Please see article below from Jupiter Asset Management written by the European team at Jupiter – received 21/07/2020

Summary

- Welcome to the second instalment of our quarterly series of investment updates from your European Growth team at Jupiter.

- Alongside our usual monthly fund commentaries, we aim to build a library of insights into the way we think and the way we work. Think of this as the behind-the-scenes extra to the main feature.

- This quarter we give an update on the team, consider the global reach of our investments and offer an alternative perspective on the value of dividends.

Team update

We are very pleased to announce two new hires to support the European Growth strategy. We look forward to welcoming Nikisha and Phil and hope to introduce them to you in person when conditions permit.

The first, Nikisha Mistry, has joined us from Merian where she has worked on the European Smaller Companies strategy for the past three years. Nikisha will begin by focusing on ideas and holdings in our Smaller Companies funds but over time will, like all of us, broaden her coverage to the entire European investment universe.

Phil Macartney is an experienced equity investor we know well and are excited to have joining us. Phil is a UK and European analyst having worked on both long and long/short funds over 13 years. He joins us from Columbia Threadneedle where he was co-manager on the Threadneedle UK Mid-250 fund and also deputy manager on the Threadneedle UK Absolute Alpha fund. Phil joins the team in September.

Our culture of challenge and constructive debate will only be enhanced by these two excellent hires.

Around the world in 80 days

In lockdown for 80 days or so and unable to follow in Phileas Fogg’s footsteps, we have had time to consider the global nature of our strategy. Our search for companies with sustainable advantages naturally leads us to businesses that compete on the world stage.

As European equity investors, we regularly meet many who bemoan Europe’s prospects. They cite demographic headwinds and bureaucratic, inefficient governments. Some are hampered by large debts while others with strong fiscal positions are reluctant to spend.

We see things differently. Whether it is the digitalisation of the financial system in Brazil, the dynamism of healthcare in the United States or the emerging middle class of consumers in China, European-listed companies offer us access to many attractive growth opportunities. And, being European, they often come with better corporate governance, accountability and a focus on sustainability, too.

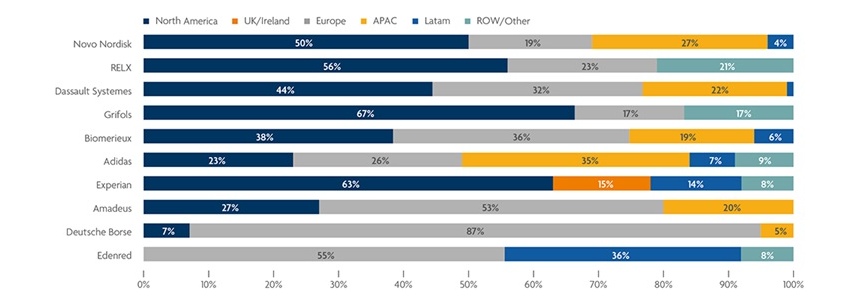

Revenue by Geography FY19

Chart: Company revenues by geography full year 2019 for some of our largest holdings. (Source: Jupiter, Bloomberg)

Global healthcare

Although the USA is known for innovative biotechnology, it is not alone. Europe was a pioneer in the process of plasma exchange – the harvesting of antibodies from blood donors to make therapeutic agents used to treat many autoimmune conditions. The pioneers, Dr Grifols and his two sons, built up the eponymous company in which we invest – it is still run by members of the family today and generates over two-thirds of its profits from the US market. Grifols continues to innovate. One potential area of promise is Alzheimer’s disease, where research has shown its products slow the progression of the disease in some patients with moderate Alzheimer’s.

Accessing Chinese consumers

A family feud between the Dassler brothers resulted in the creation of Puma and Adidas. Today, both would agree on the importance of China to the sporting goods industry. Last year, Adidas generated 35% of its revenues in the Asia-Pacific region with China being the largest contributor. A favoured brand among some 400m Chinese millennials, Adidas has stores in over 1,200 cities in China but hopes to expand to 2,400 to meet the growing demand. A strong digital footprint allows it to serve customers through its own website and those of partners such as Tmall.

Formalising the Brazilian economy

Edenred, a French company originally spun out of Accor, delivers digital payment solutions that appeal to clients far beyond its traditional homeland. Its products efficiently deliver benefits to corporate employees, give companies greater control over their expenses and help governments formalise their economies. In 2009, Latin America alone accounted for 40% of total operating profits. Here, over 90% of its business is digitalised compared to two-thirds in Europe. Digitalisation allows Edenred to offer many different benefits to its customers in a highly-attractive and cost-effective manner.

