Please see below an article received from Brooks Macdonald today 17/03/2023 which provides their views on recent global market events:

What has happened

Equities stabilised, then rallied yesterday as investors concluded that contagion risks were receding in the aftermath of the SVB and Credit Suisse issues.

Bank crises

Shares in First Republic Bank, a regional US bank considered to be one of the most exposed to a SVB-style event, opened lower yesterday but started to recover as reports suggested that a support package was imminent. Just before the market closed, a consortium of major US banks contributed $30bn of uninsured deposits to First Republic. First Republic announced after the market close that it would be suspending its dividend and will be seeking to repay some debt instruments. Credit Suisse equity rallied yesterday after the overnight news that the bank would be using a Swiss National Bank liquidity facility to meet near-term liabilities. The bond market was less impressed however with credit default swaps, effectively an insurance contract on the bank’s debt, remaining elevated and their bonds remaining under pressure.

ECB meeting

The ECB chose to follow through on its pre-announced 50bp interest rate hike despite the meeting coming within the midst of the current banking sector turmoil. Arguably the outsized hike was a ‘dovish’ move in that the ECB made no future commitment to the path of interest rates, stressing a data-dependent approach going forwards. This is no real surprise as the ECB must have felt boxed in by their previous 50bp guidance and one wonders whether they would have proceeded with that larger hike without the prior commitment. The ECB said that it was monitoring the current market volatility closely, adding that the ‘euro area banking sector is resilient, with strong capital and liquidity positions.’

What does Brooks Macdonald think

With the ECB meeting out of the way, investors are already looking ahead to the Fed meeting next week with markets broadly pointing to a 80% probability of a 25bp move and 20% probability of no change at all. With the Treasury market the release valve for SVB tensions over the last week, as some of the immediate fears have subsided the yield curve is unwinding its emergency pricing with the 2-year yield up over 25bps yesterday alone. The other important change has been a heavy revision of the number of Fed rate cuts expected in the second half of this year, with bond investors now pricing in a longer pause and decline after the Fed reaches its terminal rate.

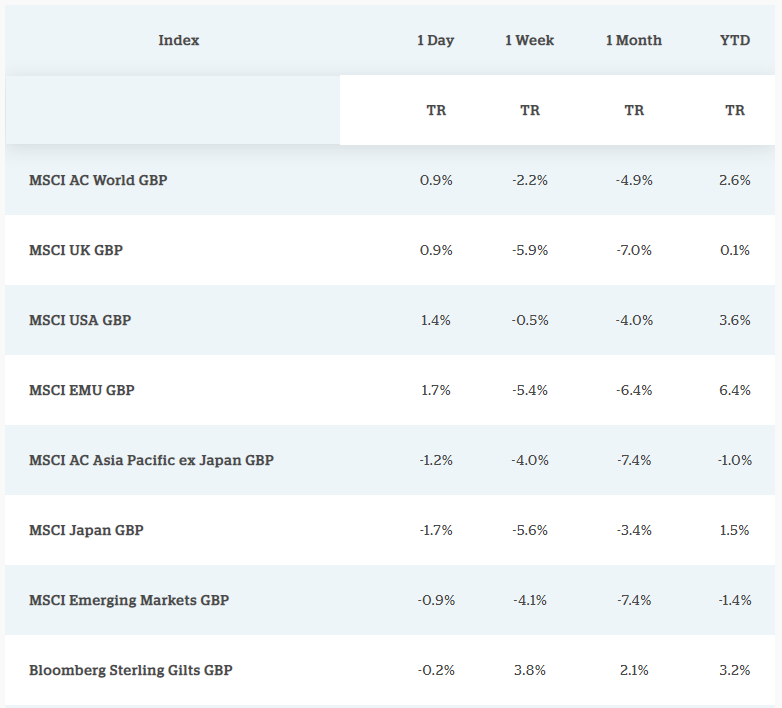

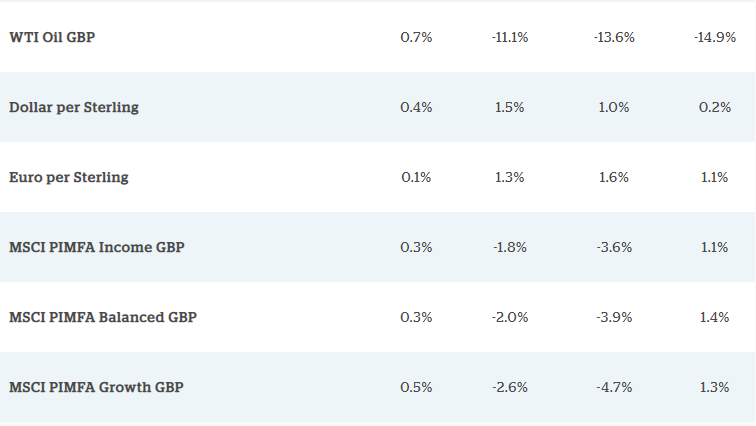

Bloomberg as at17/03/2023. TR denotes Net Total Return

Please check out blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses

Adam Waugh

17/03/2023