Please see below article received from EPIC Investment Partners this afternoon, which provides market predictions for 2025.

As next week’s FOMC meeting approaches, we turn to our proprietary Fed funds model for insights into the likely path for US interest rates. Developed in the 1990s, the model analyses US capacity utilisation, unemployment, and inflation to predict the appropriate federal funds rate. While the neutral rate—or r-star—represents the interest rate that neither stimulates nor restricts growth, the model focuses on projecting short-term policy adjustments by analysing capacity utilisation and unemployment. At present, the federal funds rate remains above the neutral level, estimated at roughly 3%.

Capacity utilisation, a key indicator of economic slack, currently stands at 77.6%, below its historical average. This underutilisation signals room for economic growth without triggering inflation, providing scope for a more accommodative policy stance. With inflation expectations anchored at 2% and a real rate of 0.5–1%, the neutral rate is estimated at approximately 2.5–3%, serving as a benchmark for evaluating monetary policy. Historically, periods of below-average capacity utilisation have supported lower rates, as slack reduces inflationary pressures. While a pause in rate adjustments is likely in January, gradual cuts toward this neutral range seems likely as 2025 progresses.

The neutral rate is closely tied to capacity utilisation and unemployment, key inputs in our Fed funds model. While the model does not explicitly estimate the neutral rate, it aligns federal funds rate predictions with prevailing economic conditions, reflecting shifts in these metrics. Periods of high slack, for example, signal the need for lower rates, aligning policy with prevailing economic conditions.

Market expectations for 2025 broadly align with the model’s forecast for federal funds rate adjustments, which consider both economic slack and inflation trends. Despite the uncertainty surrounding fiscal policies under the current administration, the economy remains below the conditions needed for a neutral monetary policy stance. Monetary policy remains restrictive, with rates above neutral estimates. A pause during the January meeting would provide an opportunity for the Fed to evaluate incoming data and refine its outlook. Should inflation continue to moderate alongside subdued capacity utilisation, a gradual shift toward the neutral rate is expected as economic slack persists and inflation moderates. However, the transition will require careful calibration to prevent reigniting inflationary pressures or undermining growth.

Further Fed easing sets the stage for opportunities in fixed-income markets. Looking through the uncertainty of fiscal policies, higher-quality investment-grade emerging market bonds are particularly well-positioned to benefit from declining interest rates and stabilising global economic conditions. Mexican credit, in particular, looks attractively valued, offering compelling opportunities for investors looking for opportunities to diversify. These assets combine robust credit profiles with attractive yields, making them a compelling choice for investors looking for alpha opportunities. With risk sentiment likely to improve alongside monetary easing, 2025 offers a favourable environment for higher quality emerging market debt.

Please check in again with us soon for further relevant content and market news.

Please see below, an article from EPIC Investment Partners providing a brief analysis of the current economic conditions within Europe. Received today – 23/01/2025

At the World Economic Forum in Davos, Christine Lagarde delivered a sobering assessment of Europe’s economic landscape, warning of an “existential crisis” that demands immediate attention. The ECB president highlighted the continent’s vulnerability to the US’s shifting global economic strategy, particularly in light of Trump’s “America First” policies.

The economic outlook paints a challenging picture. The IMF forecasts a meagre 1% expansion for the eurozone, starkly contrasting with the US’s projected 2.7% growth. Germany, Europe’s largest economy, has experienced two years of contraction and is expected to grow by only 0.3% this year.

Deep pessimism about Europe’s economic prospects has been discussed by several key economic figures. Concerns mounted around several critical issues: leadership challenges in Germany and France, the rise of far-right movements, technological regulation uncertainties, and the overall strength of the European Union.

Ursula von der Leyen, European Commission president, acknowledged the stakes, emphasising the importance of preserving transatlantic trade relations. With bilateral trade volumes at €1.5tn, both sides have significant interests at risk.

