Please see below, Evelyn Partners’ Investment Outlook providing a monthly round-up of global markets and trends. Received Friday afternoon – 06/01/2023

Playing the field for yield in 2023

2022 was a tumultuous year for financial markets. Both bond and equity prices fell sharply, a rare and unwelcome occurrence for multi-asset investors, as central banks moved abruptly to more aggressive monetary policy to address the highest inflation seen for 40 years.

Given the volatility seen in financial markets, in 2023 we expect investors to remain defensive and seek income-yielding securities backed by reliable cashflows to protect against potential further falls in markets. Excluding the pandemic, the good news is that the sell-off has led to the widest dispersion of dividend yield in global stocks for 13 years. In other words, dividend yields are high and there are more companies paying attractive yields. Assuming dividends are not cut, this is a time to play the field for yield and lock in the income they provide.

Our analysis finds the highest one-year forward dividend yields are in the energy sector at 4.1%. This is supported by elevated energy prices and capital expenditure discipline. Defensive areas of the equity market (e.g. consumer staples and utilities) and materials also score well on this front. This is in stark contrast to the low-yielding information technology, consumer discretionary and communications services sectors — which all pay dividend yields of less than 1.6%. There is an opportunity cost for sticking with such low-yielding stocks when short-term interest rates have risen and offer a higher return.

We see similarities in stock markets across different geographies. UK equities are expected to pay a dividend yield of 4.3%, the highest out of the major developed stock markets. This is supported by healthy company cashflows. The US, in contrast, is the lowest yielding market on 1.7%. Throughout 2023 we expect money to continue to flow into cashflow-backed income yielding assets, such as UK large-caps.

Once the US Federal Reserve (Fed) stops raising interest rates, possibly by the summer of 2023, it may provide a chance to acquire government bonds where yields are up from a year ago and economic growth is slowing. A Fed pause may also be a catalyst for Asian (ex-Japan) stocks should it weaken the US dollar, which would help encourage capital to flow back to the region. An improving situation in China, driven by the end of its zero-Covid policy, is another reason why Asian stocks could outperform global markets in 2023.

Balancing market headwinds and tailwinds

The stock market outlook still appears uncertain. Investors face plenty of headwinds, including lower global growth following interest-rate hikes and the cost-of-living crisis. Oxford Economics projects subdued global real GDP growth of 1.2% in 2023, well below the 2.9% estimated for Investment outlook Playing the field for yield in 2023 2022. For investors, slower growth implies a downside risk to the consensus estimate of 3% Earnings Per Share growth for the MSCI All Country World equity index.

There are also plenty of geopolitical concerns for investors to consider. For instance, Washington raised tensions with Beijing by imposing an effective ban on US tech companies exporting high-spec chip-manufacturing equipment to China on 7 October. Meanwhile, the Chinese military has held increasingly aggressive operations close to the borders of Taiwan. While there seems no sign of easing in Sino-US tensions, at least there are no scheduled presidential or general elections in G7 countries over the next year — the first time that has happened this century. This provides some stability and may help to ease political uncertainty.

In spite of choppy markets there are tailwinds to lift equities higher. Inflation is set to peak around the globe, giving central banks room to ease off from raising interest rates. Our analysis of the last six Fed hiking cycles shows that US stocks rose by 18%, on average, over the 12 months following a pause in rate increases.

Another tailwind would be if growth surprises on the upside. A lot depends on China. The Chinese authorities have largely scrapped their zero-Covid policies in response to the social unrest seen in many cities. With plenty of stimulus pumped into the economy already, Oxford Economics expects China’s real GDP growth to accelerate to 4.2% in 2023 from 3.1% in 2022.

And finally, US CPI inflation has come in below market expectations in the last two months, with the majority of economists anticipating a steady slowing throughout 2023. As inflation decelerates, real take-home pay (and spending) can be expected to recover. US household balance sheets are in decent shape following years of debt reduction since the Global Financial Crisis in 2008. Furthermore, consumers also have aggregate ‘excess’ personal savings built up since the pandemic of around $2 trillion (circa 10% of take-home pay), which can help to cushion the rise in the cost of living.

In our view, much of the bad news is now baked into global stock market valuations. The MSCI All Country World index trades at an undemanding price-to-earnings ratio of 15 times, well down from the cyclical peak of 20 times in September 2020. This creates a favourable platform for higher dividend-yielding stocks to perform in 2023. Nevertheless, expect plenty of market volatility as the global economy nurses its way through an inflationary hangover.