Global leadership in niche markets

Global leadership is not the preserve of large companies. Smaller companies often dominate their markets, especially in niche areas. For example, Dometic, with a market cap of just Eur2.3bn, is the leading manufacturer of appliances and components for recreational vehicles. It enjoys a market share of 45%, some four times greater than its nearest rival. Dometic’s headquarters may be in Sweden but over half of sales arise from the Americas, its largest market.

A preference for effective capital allocation – why we don’t focus on dividend yield

Companies are increasingly asking us what we think about their dividend policies. You can probably guess why.

It’s been an extraordinary year. For equity investors, huge uncertainty and immense share price volatility have made many traditional valuation metrics meaningless. Income investors have had a torrid time as supposedly stalwart dividend payers cancelled or clawed back payments to offset collapsing revenues, bolster over-stretched balance sheets or assuage societal scrutiny.

When Royal Dutch Shell surprised the market in late April, cutting its dividend for the first time since the Second World War, parts of the financial press went into overdrive.

“…investors who have diligently saved for retirement and rely on shares that pay regular dividends, now face a shortfall in their annual income” (This is Money – 31 March 2020)

This kind of sensational hyperbole misses the point. The real issue is that such dividend cuts are likely symptomatic of a material reduction in the intrinsic value of the company.

A common misunderstanding

Even though dividends are decided annually by the board, some investors use the dividend yield to determine the attractiveness of a company. However, we believe this is a poor guide to the intrinsic value of a business and can lead to poor corporate capital allocation.

Nevertheless, dividends are considered, by many, as a significant part of how a company creates value for its shareholders. Consequently, some management teams slavishly try to meet specific dividend expectations or consistently grow the annual dividend per share. But is this really the best use of investors’ hard-earned savings? Do they really care how their investments are liquidated. And, more importantly, should they care?

Given that investors can create their own dividends by liquidating a portion of their holdings, we argue that the rational investor should not care1. That’s because dividends are not free income, they come at the expense of capital. If you receive a 5 cent dividend on a Eur1 share, the share price will drop in value to 95 cents. It is, in effect, an enforced capital release, not a creation of value. In our view, it makes more sense for the investor or portfolio manager to decide what capital to release and from which underlying assets, not a company management ignorant of the requirements of its individual shareholders.

If the right opportunities exist – reinvest

It is our firm belief that company managements should focus on whatever will create the greatest risk-adjusted total return for their shareholders. Thus, we would much rather a management reinvested excess cash flow into projects and opportunities with an attractive internal rate of return than feel obliged to return it to shareholders. The opportunity cost of cash returns (dividends and share buy backs) can be substantial. Reinvesting excess capital at high rates of return within the business will enable shareholders to harvest a much greater income over time, than if a company simply returned all excess income annually.

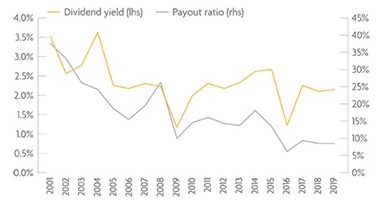

Campari, the drinks manufacturer, provides an example of how thoughtful capital allocation creates value for long term shareholders. Campari’s management is perhaps less constrained than many. With just one key majority shareholder, it is supported in its longer-term growth ambitions. And although Campari does pay a dividend, it is essentially an afterthought. What matters to management is the long-term creation of value. Here, Campari’s strategy is to acquire local or regional brands and then develop their appeal to a broader market. Its brands include Aperol, Grand Marnier and, of course, that great bitter, Campari. By using its excess capital to acquire niche spirits brands, Campari has moved from being a relatively small player to a key competitor in the global spirits market. Had management instead focused on maintaining a 40%-50% pay-out ratio then the investment story would have likely been quite different.

Campari – capital allocation decision to reduce dividend pay-out ratio (rhs %)

Campari – Relative share price performance and Market Capitalisation (Eur m)

Charts: Campari chose to reduce its dividend pay-out ratio and use its free cash flow to focus on long-term value-enhancing M&A. This has created huge capital appreciation for shareholders in absolute terms and also relative to the wider market. (Source: Jupiter, Bloomberg)

That is not to say that companies should not pay dividends. If there is no opportunity to enhance shareholder returns through further investments then excess cash should be returned.

Your Jupiter European Growth team:

Mark Nichols, Mark Heslop, Sohil Chotai, Nikisha Mistry

An interesting article from the European team at Jupiter Asset Management which gives us a good alternative perspective on the value of dividends and the global reach of their investments.

Please continue to check back for our latest blog posts and updates.

Charlotte Ennis

22/07/2020