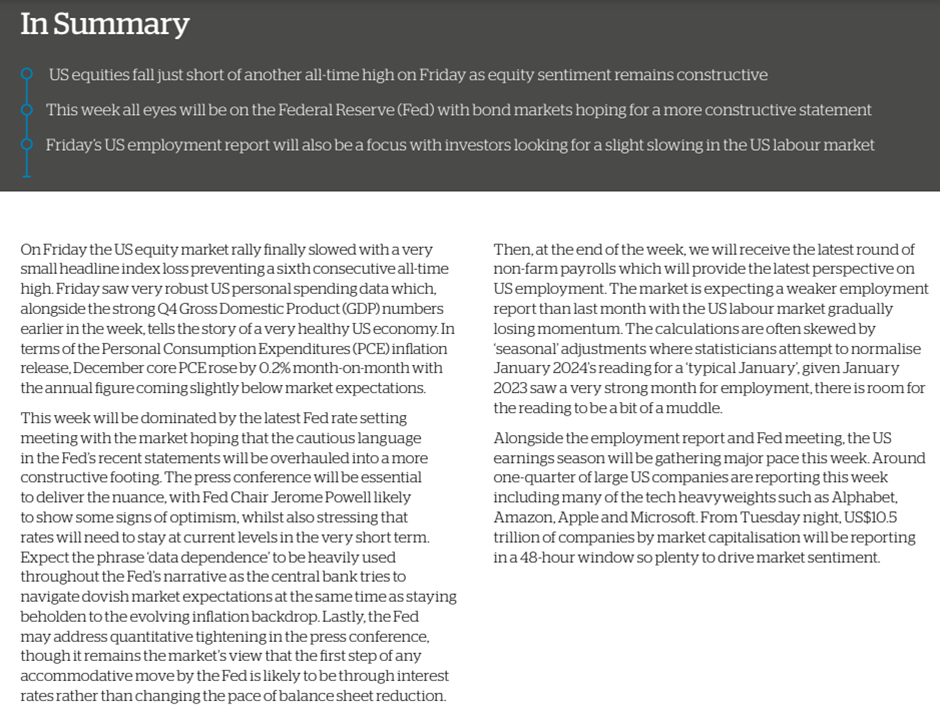

Please see below, an article from EPIC Investment Partners which focuses on the economic strength of Qatar and the potential investment opportunities. Received this morning – 31/01/2024

We have often mentioned to clients that we believe the rating agencies are behind the curve, so we were pleased to hear that Moody’s Investor Service recently upgraded its long-term rating for Qatar by one notch, from Aa3 to Aa2, its first upgrade since 2007. The already high rating for the wealthy nation now sits on par with the UAE, South Korea and France, and is now in-line with S&P Global’s AA rating. Fitch rates Qatar one notch lower, at AA-, with a positive outlook, signalling a potential upgrade.

Moody’s analysts attribute the upgrade to Qatar’s improved fiscal metrics, which have been “achieved during 2021-2023”, and are expected to be “sustained in the medium term”. The government’s commitment to fiscal prudence (the IMF estimates the nation’s debt to GDP is ~40%, from 73% in 2022), including the gradual reduction of infrastructure spending (linked to preparations for the 2022 FIFA World Cup), is seen as a contributing factor to the upgrade.

The rating agency further recognises Qatar’s major investments in liquefied natural gas (LNG) production capacity as credit positive. Qatar, the world’s third-largest LNG exporter, is investing substantially to boost its output by about 60% over the next three years, in a move to meet rising global demand growth, particularly given the significant role the fuel plays in the transition to cleaner, more sustainable power sources.

Given the rising frictions in the Red Sea and Qatar’s dependence on the export route, S&P Global recently commented that diverting LNG carriers away from the Red Sea would minimally affect Qatari oil and gas entities, since most of their customers are located in Asia. The agency went on to add that barring risks of regional war, the impact of tensions on rated Qatari energy firms like Nakilat, and QatarEnergy’s LNG project is manageable.

Away from hydrocarbons, Qatar has made impressive strides in diversifying its economy, driven by the Vision 2030. Thanks to sustained investments and policy support, Qatar’s non-oil sectors now comprise over 50% of real GDP. Thriving industries such as financial services, tourism, and manufacturing are fast emerging as new engines of economic growth. Qatar is also expanding output in high value sectors like chemicals and technology, which leverage its natural gas resources. With huge investments allocated to transport infrastructure and private sector stimulation, Qatar’s economic base is rapidly broadening. Prudent economic management has translated this diversification into solid GDP growth rates despite hydrocarbon price volatility.

We also remain cognisant of Qatar’s diplomatic mediation initiatives. Driven by a desire to establish itself as an independent and progressive player on the world stage, Qatar has embraced diplomatic mediation as a cornerstone of its foreign policy.

We have long favoured Qatar’s sovereign and quasi-sovereign bonds. Through our investment process, we have identified Qatar as having a 7-star NFA score, defined as a “wealthy nation”. Then, using our proprietary relative value model, we have identified undervalued bonds issued by the government and government-owned entities. A good example of a bond we favour is the Qatar 6.4% 2040s. This bond is currently trading ~45 bps wider than similarly rated bonds with a ~10-year duration and offers a risk-adjusted return and yield of ~10%.

Qatar has not issued international bonds in around four years, simply because it does not need to. So, its first green bond offering, which is coming “soon” according to the nation’s finance minister, Ali Al-Kuwari, will attract much attention, and will further demonstrate its commitment to sustainability funding.

We continue to believe Qatar’s economy will maintain its positive trajectory, supported by rising LNG exports and diversification efforts, and through its mediation efforts will continue to bring it to the fore as a global ally. Therefore, as long as the bonds offer attractive risk-adjusted returns, or alpha, Qatar will remain a high conviction investment in our Next Generation Bond Strategy.

Please continue to check our blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Alex Kitteringham

31st January 2024