The challenges extend beyond economic metrics. Technology and AI regulation emerged as crucial battlegrounds, with one executive warning that a conservative approach could further marginalise Europe. The continent faces pressure to adapt quickly to evolving global economic and technological landscapes.

Despite the gloomy forecast, some voices of optimism emerged. Spain’s economy minister, Carlos Cuerpo, highlighted his country’s strong performance, with estimated growth of 3.1% last year, outpacing the US, coupled with a booming labour market.

On a further positive, solar power marked a pivotal moment in the European Union’s energy transition last year, generating 11% of electricity and surpassing coal’s 10%. Solar generation increased by approximately 22% to around 304 terawatt hours, while coal power fell nearly 16% to about 269 terawatt hours, reflecting a broader shift away from fossil fuels. With wind and solar now comprising 29% of EU electricity generation and countries like Germany and Poland reducing coal usage, Europe is making significant strides towards a more sustainable energy future.

Please continue to check our blog content for the latest advice and planning issues from leading investment managers.

Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 21/01/2025

There was something quite abstract about having a big week of economic data in the final run-up to the inauguration of a U.S. president who’s promised to shake things up.

Analytically, we can go through the motions, identify the outliers and the seasonal discrepancies, and take a view on the likely trajectory of the economy going forward. But we also need to appreciate that some things are likely to change with the new administration.

Returning to the here and now, inflation was the major focus last week, with the U.S. reporting producer and consumer prices data. The UK also reported its inflation data on the same day. This would normally be of only local interest, but with UK bonds having underperformed, and a measure of political pressure building on the UK government over its handling of the economy, gilts have threatened a return to infamy.

And what did the data tell us?

UK inflation was below expectations, which was very well received by the market, and likely very welcome in the halls of government. The decline in the headline inflation rate was marginal, but it’s core inflation, which strips out the volatile food and energy prices, that’s been the thorn in the UK economy’s side. It slowed from 3.5% to 3.2% per annum.

This was excellent news, and enough to see UK government bonds rallying. However, there was a fairly hefty caveat. Although food and energy prices are stripped out, other volatile prices aren’t.

A good example of these would be airline fares, which fluctuate wildly – not just from month to month, but even from day to day. They typically rise as the Christmas holidays begin but drop sharply on Christmas Eve and New Years Eve when few people want to travel. These dates were used to measure return flights for European and long-haul flights and would therefore have depressed the overall figures. It means that air fare inflation seemed to rise less than previous years.

Despite this, measures we like to follow continue to point to further disinflation. The rise in the median consumer price index (CPI) category was lower than last month, and services inflation had already slowed in recent months. Overall, core inflation may have been a little flattered by the measurement of air fares, at 3.2% per annum. It remains too far above target, but has been coming down, and should continue to do so.

The UK differs from the U.S. in an important regard. Persistent U.S. inflation could be ascribed to the strength of the country’s economy. Strong retail sales growth indicates that growth is likely to be at an annual rate of around 3% in the final quarter. In the UK, Thursday’s quarterly gross domestic product (GDP) data and Friday’s retail sales data were both very weak.

The strength of the U.S. economy, and the ensuing rise in U.S. and global bond yields, meant there was a lot of anticipation for higher U.S. inflation data. Indeed, prices rose faster in the U.S. over December, reflecting the rise in oil prices. But the core measure of inflation slowed without any of the irritating statistical gremlins that plagued UK inflation figures. The market reaction has been surprisingly strong to a modest undershoot of one measure of inflation. This is an indication of how nervous investors had been about the prospect of a re-acceleration in prices.

There’s been room for optimism as far as inflation data is concerned but that, as economists like to say, is ceteris paribus (all other things being equal). But we know that all other things won’t be equal.

How will a second Trump presidency differ from the first?

On Monday, Donald Trump was sworn in as the 47th President of the United States, and it’s looking like he’ll hit the ground running with early policy measures.