Market Highlights

Equities

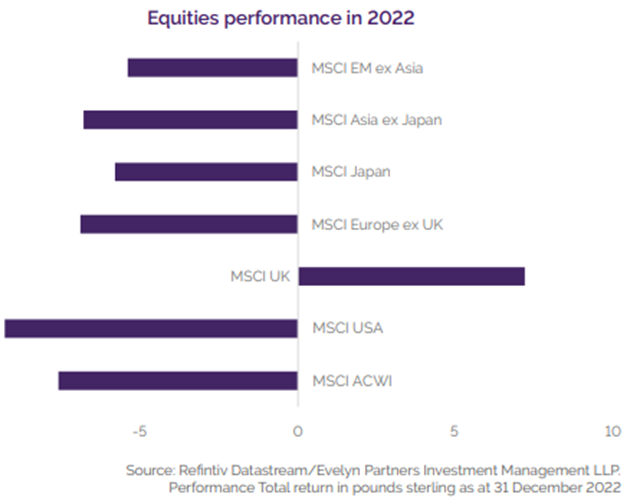

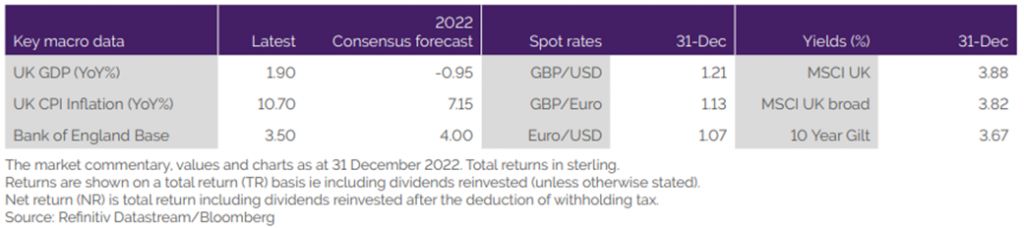

2022 was a year fraught with macro headwinds resulting in the worst performance of global equities since 2008. Rampant inflation prompted central banks to implement aggressive interest rate hikes that saw sensitive growthoriented stocks fall from the high valuations seen at the end of 2021. The US bore the brunt of this. MSCI USA fell 9.3, with the mega caps (Apple, Microsoft, Amazon, Tesla, Alphabet and Meta Platforms) falling, on average, by 42.2%. The war in Ukraine further compounded economic uncertainty and the resulting energy crisis contributed to Europe falling 6.9% over the year. Asian equities were not immune with China’s zero-Covid policy and the strong US dollar hampering growth in the region. Despite the troubling economic backdrop, the UK stock market returned 7.2%, substantially outperforming its peers. This was due to its bias towards defensive ‘value’ sectors such as healthcare, consumer staples and materials as well as a large exposure to the energy giants, BP and Shell.

Fixed income

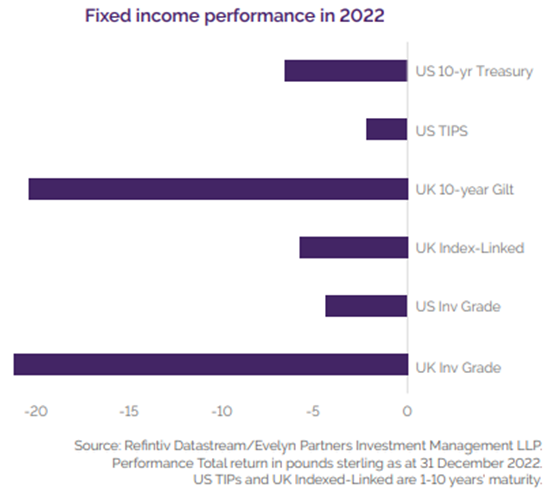

Government bonds did not offer protection during 2022 and posted one of the worst years on record. Rampant global inflation and accompanying interest rate hikes saw bond yields soar across both UK gilts and US treasuries. Longer duration assets performed poorly, with the US 10-year treasury falling 6.5% in sterling terms. The UK gilt market had a particularly turbulent year following Kwasi Kwarteng’s ‘mini-budget’. 10-year gilts were briefly down 24.4% and ended the year down 20.1%, their worst performance since 1974. Corporate bonds faced similarly poor performance, with US and UK investment grade bonds falling 4.3% and 20.9%, respectively in sterling terms. Both treasury inflation protected securities (TIPS) and inflation linked gilts failed to offer protection in the face of rising inflation, with rapid interest rate rises causing real interest yields to rise. US TIPS performed only slightly better down 3.0% in sterling terms, whilst UK index-linked fell 5.2%. The weak pound helped shield sterling investors from some of the negative returns in dollar denominated assets.

