Please see below, a ‘Markets in a Minute’ article from Brewin Dolphin covering the key market news from around the world. Received this afternoon – 29/12/2022

Stocks were mixed last week in the run up to the Christmas break.

The Dow ended the week up 0.86%, but the S&P 500and Nasdaq both fell, 0.20% and 1.94% respectively, primarily driven by concerns in the tech sector. This did not prevent the FTSE100 ending up 1.92% and the Stoxx 600 and Dax 0.64% and 0.34% respectively in Europe.

In Asia the Hang Seng ended up 0.73% but the Shanghai Composite was down 3.85%, hit heavily by concerns resulting from increased reports of coronavirus cases.

In Japan the Nikkei was down 4.69%, following the surprise announcement of changes to the yield curve control (YCC) policy earlier in the week.

Last week’s market performance*

• FTSE 100: 1.92%

• S&P 500: -0.20%

• Dow: 0.86%

• Nasdaq: -1.94%

• Dax: 0.34%

• Hang Seng: 0.73%

• Shanghai Composite: -3.85%

• Nikkei: -4.69%

• Stoxx Europe: 0.64%

* Data from close on Friday 16 December to close of business on Friday 23 December.

Investors weigh China’s Covid impact

Since markets were closed for the Christmas holiday, investor sentiment has ebbed and flowed in response to increased Covid cases in China. Tuesday’s announcement by the Chinese authorities of relaxed border restrictions gave confidence that tangible steps are being taken to reopen China’s economy. However, this optimism was muted by continuing concerns regarding the numbers of new Covid cases, particularly into Wednesday and Thursday as a growing number of countries imposed testing requirements on arrivals from China.

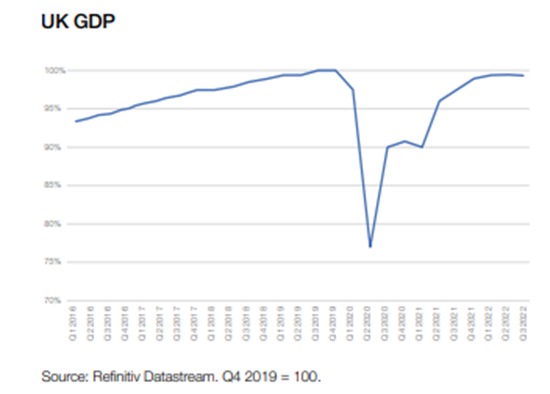

UK economy shrinks more than expected

Figures published by the Office for National Statistics (ONS) last week showed the UK economy contracted by more than expected in the third quarter. Gross domestic product (GDP) declined by 0.3% from the previous quarter, worse than initial estimates for a 0.2% contraction. The services sector grew by 0.1% whereas the production sector shrank by 2.5%.

The revised data means the UK economy is now estimated to be 0.8% smaller than it was in the final quarter of 2019, just before the Covid-19 pandemic hit. In contrast, the other G7 economies grew, with US and eurozone GDP up by around 4% and 2% respectively in the third quarter versus Q4 2019, according to the OECD. The ONS data also showed households’ real disposable income – the amount available to spend after taking inflation into account – fell by 0.5% in the third quarter marking the fourth consecutive quarter of declines. Real household spending fell by 1.1%, the first drop since the spring of 2021. The ONS said the slowdown in spending on restaurants and hotels, and recreation and leisure reflected the cost-of-living squeeze on households’ disposable income.

US GDP growth revised higher

In contrast, US GDP growth in the third quarter was stronger than expected. According to data from the Commerce Department, GDP grew by 3.2% compared with the second quarter, better than initial estimates of 2.9% growth. The rebound reflected increases in exports, consumer spending, non-residential fixed investment and government spending, as well as a decrease in imports. The presence of a proper US recession is dismissed for now, as the data signals the end of a technical US recession, after GDP fell by 0.6% and 1.6% in the first two quarters of the year. (Many economists define a recession as two consecutive quarters of contracting GDP.) However, it is still expected that the US will fall into a recession in 2023. US indices fell following the release of the data, on concerns the Federal Reserve will continue to increase interest rates. These concerns were exacerbated by lower-than-expected weekly jobless claims, a further sign of the tight labour market.

US consumer confidence rebounds

The US GDP data came a day after figures showed a rebound in consumer confidence in December. The Conference Board’s consumer confidence index rose to 108.3, the highest reading since April and well above forecasts of 101.0 in a Reuters poll. The present situation and expectations indices also increased, reflecting consumers’ more favourable view of the economy and jobs. Inflation expectations retreated to their lowest level since September 2021, driven by recent declines in gas prices. Plans to purchase homes cooled further, which could continue to weigh on the US housing market through 2023. Separate figures from the National Association of Realtors (NAR) showed existing home sales tumbled by 7.7% in November from the previous month and by 35.4% year-on-year. Lawrence Yun, NAR chief economist, said this was driven by the rapid increase in mortgage rates, which hurt housing affordability and reduced incentives for homeowners to list their homes.

Please check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses

Alex Clare

29th December 2022