During his first term, Trump was politically intuitive but inexperienced and unconnected. He struggled to build a team to implement his policies and ended up relying on the Republican Party establishment to suggest colleagues and advisers. These included members of the administration such as Steven Mnuchin (Secretary of the Treasury), Gary Cohn (Chief Economic Adviser) and Rob Porter (White House Staff Secretary), who didn’t share the president’s agenda and worked against it. Consequently, it was a year before any tariffs were actually announced.

This time around, the Trump administration has prepared better, and Trump himself has built a team around him who are ideologically aligned (mostly). There are differences, but those are more likely to be evident later in the presidency.

Some members of President Trump’s administration, such as Scott Bessent, who’s been nominated as Treasury Secretary, see tariffs as more of a bargaining chip. Imposing tariffs now enables the administration to seek concessions in other policy areas. The most obvious example is encouraging other NATO members to invest in defence (U.S.-made defence) on pain of tariffs.

Other members of the administration, such as Peter Navarro, one of the few survivors of Trump’s original administration, consider tariffs against China at least to be a means of permanently moving away from economic integration with a strategic rival.

The above is an example of the nuance that can exist within a particular policy area amongst an aligned group of individuals. But there are multiple policy areas that have the potential to impact the economy. Tariffs are relatively easy to understand, even if we don’t yet know how broad they’ll be. Tariffs are also inflationary. They raise prices, albeit only on imported goods. Because goods form a small and declining share of the CPI basket, the impact will be limited, at least initially.

How will Trump’s policies impact the U.S. labour market?

The greater question is about the impact of immigration controls on the U.S. labour market. After data released in early January showed strong growth in employment, and with surveys suggesting that companies expect to hire more staff due to greater economic optimism, the availability of staff may become a big issue (as it was during 2022).

Exactly how many undocumented migrants President Trump will be willing and able to deport remains to be seen. It may only need a reduction in migration to start reducing the supply of workers and trigger renewed inflation. This is particularly true in the agriculture sector, which utilises a lot of migrant workers.

This will be amongst the key policy areas to watch out for announcements now that Trump has been inaugurated.

Finally, it’s worth mentioning the beginning of earnings season on Wednesday, which saw a buoyant start. As always, it was the banks that marked the unofficial start. Generally, their results were strong. Net interest margins have risen as savers feel less inclined to shuffle their savings around seeking the optimum rate available. Meanwhile, the big investment banks made large profits from trading bonds around the U.S. election, an early benefit of the new president.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Please see the below article from Brooks Macdonald detailing their thoughts on a recently sworn in Trump administration. Received this morning 21/01/2025.

What has happened

With US financial markets closed yesterday, investors instead watched Donald Trump being sworn in as the 47th US president. President Trump subsequently wasted no time in signing a raft of executive orders tightening immigration, ending green energy incentives in favour of oil and gas, and (albeit late in the day yesterday) planning tariffs on Canada and Mexico. Equity futures markets, which had earlier rallied on the lack of tariff news, subsequently retraced some of those gains, while the US dollar which had weakened earlier in the day, saw a jump up against most major currencies.

Trump ends green energy incentives

US President Trump yesterday ordered an “immediate pause” in spending on clean energy and other climate initiatives, deriding former US president Biden’s signature climate law (the ‘Inflation Reduction Act’) as the “green new scam”. Trump also ordered the US Environmental Protection Agency to consider eliminating the ‘social cost of carbon’, a metric used to help justify environmental policies. Earlier in his inaugural address, Trump defended a renewed energy focus on oil and gas production, saying that “we have something that no other manufacturing nation will ever have: the largest amount of oil and gas of any country on earth. And we are going to use it”.

US Trump trade tariff plans

Overnight, President Trump has said he plans to impose previously threatened trade tariffs on Canadian and Mexican imports into the US, saying that “we’re thinking in terms of 25% on Mexico and Canada … I think we’ll do it February 1st”. Trump also threatened to apply higher tariffs on Chinese imports as well as tariffs on European Union imports. However, while Trump indicated he was still considering a universal tariff on all foreign imports to the US, he added that he was “not ready for that yet”.

