Please see below article received from Brooks Macdonald yesterday, which provides an update on the markets as world leaders reconvene for a fifth day at the United Nations Climate Change Conference in Glasgow.

What has happened

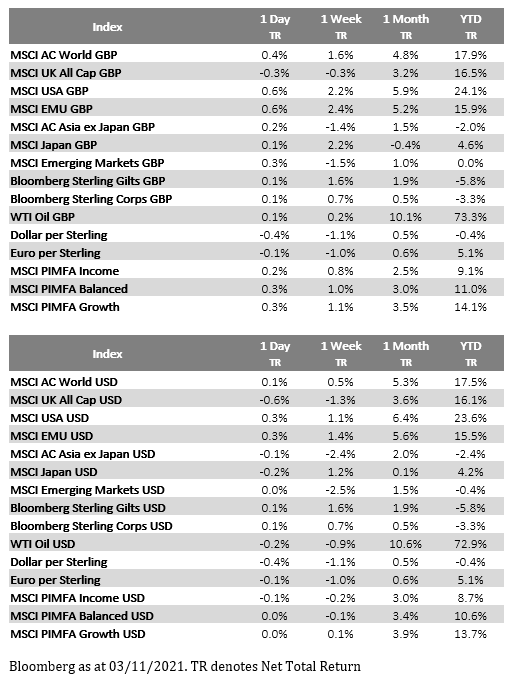

Global equities continued their series of fresh highs yesterday with mild gains across the US and Europe. Earnings continue to be a driver of these gains, even if they look slightly less bountiful than at the start of the season, with c. 90% of US companies reporting yesterday beating their earnings estimates.

Central Banks

After the RBA decision yesterday we saw a rally in sovereign bonds as bond markets priced in the possibility of central banks’ bark being worse than their bite. The major event today will be the Federal Reserve decision which is widely expected to contain a reduction in the monthly asset purchases by the US central bank. It’s worth noting that this is tapering the pandemic quantitative programme i.e. until the middle of next year there is still pandemic era net stimulus being provided by the Fed, just every month it’s slightly less. The distinction between a withdrawal of pandemic era stimulus narrative versus the beginning of a tightening cycle will be a tightrope all central banks will need to walk. Meanwhile President Biden yesterday said that we would make an announcement ‘fairly quickly’ on whether Fed Chair Powell would continue in his post for another term.

US Politics

Voters have gone to the polls in Virginia and New Jersey to elect their new governors. Several news outlets have called Virginia for the Republicans and rumours are abound that New Jersey will follow the same path. Virginia saw a 10 point margin of victory for Biden in the Presidential Election so a defeat here will be politically difficult for the President and bode badly for the mid-terms next year. Whilst a year is a long time, the probability of legislative gridlock in the US after the midterms seems to be increasing.

What does Brooks Macdonald think

A tapering announcement at the Fed’s meeting today is very much in line with the market’s expectation, however what will be of more interest is whether the Fed push back against the interest rate pricing for 2022. The difficulty for Fed Chair Powell is the highly uncertain path of near term inflation, should the inflation issues prove transitory a 2023 rate rise is probably still the base case, should pressures continue into the middle of next year a 2022 rate hike (or two?) is on the cards.

The Fed did as expected yesterday and reduced asset purchases. It will be interesting to see what the Bank of England do today on interest rates.

Please check in again with us soon for further relevant news and content.

Stay safe.

Chloe

04/11/2021