Please see below article received from Brewin Dolphin yesterday evening, which discusses new developments in the Middle East and fresh US inflation data.

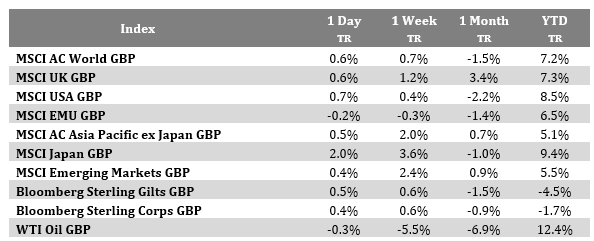

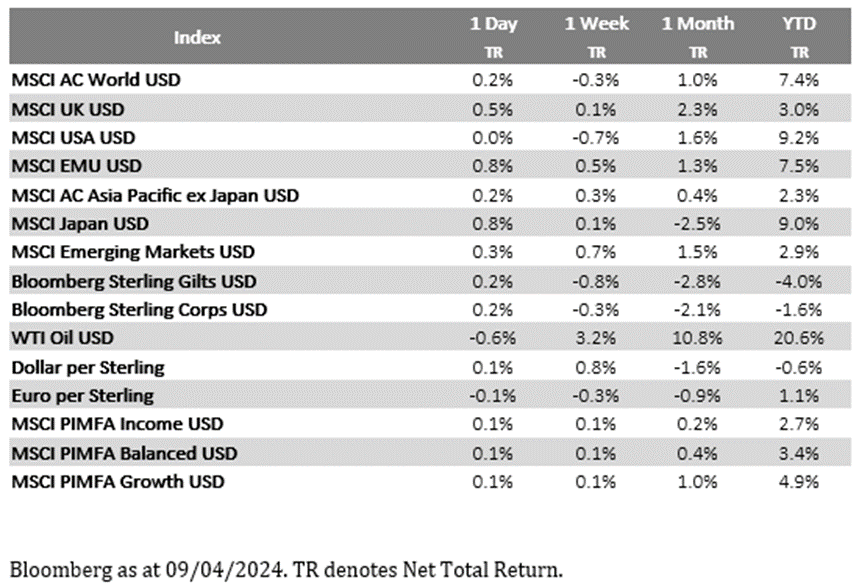

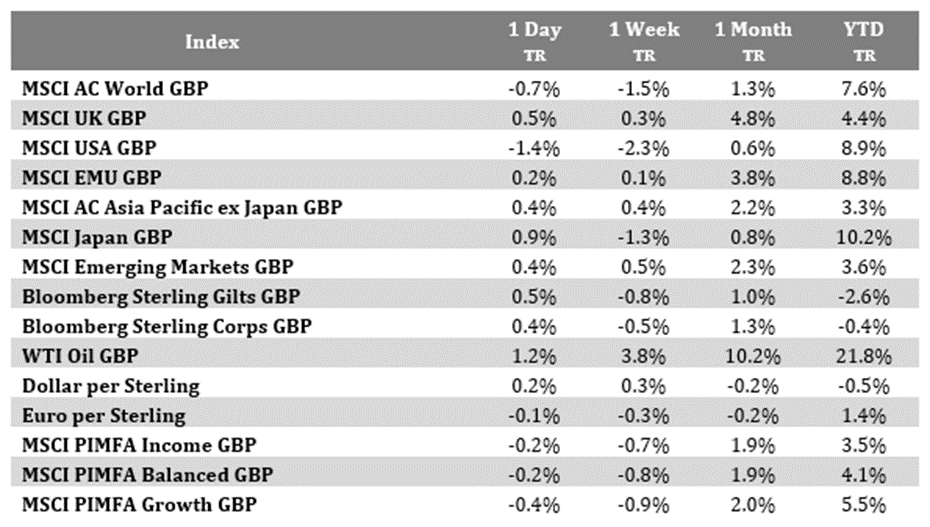

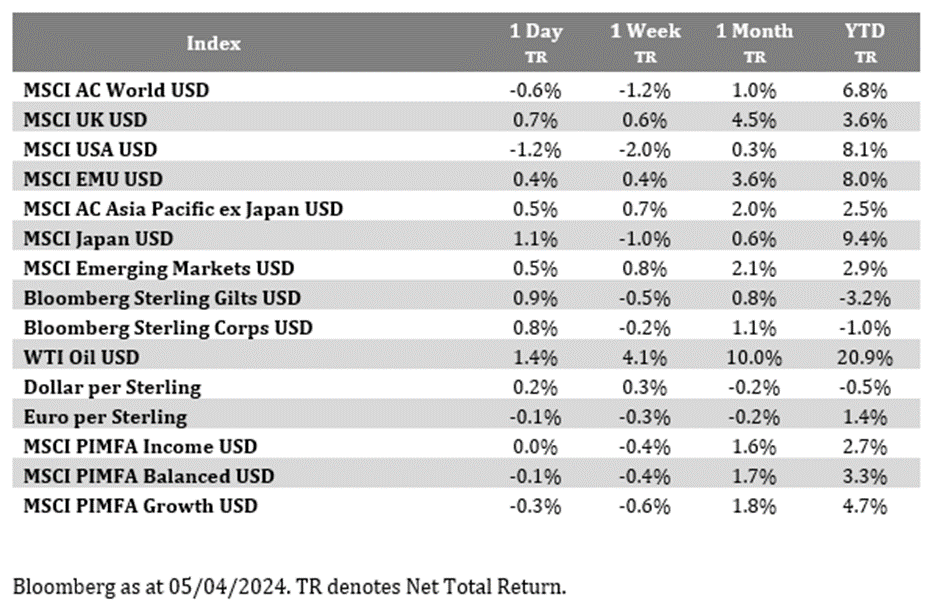

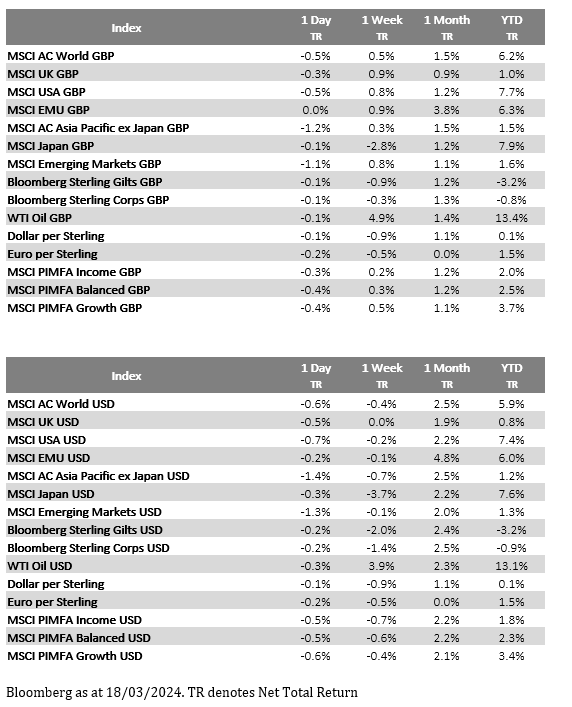

Overall, last week saw stocks pause for breath. They’ve recovered well after some modest declines in April and bonds have made modest gains too.

Markets have had to digest the news of the death of the president of Iran, Ebrahim Raisi, in a helicopter crash, which follows the ongoing tension with Israel, but markets are doing so with few signs of stress. Whilst tragic, the circumstances around the crash do not seem suspicious. Visibility was poor in a mountainous area. The president is not the commander-inchief; that honour goes to the supreme leader, Ali Khamenei.

The president’s role will now be filled by Vice President Mohammad Mokhber, with elections held within 50 days. As with President Raisi’s election, the candidate list will be heavily filtered. All eventual candidates will have ideological views that maintain the current stance of isolation from the West and favour China.

Meanwhile, from a macroeconomic perspective, last week’s U.S. inflation data was the main focus. As inflation continues to normalise the case for lower interest rates becomes stronger, that in turn supports equities and bonds. The complication with this narrative is that inflation hasn’t necessarily been normalising, it has in fact remained abnormally high.

In a previous weekly round-up, we discussed the assertion that the current level of interest rates is restrictive. While it is likely this is the case, they aren’t clearly or substantially restrictive as some members of the Federal Reserve seem to believe. If that were true, then it would mean inflation would be coming down slowly rather than overshooting, as it has tended to in the past.

A small step in the right direction for inflation

Has last week’s data reinforced or undermined that narrative?

There have certainly been suggestions that the inflation picture is improving. One such suggestion is the fact that the monthly increase in prices has slowed. This is the important core measure of inflation (stripping out volatile prices of items the central bank can’t do anything about), and this was the slowest pace of price increase in four months, and the first time in seven months that the core monthly price move has not been more than forecast. Sometimes, though, movements can be skewed by dramatic movements in individual components.

So, what did the detail of this report tell us?

Following on from some anxiety over growing tensions between Israel and Iran, the oil price had been strong. To see headline inflation slowing when there is a positive contribution from energy is quite unusual. The oil price has since eased off a bit, so unless it recovers it’ll likely be a drag on inflation next month.