What does Brooks Macdonald think

In the past 24 hours, financial markets have had an early reminder of what life will be like under a US Trump administration. In particular, overnight we have seen volatility in markets as an initial relief around the absence of immediate sweeping tariffs has given way to nerves following Trump’s announcements of his Canada and Mexico trade levy plans late in the day. One early takeaway from all this is that Trump is likely to be highly ‘transactional’ in his approach to tariffs as well as other policy areas too potentially – that could make it very hard indeed for investors to anticipate and plan for overall policy narratives and expected economic and market impacts.

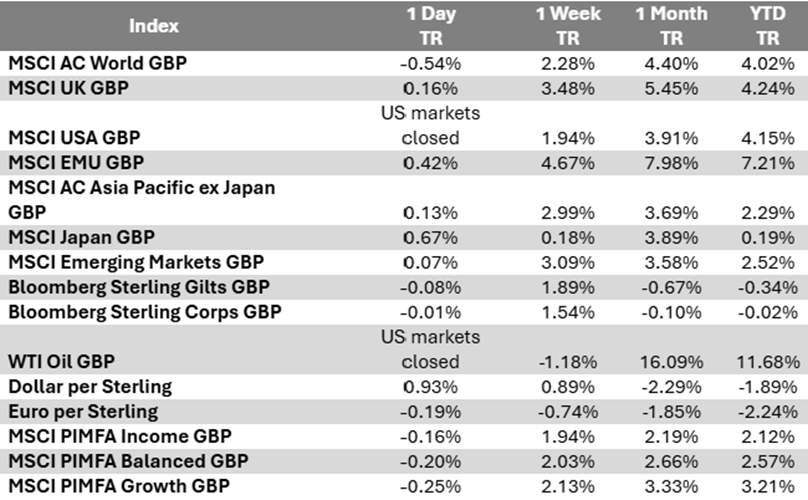

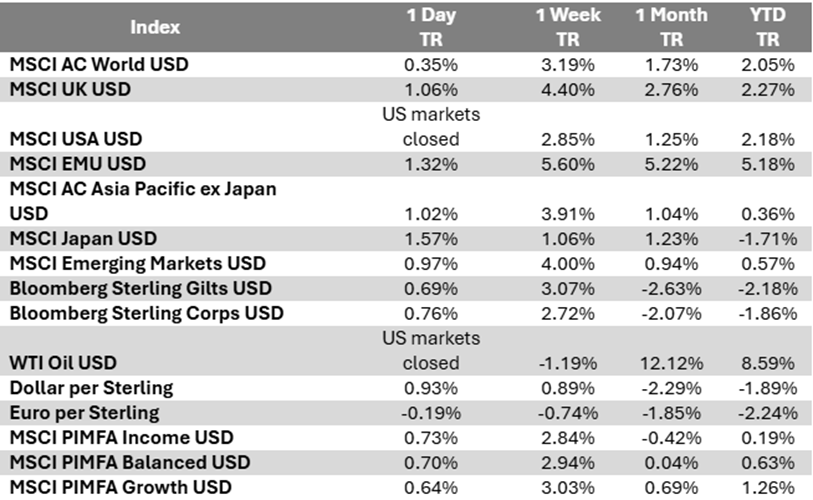

Bloomberg as at 21/01/2025. TR denotes Net Total Return.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see below, this week’s Monday Digest from Tatton Investment Management, analysing the key factors currently affecting global investment markets:

Calmer markets ahead of Trump inauguration

Global stocks bounced back 2% last week and bond markets calmed. UK investors did not even have to rely on a weak pound to boost sterling-based returns. UK government bonds recovered from the previous sell-off, as we cover below. Lower-than-expected inflation data for December makes an interest rate cut at the Bank of England’s (BoE) next meeting likely, and there was a refreshingly dovish speech from one BoE committee member. Annual inflation will almost certainly go up (due to higher energy prices) but we have argued the BoE should ‘look through’ near-term inflation and at least one BoE official seems to agree.