Currencies and commodities

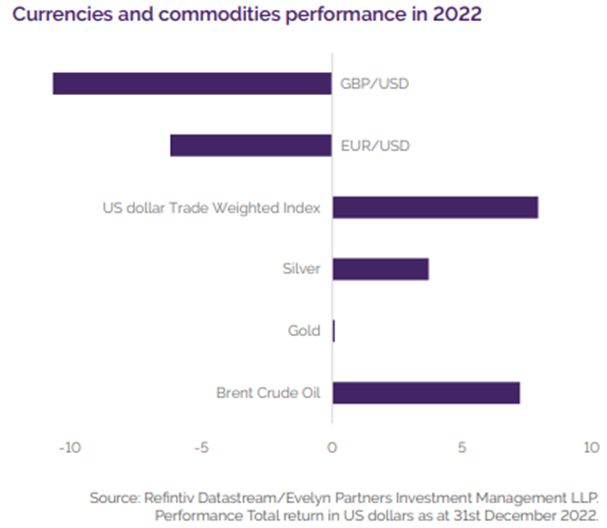

2022 was a volatile year for both currencies and commodities. Crude oil was up 37.4% by the end of first quarter, as Covid fears faded and western sanctions on Russia were imposed. However, Brent crude finished 2022 up 7.2% in US dollar terms as demand wilted under the threat of a global economic slowdown, despite OPEC+ announcing cuts to output. Gold remained largely flat in US dollar terms. Its initial strength, due to geopolitical uncertainty, was dampened by aggressive US Federal Reserve interest rate hikes. This resulted in the US dollar Trade-Weighted Index increasing 7.9% to a 20-year high as investors flocked to the greenback as a ‘safe-haven’ currency in the face of economic uncertainty. The euro found parity with the US dollar during 2022, before recovering slightly as the dollar’s strength eased. Sterling fell from $1.35 to $1.21 but found an all-time low of $1.037 following Kwasi Kwarteng’s ‘mini budget’.

Market commentary

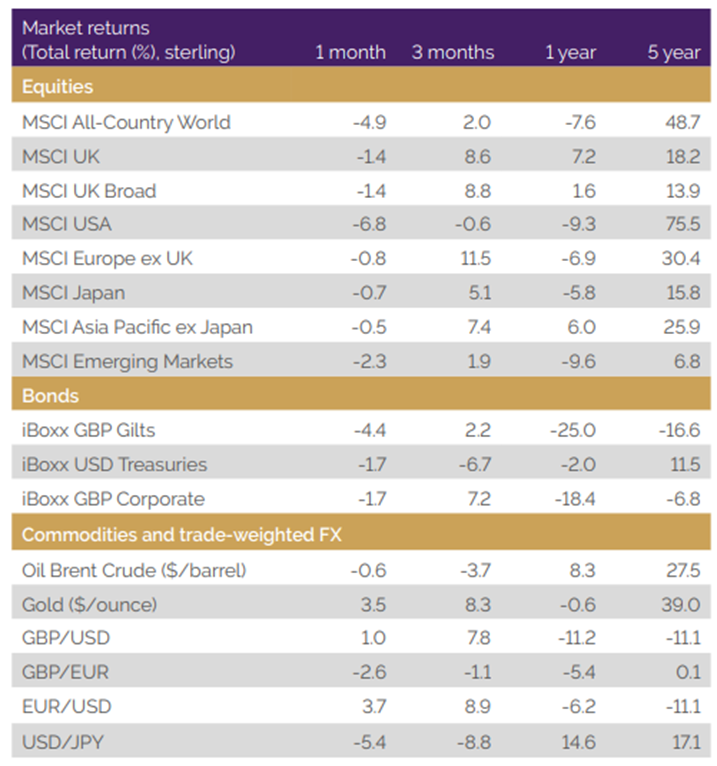

Equities were down across the board to close out the last month of 2022 with MSCI All-Country World down 4.9% in sterling terms. December’s Federal Reserve meeting pointed to interest rates remaining higher for longer than the market had previously expected which weighed on the outlook. MSCI USA was the worst performer of the month, down 6.8%. Asia Pacific was the best performer. News of lockdown restrictions easing in China and a weakening US dollar were both positive catalysts for the region. Interest rate expectations moving up similarly weighed on fixed income with gilts down 4.4% and treasuries down 1.7% on the month, in sterling terms. Gold was up 3.5% for December and over the year fell by 0.6%, despite periods of rising interest rates traditionally favouring income producing assets. The US dollar continued to weaken through December with sterling and euro up 1% and 3.7% respectively.

Please continue to check our Blog content for advice, planning issues and the latest investment, markets and economic updates from leading investment houses.

Alex Kitteringham

9th January 2023