Please see the below article from Brooks Macdonald detailing their discussions on markets. Received this afternoon 02/04/2026.

What has happened?

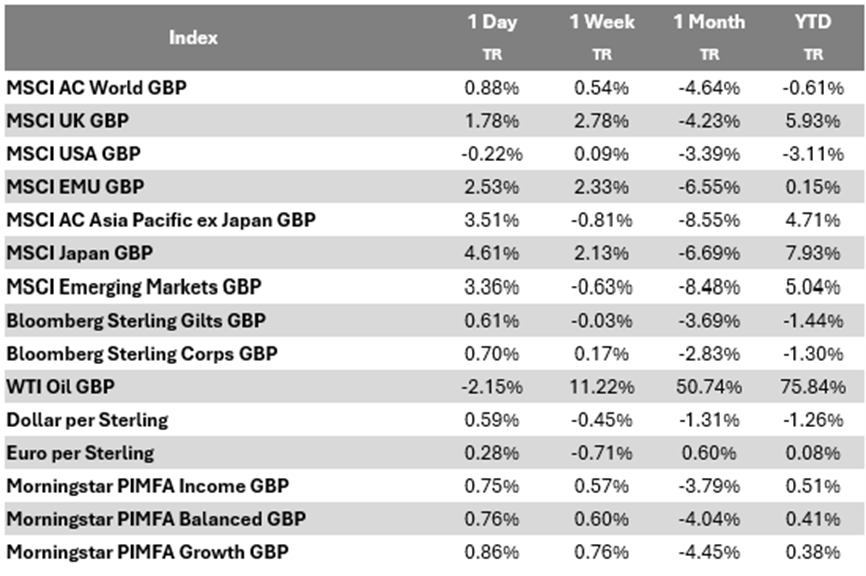

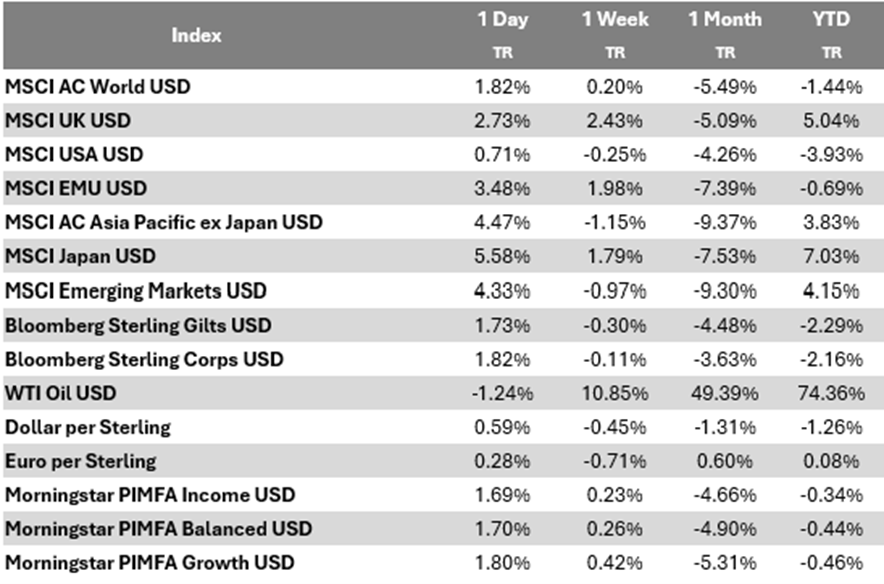

Global equity markets extended their rally yesterday, led once again by US tech stocks. The S&P 500 rose +0.72%, with the NASDAQ (+1.16%) and the Mag 7 (+1.37%) outperforming. European markets played catch up to Monday night’s US gains, recording sharp advances across the region. The STOXX 600 (+2.50%), DAX (+2.73%) and FTSE 100 (+1.85%) all posted their largest daily gains since last April. The risk on mood also spilled over into bond markets, helped by easing energy prices. Natural gas prices fell sharply, with front month TTF futures down -5.49% to €47.51/MWh, the lowest level since early March. As a result, government bond yields declined, with 10 year bund yields falling -1.8bps to 2.98%, while UK gilt yields dropped more sharply after a downward revision to the UK manufacturing PMI. Elsewhere, euro area manufacturing data was revised slightly higher, pointing to resilience despite recent energy price volatility.

Trump rhetoric offered little reassurance

Market sentiment has weakened overnight after President Trump’s widely anticipated address offered little clarity on the timing or conditions for ending hostilities with Iran. While suggesting the military operation was “very close” to completion, he also warned of further escalation if negotiations fail, with no clear signal of an imminent off ramp. The US again emphasised that safeguarding shipping through the Strait of Hormuz should fall largely to other nations. In response, Brent crude rose sharply and is trading above $107 this morning. Meanwhile, the UK is set to convene talks with around 35 countries to discuss restoring shipping routes, highlighting the growing role of US allies in managing regional fallout. Separately, renewed commentary around a potential US withdrawal from NATO briefly drew attention, though significant political hurdles remain.

What does Brooks Macdonald think?

Attention now turns back to US economic data, particularly the labour market, which remains a key anchor for market expectations. After yesterday’s firmer than expected ISM manufacturing reading and stronger ADP employment data, investors will be watching today’s weekly jobless claims and Friday’s non farm payrolls report closely, even as many global markets are closed for Good Friday. With inflation pressures still present and energy prices volatile, incoming labour market data will be important in shaping views on the resilience of the US economy and the path for monetary policy.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Alex Clare

02/04/2026