Please see the below article from Invesco received over the weekend:

The economic success of China presents appealing investment opportunities in a broad range of sectors. Not only that, but efforts to loosen the reigns have enabled much easier access to its financial markets.

But how can investors gain exposure to China? Most international investors do so via a multi-country portfolio or index, however we believe this may not provide the best exposures, given China’s economic rise, strong risk- adjusted returns (see Table 1), and unique opportunities. Our view is that investors should consider a standalone China allocation.

In our view, China is an exceptional emerging market

Though it’s classified as an emerging market, we believe China warrants its own allocation. Its equity market is the second largest in the world – well ahead of the third largest, Japan, which is only around 40% of China’s size. Japan is already treated as a distinct asset class.

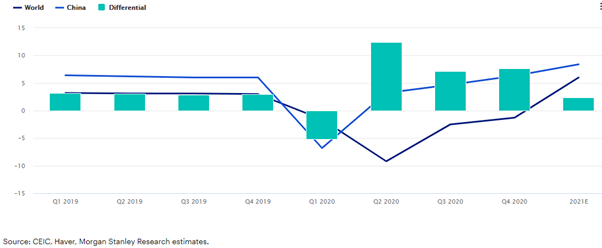

China’s GDP is now higher than that GDP of India, Russia, Africa, and Latin America combined, and we believe it’ll continue to deliver premium growth going forward. The COVID-19 crisis has served to strength China’s economic leadership (Figure 1). Thanks to effective containment, it has managed to emerge strongly from the pandemic. Real GDP expanded +2.3% year-on-year in 2020 – the only major economy globally that delivered positive growth. Economic activities were strong entering 2021, benefiting from continued recovery in both domestic and external demand. This contrasts with other emerging markets whose outlooks remain clouded by uncertainties surrounding the pandemic.

Figure 1. China is expected to deliver premium GDP growth over the world

In our view, the Chinese economy is poised for long-term structural growth. The strengths we see from a broad range of economic indicators will likely continue. China is also repositioning its growth drivers towards consumption and services, which are already the largest contributors to GDP growth. We expect its consumption market to hit US$17 trillion by 2030, supported by an expanding middle class and sustained income growth. Policy support is expected to be strong given consumption’s strategic importance to the government’s long-term growth plan. These can enable China to generate sustained expansion going forward and to remain the largest driver of global growth.

Historic appealing risk-adjusted returns

China’s strong economic prospects have been reflected in its equity market performance (Figure2). We compared the return and risk profile of Chinese equities and Emerging Markets ex-China equities on a five-year basis. Chinese equities delivered a much higher annualized return, and even after adjusting for risk, they offered a premium over Emerging Markets ex-China equities (Table 1).

Figure 2. Equity market performance of China relative to EM (April 2016=100)

Position into the future

China’s importance in the MSCI EM index has risen in recent years. Its index weight has increased to around 40% now from below 25% five years ago. We expect its index weight to keep rising given faster economic growth and further A share inclusion. Over the past 20 years, we’ve seen the return correlation between China and Emerging Markets structurally rising to around 0.9 from 0.6 (Chart 3). Once China’s weight exceeds a certain threshold, we believe emerging market equities could become almost indistinguishable from China alone.

Figure 3. Historic return correlation between China and EM

A dedicated China allocation could make it easier for investors to capture the entire opportunity set in China, discover new names as well as alpha sources.

Unique domestic opportunities

The growth of the Chinese economy means that there are now more than 5,500 competitive Chinese enterprises, across a broad range of sectors, listed across mainland China, Hong Kong, and the US. We believe they provide a large selection of alpha sources for investors to choose from when constructing their portfolios.

Compared to other emerging markets (except Taiwan and Korea) that remain dominated by traditional growth sectors, the communication services, consumer discretionary and healthcare sectors together account for above 60% of the MSCI China Index. They make up just 17% of the MSCI EM ex-China index (Chart 4).

In our view, this is another compelling argument for a dedicated China allocation. Given the structural changes the pandemic has made to the way we work and live, it provides investors with the chance to position for the future.

Figure 4. China may offer abundant investment opportunities in structural growth sectors that have been strengthened by COVID-19

What factors could challenge our views?

Pushback 1: COVID-19 will have long-lasting impact on employment and income growth in China

As consumption becomes more important to its economic growth, there’s a concern as to whether China can generate the employment and income growth needed to support ongoing strength in domestic consumption. Considering the uncertainty caused by COVID-19, this is valid.

In fact, the government’s surveyed unemployment rate rose to +6.2% in February last year and urban households only saw an increase of +0.5% in their disposal income in the first quarter. These data points are however improving as the economy recovers.

Unemployment rate fell to +5.1% in April this year. On the income side, growth also picked up to +12.2% in the first quarter of 2021.1 We expect further improvement in 2021 as economic activities are on track for normalization.

Long-term, the government continues to focus on the quality of growth rather than quantity. Employment is being prioritised in various policy decisions – with the goal of promoting and stabilising it.

Meanwhile, income inequality is on top of the policy makers’ agendas as well. China released its new Five-Year Plan this year and there is strong emphasis on social welfare and improving income equality in the document.

Challenge 2: Geopolitical tensions with the US will derail its long-term growth

Our team believes the geopolitical tensions with the US will be an ongoing topic. This is in line with many investors’ views. That said, we don’t expect this tension to derail China’s long-term economic progression.

Our view is that it’s worth investing in China, even with the ongoing tensions. It’s large and expanding domestic market is a valuable feature of its economy allowing it to enjoy unique economic and business cycles. These cycles rely on its domestic strength, helping to shield it from geopolitical complications. On a corporate

level, Chinese companies derive over 90% of their revenues from the domestic market and less than 5% from the US.2

Challenge 3: ESG standards are low in China

ESG development is gaining traction in China. An upward trend in disclosure rates of environmental, social and governance indicators is gradually catching up with global and regional standards.

During the United Nations General Assembly last year, China also pledged to reach carbon neutrality by 2060. We believe this ambitious commitment exemplifies China’s desire to pursue long-term sustainable growth and will propel the wave of ESG development going forward.

Regulators are a powerful force in China, which should drive further improvement in ESG disclosures among Chinese companies. The China Securities Regulatory Commission (CSRC) is expected to publish guidelines for mandatory corporate disclosure on ESG issues soon. We believe continued financial liberalization to attract more foreign investors will also drive ESG development in China. Increased focus on ESG by international investors should lead to rising awareness and improvements in ESG practices.

Conclusion

It’s for these reasons that we believe investors should consider a dedicated China allocation. Besides premium growth, the country may also offer the benefits of abundant, attractive investment opportunities. Its investment universe is deep and diverse and thanks to structural growth, may provide investors with ample compelling opportunities.

We believe investors can consider adopting an all-share approach when investing in Chinese equities. This means selecting opportunities irrespective of listing locations. Both onshore and offshore Chinese markets have unique listed companies and together, they represent the complete opportunity set for investors. We believe investors can look to experienced managers to make the best stock selection choices.

We have various views on China, please see Friday’s blog about Alibaba and Apple and regulatory scrutiny. From my point of view I think it’s a time for ‘Active’ fund management in China and the region.

Keep checking back for more of our regular blog content including market insights and views from some of the world’s top investment managers.

Andrew Lloyd DipPFS

20/09/2021