flow, but we won’t have long to wait to see if the US jobs data later today, or the US CPI data on Tuesday next week plays ball.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Carl Mitchell – Dip PFS

Independent Financial Adviser

10/03/2023