Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 17/06/2026.

Is the end in sight for the Strait of Hormuz blockade?

The U.S. and Iran are close to a deal that could reopen the Strait of Hormuz and bring oil prices down.

Key highlights

- Geopolitical volatility: Markets experienced ‘whiplash’ as Middle East tensions escalated before a sudden ceasefire announcement.

- Central bank divergence: The European Central Bank (ECB) raised rates to combat inflation, while the U.S. Federal Reserve (the Fed) and Bank of England (BoE) are expected to hold steady.

- Asset class shifts: Treasury yields are drifting higher amid AI-driven demand, creating headwinds for gold despite its long-term appeal.

From escalation to “the war is over” – a week of whiplash

There’s been some drama in markets recently. As a reminder, investors began last week scarred by a sharp sell-off in technology stocks and fears that U.S.-Iran ceasefire negotiations seemed to have stalled.

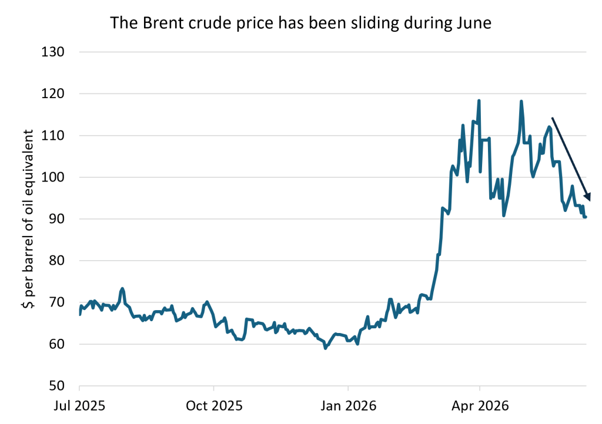

In the week after the sharpest drop in NASDAQ this year, sentiment was weak but the trend that developed was one of progress towards a deal that could open the Strait of Hormuz. This would take some pressure off the very tight markets for energy and associated industrial chemicals. But it wasn’t without setbacks. Iran downed a U.S. helicopter, the U.S. launched retaliatory strikes, and Iran struck back. Both sides maintained, seemingly implausibly, that the ceasefire remained in place. Energy prices barely flinched.

Then on Thursday evening, the tone shifted dramatically. President Trump declared the war over and suggested a deal could be signed as soon as the weekend. Iran was more cautious, noting that no conclusion had been reached and that the U.S. had raised new demands. By Friday morning, oil was at its lowest since April, bond yields had fallen sharply, and equities were firm across Europe following a strong U.S. session.

Source: LSEG

For portfolios, the implications cut both ways. Lower oil prices ease inflationary pressure globally and reduce input costs for businesses, but they create a headwind for the energy-heavy FTSE 100, which closed near 10,400. The domestically focused FTSE 250 traded cautiously all of last week, caught between the benefit of lower energy costs and the reality of sustained high borrowing rates. U.S. equities, particularly in technology and semiconductors, rallied hard as the geopolitical risk premium unwound and AI-related earnings momentum continued.

The ECB hikes – and it won’t be the last

The ECB became the first major central bank to raise rates in response to the oil shock, lifting its policy rate by 25 basis points to 2.25%. President Lagarde noted that the energy shock was broadening throughout the economy, with indirect costs now becoming evident. The ECB’s updated projections revised inflation higher and growth lower – but it’s clearly prioritising price stability, its sole mandate. The ECB now sees core Consumer Price Index (CPI) remaining above 2% at least through 2028.

Two further quarter-point hikes are priced into overnight index swaps, and there’s no obvious reason to think those odds are wrong. Eurozone unemployment remains near an all-time low, and household balance sheets remain resilient – the debt service ratio sits at its lowest since the late 1990s.

The ECB appears confident that moderate tightening won’t crush the economy. That said, growth momentum has clearly weakened relative to the U.S., and wage growth at just over 2% remains muted. Without a major re-acceleration in energy prices, aggressive hiking seems unlikely. The Fed and BoE both meet next week – neither is expected to hike, as their policy rates remain above neutral, unlike the ECB’s pre-meeting position. The UK is expected to raise rates this year but not until September.

Treasury yields – conditions still point towards higher yields

Several Fed officials have pushed back against the idea that AI-driven productivity gains justify rate cuts. New Chair Kevin Warsh’s view that AI is disinflationary appears to be a long-term thesis at best; in the near term, soaring demand for electricity, memory chips and the wealth effect from rising equity markets are all inflationary.

With growth momentum improving, the AI capex boom continuing, and bond supply increasing as government debt-to-GDP rises, yields are more likely to drift higher than lower – though many investors have already bet on higher yields, leaving limited room for further moves upward.

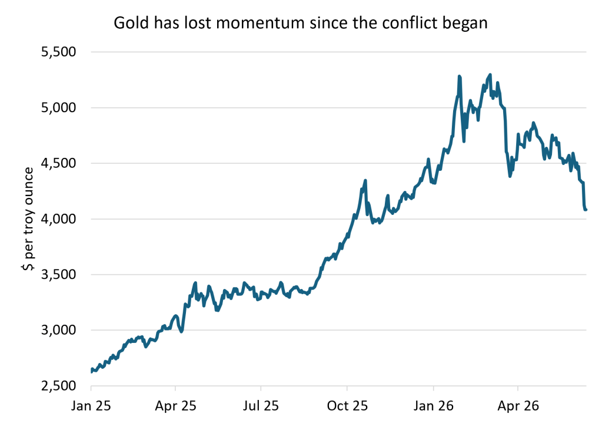

Gold loses its shine

Source: LSEG

The inverse correlation between gold and Treasury yields has reasserted itself, and with yields likely to drift higher, that’s a headwind.

Gold now trades as a very risk-on asset – its volatility exceeds that of the S&P 500 – leaving it vulnerable to outsized losses in any broader market sell-off. A rising oil price would strengthen the dollar, another negative for gold, and would pressure major importing nations like Türkiye and India to implement policies that weigh on aggregate demand for the metal. The technical picture has also deteriorated, with an emerging pattern of lower highs and lower lows. Interestingly the recent drop in oil has not helped the gold price much. Unlike other asset classes where lower valuations can entice new investors, with gold it seems sensible to moderate exposure until a more positive trend emerges.

This doesn’t represent a structurally negative view. The long-term case – central bank diversification away from Western assets, China’s reserves still below 10% in gold, and scope for dollar depreciation over time – remains intact. China has been making contrarian purchases during this period of gold price weakness. But tactically, the balance of risks no longer seems supportive.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Charlotte Clarke

18/06/2026