The category weighing on prices is durable goods. Durable goods prices have declined every month for almost the last year, and for most of the last two years. This represents the hangover from a massive overspend on durable goods which took place during the lockdown when U.S. consumers had ample cash and time but had relatively few alternative consumption options. Second-hand cars have weighed heavily on this subcategory.

Services are still hot

Beyond goods though the picture is less encouraging.

Services prices are more directly affected by the labour market and fall more squarely in the category of things the central bank can influence. If services prices are rising, then raising interest rates should limit the amount consumers are able to spend.

Services consumption should decline, and services prices should slow or fall.

Alas, services prices are not slowing as much as had been hoped. The special category of core services excluding shelter, which policymakers and investors use to gauge this, rose 0.4% in April. That’s the slowest rate so far in 2024, but it’s more than double the target rate, so some improvement is needed to make policymakers believe inflation is on a sustainable path towards target.

We do assume this will happen though. One of the reasons consumers have been able to keep on spending on services is because of their accumulated savings, but according to estimates by the San Francisco Federal Reserve, these are now fully depleted.

The market cheered this release, which may seem odd given the ambiguous readings on services. But it came at precisely the same moment as a set of downbeat retail sales reports, so for investors hoping to see lower interest rates in the future, there was at least some evidence (although still mainly focused on goods rather than services).

And then there are other signs that interest rates may not be restrictive.

For one, we’ve seen a lot of corporate bond issuance in the early part of 2024. Issuers believing interest rates are going to fall might wait until their borrowing would be cheaper, but more importantly the ease with which the market absorbed this issuance suggests that financial conditions are quite loose.

Move over Lion King, ‘Roaring Kitty’ is back

We then have the bizarre return of the meme stock craze.

Meme stocks were a late 2020 and early 2021 phenomenon which saw a couple of relatively small companies experience incredible levels of price volatility driven by the actions of retail investors, aided by the widespread availability of leveraged investments.

YouTuber Keith Gill, known as Roaring Kitty, identified a situation in which hedge funds (one in particular) were speculating on declines in the shares of a particular company whose fundamentals were probably not as bad as they believed.

By investing on a leveraged basis and commenting on what he was doing, and thereby attracting fellow investors, he drove the price upwards.

This was not good news for anyone who had speculated on them declining. They were in a situation where they’d borrowed the shares to sell and were now needing to buy them in order to return them to the lender.

Eventually, for a variety of reasons, the speculation in both directions ebbed away and the prices of both stocks, Gamestop and AMC, declined.

But last week has seen the craziness resume. GameStop was at one time 200% higher, whereas AMC rose 300%, but both have since fallen sharply.

It might be surprising that meme stock mania has returned given the number of investors who were tempted into the speculation last time, only to suffer significant losses. But what is more surprising is what sparked the latest rise and fall.

It was prompted by Keith Gill posting an image on his social media of a video game player, leaning forwards. This single post added billions of pounds of implied value to the shares of this company, despite not really containing anything approximating an endorsement.

The original meme stock wave was partly ascribed to people having lots of time and money during lockdowns, but the economy has reopened and consumers are supposed to be tightening their belts. Perhaps this wave of apparent stock market speculation is consistent with an environment of restrictive interest rates?

China struggles on

Finally, it’s worth mentioning Friday’s economic data out of China.

Chinese shares have been terrible performers for the past six years, with only the occasional short-term rallies. Their most recent low was in mid-January and since then they have rallied 35%. But why is this?

It’s not because of the strong Chinese economy. In fact, it’s likely the opposite.

Friday’s data continues to show China struggling. Retail sales are slumping and a modest recovery in industrial production was driven by overseas demand. Consumers are suffering because the value of their principal wealth, their houses, has fallen by an average of 7% over the last year. The main concern is that because so many properties are empty, prices are likely to continue to significantly decline.

To date, property support measures have come via demand support mechanisms – directing more credit to developers to finance the completion of existing projects (good for economic activity but intensifying oversupply) and stimulating demand by cutting mortgage rates and relaxing purchase controls.

However, banks still don’t want to finance the new developments which would normally attract a lot of funds from pre-sales. Households understandably don’t want to purchase unfinished homes from developers, even at lower prices.

China’s Politburo has suggested it’ll address oversupply by taking properties out of the market. Media reports suggest that officials are considering “having local governments across the country buy millions of unsold homes,” and policymakers are considering creating a national real estate investment vehicle to acquire and revitalise unfinished properties across the country.

These proposals are promising, but a lot will depend on how forcefully they are implemented and how purchases will be financed. The size of the property overhang is enormous, and any purchased units would need to be maintained or see their value diminish.

Investors are betting that based upon these challenges, monetary policy will be loosened, and local savers will see the equity market as a better home for their wealth than the struggling property market.

Please check in again with us soon for further relevant content and market news.

Chloe

22/05/2024