Please see the below article from Brewin Dolphin detailing their analysis of the U.S. job data and the impact on financial markets. Received yesterday 08/10/2024.

While there was some reassuring news on the economy last week, there was some concerning news on the geopolitical front. It’s worth considering how these trends can become intertwined.

It’s been a year since Hamas launched its unprecedented attacks on Israel from Gaza. Since then, Israel has conducted an extensive ground operation in the region. Conflict has also continued between Israel and the Houthis in Yemen and Hezbollah in Lebanon.

In recent weeks, the conflict has intensified significantly around the Lebanese border, with some ground operations by Israeli forces in Lebanon. Last week, Iran launched 180 ballistic missiles against Israeli targets. The two sides differed in their reports of the operation’s success but thankfully, casualties were low.

Nevertheless, speculation has risen that Israel could attack Iran’s oil infrastructure in retaliation, as predicted by former Israeli Prime Minister Ehud Barak. This speculation was fanned by comments from U.S. President Joe Biden. When asked whether the U.S. would support such a move by Israel, Biden responded: “we’re discussing it”.

What’s at Risk?

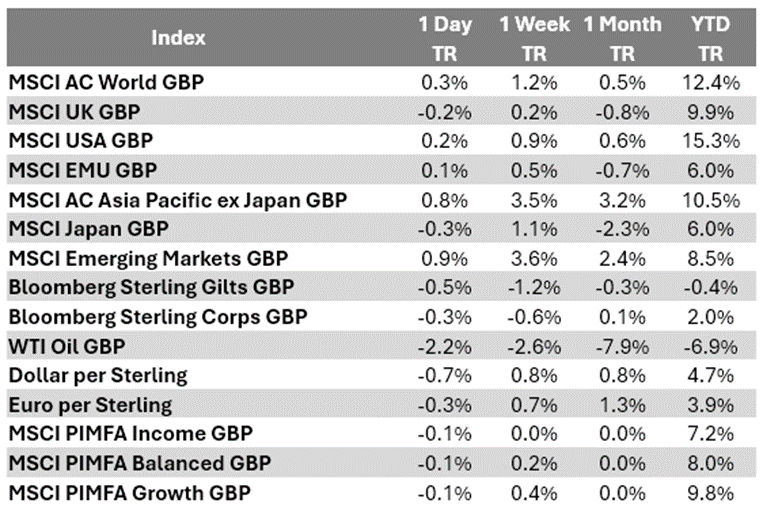

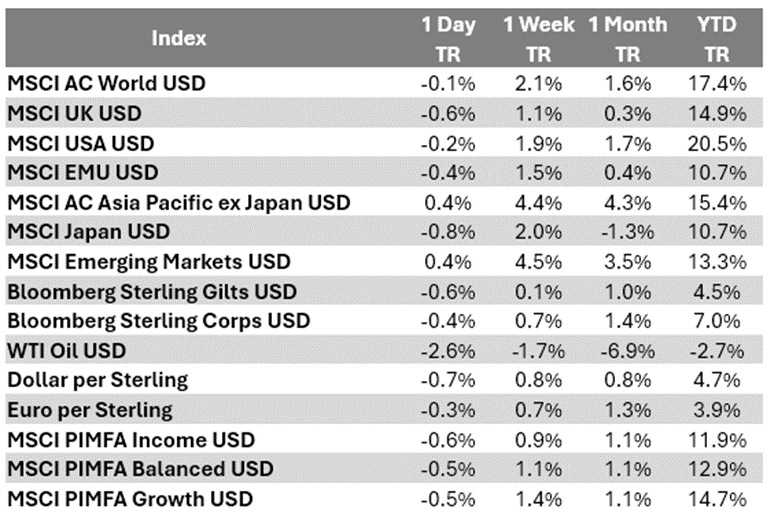

The events in the Middle East are very troubling from a human perspective, but we know that markets and to a large extent economies, are dispassionate about such things. If the conflict were to impact energy production, markets and economies would begin to react quickly. Indeed, following Biden’s comments on Thursday, oil rose around 4% and ended the week 9% higher.

In previous notes, we have discussed the benefits of an energy position within portfolios. The bull case here is that energy stocks stand to benefit from a reluctance to invest in new energy supply. Constraints on energy investment are more politically acceptable than taxes on energy consumption, which have the same effect of driving energy prices higher. The difference between the two is that taxes would create revenue for governments, whereas supply constraints increase profits for suppliers.

