Please see below, Brooks Macdonald Daily Investment Bulletin, covering the impact of global key market events. Received this afternoon – 05/01/2023

What has happened

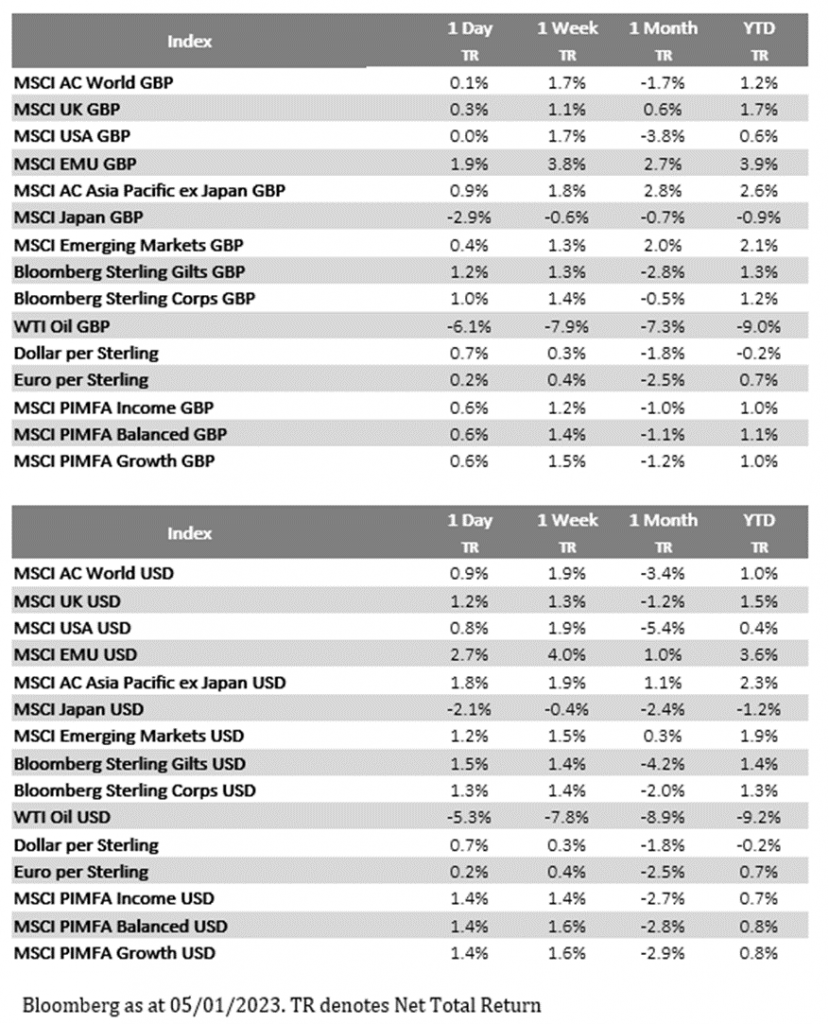

Equities received another boost yesterday after the French inflation numbers missed and US ISM manufacturing data came in at its weakest level since April 2020. Concerns over US labour market tightness caused Europe to outperform US indices for the second day running.

Inflation

Yesterday saw the release of the French inflation numbers which, using the EU-harmonised measure, came in at 6.7% against market expectations of 7.3%. We have the full Euro Area release tomorrow but given France, Spain and Germany have all been lower than expected, this bodes well for a weaker than expected inflation figure to support European risk appetite. The bond market was quick to reduce the number of ECB hikes expected in 2023 as a result. Looking further ahead, energy prices will be a key input for European inflation numbers. There was pleasing news here yesterday with European natural gas futures falling to a one-year low on the back of unseasonably warm temperatures in Europe which has curbed demand. Oil prices also fell yesterday which should also help ease broader energy prices at the start of the year.

US jobs data

The US labour market data was less supportive of equities however, with the US JOLTS report pointing to a very tight labour market. Job openings came in at 10.458m, higher than the expected 10.05m with the previous reading also being revised higher. This means that there are 1.74 job openings for every unemployed US worker, a significantly higher number than the pre-pandemic average of 1.2. Lastly the quits rate, measuring those voluntarily leaving their jobs, also picked up in November, suggesting that bargaining power is still intact.

What does Brooks Macdonald think

The FOMC minutes, also released yesterday, stressed that the central bank would continue to raise rates until inflation was confirmed as under control. The committee discussed the labour market, noting its strength, and therefore the JOLTS figures will confirm to the more hawkish members of the committee that more needs to be done. The FOMC actually explicitly called out the risk of ‘an unwarranted easing in financial conditions, especially if driven by a misperception by the public of the committee’s reaction function, would complicate the committee’s effort to restore price stability.’ Effectively saying that the Fed was worried that markets will take an overly dovish interpretation of the recent inflation data, causing financial conditions to loosen earlier than the Fed wants. In the short term therefore, expect the Fed to continue with their tougher rhetoric.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Cyran Dorman

5th January 2023