Please see below, a weekly market commentary received from Brooks Macdonald yesterday afternoon – 25/07/2022

- Europe was in focus last week with Nord Stream 1’s reopening, Italian elections and the European Central Bank’s (ECB) hike all competing for attention

- This week the US Federal Reserves’ (Fed) meeting and US Q2 Gross Domestic Product (GDP) will set the tone as we close out a volatile July

- US and European earnings ramp up this week with the majority of companies beating expectations so far

Europe was in focus last week with Nord Stream1’s reopening, Italian elections and the ECB’s hike all competing for attention

Economic growth expectations remained a key driver of market moves last week with weaker data continuing to paint a picture of a slowdown in the US and the rest of the world. As a result bond yields fell, helping growth focused equities outperform already strong gains within the European and US stock markets.

Last week was dominated by European headlines, be those around the resignation of Italy’s Prime Minister, the restarting of the Nord Stream 1 pipeline or the ECB which scrapped its forward guidance in favour of a 50bp hike1 . This week the US will be in focus with the Federal Reserve concluding its rate setting meeting on Wednesday where it is widely expected to hike rates by 75bps2. Investors will be looking at how Fed Chair Powell balances the inflation risks with economic growth risks particularly given the weaker initial jobless claims of recent weeks which suggests a deterioration in the employment outlook. With the market now pricing in a change in tone at the Fed at the start of next year, with subsequent interest rate cuts, how the Fed addresses this elephant in the room is arguably more important than the size of Wednesday’s hike.

This week the US Fed’s meeting and US Q2 GDP will set the tone as we close out a volatile July

With recession fears remaining central to market moves, investors will also be watching the US GDP number on Thursday, which if negative means the US has entered a technical recession after contracting in Q1 of this year. It is worth stressing the technical nature of this recession, should it occur, given Q1 US GDP was driven lower by global factors rather than US factors. Equity markets are likely to look through such an outcome however it may have second order impacts on consumer demand should it solidify consumer negativity about future economic growth.

US and European earnings ramp up this week with the majority of companies beating expectations so far

All of this alongside a bumper week for US and European earnings means that the week will be a fitting end to a volatile July. So far in the earnings season, around 20% of US companies have reported with the majority beating earnings expectations. Many companies have painted a more cautious picture of 2023 however this largely chimes with the market’s broader macroeconomic thinking and therefore has been accepted by investors without too much concern.

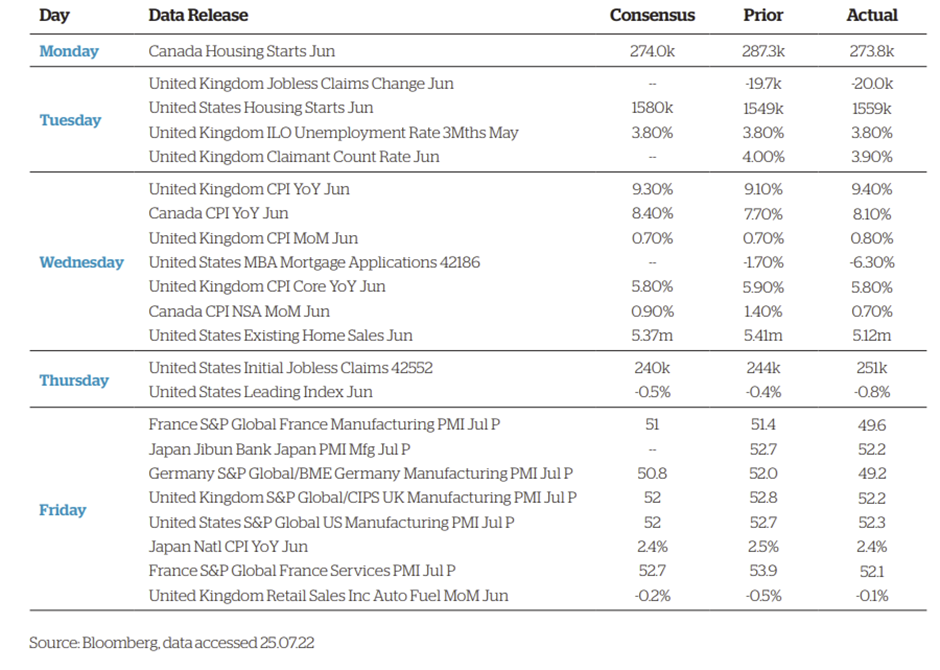

Economic indicators (week beginning 18 July)

Economic indicators (week beginning 25 July)

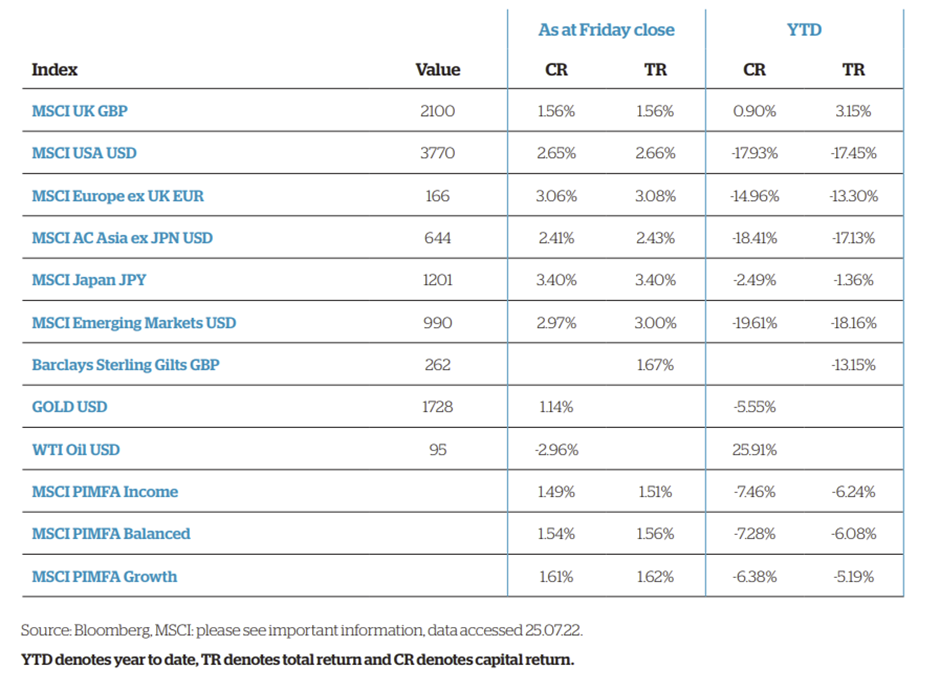

Asset Market Performance

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

David Purcell

26th July 2022