This capital cycle argument has in recent months been overwhelmed by a gloomy outlook for energy demand. In the U.S., the change in consumer behaviour over the summer months has raised fears that gasoline demand could be weak. Across the U.S. and Europe, evidence last week continued to suggest that the manufacturing sector is suffering from an ongoing recession. But the main factor weighing on energy demand has been China.

We discussed a couple of weeks ago how the China situation has changed significantly, with a forceful monetary and fiscal stimulus unveiled over a few days the week before last. While the Chinese mainland market was closed for most of last week due to the country’s Golden Week national day celebrations, Hong Kong shares rallied, meeting the threshold for a bull market (a 20% gain). Prior to this, Hong Kong-listed Chinese shares had seen a decline of 50% since early 2021.

Historic worries over oil prices

Anxiety over the energy supply has haunted investors since the 1970s. Why? Well, oil price increases can act as a tax on consumers and cause them to reduce other forms of spending.

Here’s a brief recap of the major incidents since the ‘70s:

- The 1973 oil embargo by the Organization of the Petroleum Exporting Countries (OPEC+) in protest of the Arab Israeli war caused prices to quadruple and triggered a global recession

- A second oil price shock at the end of the 70’s was triggered by production disruption caused by the Iranian revolution

- The Gulf War precipitated an oil price spike and led to the early 1990s recession

- Sharp energy price increases were also present when the tech bubble burst in early 2000 and at the outset of the global financial crisis in 2007

It can be a little unclear how a central bank would react to a price spike. If it happens when the labour market is healthy, there’s a higher chance of workers demanding their wages keep pace with inflation. If unemployment has been increasing, they may cut back on discretionary spending instead. This will determine the extent to which the central bank feels it needs to increase interest rates, given that a rise in oil prices can be destructive to demand on its own.

What’s happening now?

That brings us on to the current state of the U.S. economy.

We have talked a bit about management commentary, which has suggested things are stable, and that the summer slowdown was a seasonal lull rather than a terminal decline. Last week’s labour market data backs that up.

Early last week, the U.S. Bureau of Labor Statistic (BLS)’s Job Openings and Labor Turnover Survey showed fewer people are quitting their jobs. This suggests less need for high interest rates because the rate of job quitters is a good leading indicator of wage growth. Encouragingly, the number of job openings increased, suggesting that labour demand remains robust.

The non-farm payrolls employment report seemed to confirm this on Friday, as it showed an acceleration in jobs growth to the fastest rate since March.

This followed the purchasing managers indices, which suggested that U.S. services sector activity remained very robust – however manufacturing remains very weak.

Meanwhile, continental Europe is suffering a slowdown that seems to be leaking from manufacturing into services. Some U.S. services sector anecdotes seemed to suggest this was happening there too, while others expressed concerns over the forthcoming election in early November.

What’s Next?

It was a surprising week even for those of us who believe the economy will buck the historical trend and avoid recession. From an investment perspective, we’ve seen a lot of liquidity added to markets. This will continue with the large-scale Chinese stimulus announced the week before last. Further action is expected, particularly from the European Central Bank. Even Bank of England Governor Andrew Bailey talked about being more aggressive with rate cuts if the inflation data remains under control.

That should provide a decent environment for assets like equities, but we find diversifiers like gold have a role to play as well. Bonds saw some selling because of the good news on the economy, and gold was certainly caught up with that to an extent. But the risks that remain from high oil prices and fiscal largesse from the U.S. electoral candidates are factors that would encourage investors to flock to gold.

The current environment is one that seems well suited to real assets like gold and oil, not least because of the uncertainty that prevails at the moment. While the soft-landing scenario got a boost last week, we have long felt it was the most likely scenario in the absence of an economic shock. The most obvious source of such a shock would be the oil price, and Middle Eastern tensions serve as a reminder of how fragile a solid economy can quickly become.

This week will see further evidence of the inflation moderating in the U.S. before earnings season starts on Friday. A number of banks, including JP Morgan, will announce their results, but they will also be asked about the state of the American consumer, and with sight of household bank balances and spending patterns, what they say will go a long way to setting the tone for earnings season as a whole.

Please continue to check our blog content for advice, planning issues, and the latest investment, market and economic updates from leading investment houses.

Alex Clare

09/10/2024