Please see below article received from Brooks Macdonald this morning, which provides a global market update for your perusal.

What has happened

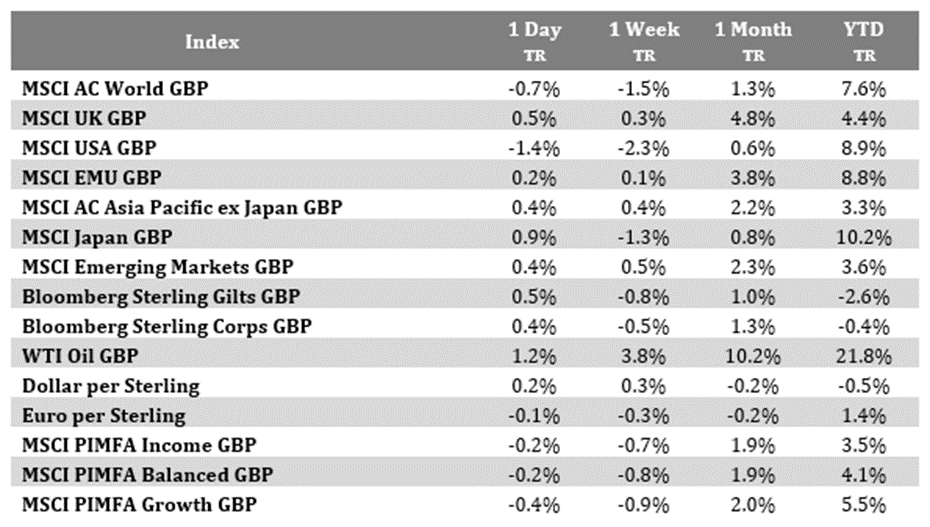

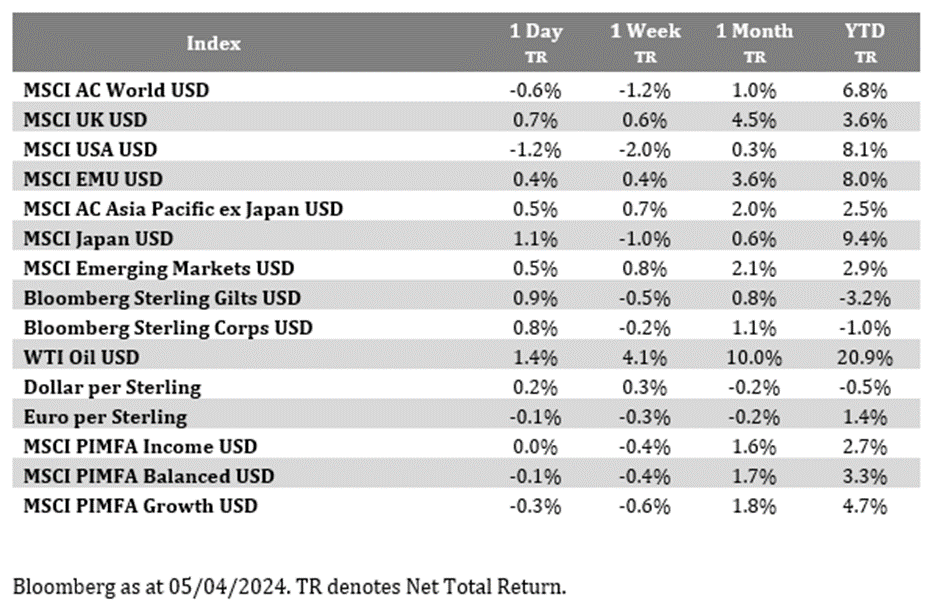

Equity markets were initially building for a small up-day yesterday, but after Europe closed, in later US hours trading things took a sharp turn down. The US S&P 500 equity index fell by over 2% intraday, ending the session down – 1.23%. The main catalyst for the fall was rising tensions in the Middle East, which has pushed oil prices higher, and in turn adding to worries around the risks for resurgent inflationary pressures. In better economic news, yesterday saw the Euro Area composite PMI (Purchasing Managers Index) which was up to 50.3 for March, versus February’s 49.2, and marking the first time it has been in expansionary territory in ten months. Later today, markets will be focused on the US labour market, with US non-farm payroll numbers for March due – payrolls are seen increasing by at least 200,000 for a fourth straight month. Average hourly earnings are projected to climb 4.1% from the same month last year, which would be the smallest annual advance since mid-2021.

Oil prices hit $91 a barrel

Brent crude oil prices have made new 5-month highs in early trading this morning, building on yesterday’s gains, and briefly trading above $91 per barrel. The latest rise follows mounting geopolitical tensions around the Middle East – Israel has increased preparations for potential retaliation by Tehran after Monday’s strike on an Iranian diplomatic compound in Syria. Meanwhile, US President Joe Biden told Israeli Prime Minister Benjamin Netanyahu this week that US support for the war in Gaza depends on new steps to protect civilians. Separately, Netanyahu said at his country’s security cabinet meeting that Israel will operate against Iran and its proxies and will hurt those who seek to harm it. Oil has rallied this year on the back of combination of tightening global supplies, better than expected demand, and geopolitical risks in both Russia-Ukraine and the Middle East. Finally, regarding Russia, a NATO official said yesterday that Ukrainian drone strikes on Russian refineries may have disrupted more than 15% of Russian capacity, potentially adding to supply constraints.

US dollar strength is not good news for some

This year has seen an arguably already strong dollar move stronger, boosted as markets have in recent months reduced their expectations for the scale of likely Fed rate cuts later this year. As a result, a resurgent US dollar is causing problems for central bankers and governments around the world, forcing them into action to relieve the pressure on their own currencies. By way of example, Japan’s Finance Minister Shun’ichi Suzuki last week warned of “bold measures” to bolster the yen, while Turkey unexpectedly hiked interest rates last month, and elsewhere, Swedish officials have recently said a weaker krona could delay its first move to ease interest rates.

What does Brooks Macdonald think

Exchange rates matter because a depreciating currency can risk increasing the cost of imported goods for the country in question, leading to a drive-up in inflation. Meanwhile, there’s also an increased risk that investment flows could also move away from a country with a weakening currency in search of higher expected returns elsewhere. This so-called ‘capital flight’, which can harm domestic investment and growth, can be a risk for some emerging market countries in particular given their often relative economic reliance on investment inflows to start with.

Please check in again with us soon for further relevant content and market news.

Chloe

05/04/2024