Markets were also worried about sticky US inflation, but those fears receded. December’s inflation report was in line with expectations, but investors reacted as though it was lower. The most encouraging signs are slower wage growth (despite job gains) and a smaller contribution from the shelter component. High interest rates are still compressing activity, which gives the Federal Reserve scope to cut. Global markets would welcome that, considering recently tighter financial conditions – thanks in large part to the strength of the dollar.

Tight liquidity conditions might mean downgrades to global growth forecasts this year – which will hurt smaller companies in particular. Notably, last week’s equity bounce-back became much more focussed on the mega-caps as the week went on, having initially started in small-cap. Oil prices also increased, but that looks like a pure supply-side story, following US sanctions on Russian shipping. Geopolitics are uncertain ahead of Donald Trump’s inauguration – but hints are the Ukraine will be a top priority, and that Trump could be more supportive of Ukraine than most assume.

Trump’s second term brings uncertainties but potential rewards. It helps that we start it with calmer markets than a week ago. Long may that continue.

Gilt and anxiety

Thankfully, UK government bonds (gilts) calmed down this week. The previous spike in gilt yields was led by higher yields elsewhere, but exacerbated by concerns over Britain’s economy and government fiscal policy – which many feared would lead to persistent ‘stagflation’ (no growth but high inflation). This then hit the same structural gilt market weakness revealed after the Liz Truss ‘mini budget’ in 2022: pension funds’ overexposure to volatile inflation-linked gilts. You might have expected pension funds to end their overexposure after that crisis, but the Bank of England settled the gilt market and meant funds reduced rather than closed their positions. Recent gilt volatility reignited the problem.

We said last week that this panicked selling made long-term gilts very cheap. Theoretically, long-term real (inflation-adjusted) bond yields should represent the market’s expectations for long-term economic growth. One of our preferred measures for this (constructing a theoretical future bond out of 15-year and 30-year yields) spiked above 2.5% last week, which suggests strong growth despite all the commentary focussing on the UK’s weaker long-term growth prospects. This suggests that gilt panic was more about short-term sentiment than long-term expectations and long gilts are a good buying opportunity.

Sure enough, gilt traders took the buying opportunity this week, pushing yields down from their highs and putting them once again in line with US yields. This was helped by the government reiterating its commitment to fiscal discipline and, particularly, unexpectedly low inflation data from December. This settled the nerves and allowed investors to appreciate how cheap long-dated gilts are. The narrative that gripped gilt markets last week always looked too dire to be true; this week’s news made it even less convincing. We shouldn’t expect plain sailing – given the UK’s uncertain outlook – but historically high yields make long-term gilts look good value.

More to come from India

India has had huge success in the last few years, but positivity has faded in recent months. Its stocks are up 30% since the start of 2023 and GDP grew 8.2% in the 2023-24 fiscal year. Foreign investors have sold out of India since the autumn, though, and growth has slowed. Interestingly, capital outflows have coincided with investor optimism about China, following Beijing’s stimulus announcements. Realignment away from China was previously helping India in trade and investment terms, and it looks like the sentiment about the two markets mirror each other.

Economists expect the Reserve Bank of India (RBI) to cut interest rates next month, but inflation is still high and the rupee has fallen sharply against the dollar. Currency weakness will likely be inflationary, given India imports 90% of its oil. But, the RBI isn’t independent (the government installed a more dovish governor just last month) and seems comfortable letting the rupee slowly decline. India has consistently higher inflation than elsewhere, which means its currency is losing its real value quicker than other nations – a recipe for further declines.

The RBI’s dovishness makes sense when you consider purchasing power, though. The rupee’s recent slide hasn’t been by as much as the difference between Indian and global inflation. That effectively means the rupee’s purchasing power has increased; Indians are able to buy more, despite the weaker currency. That’s what you expect in a strong economy, but policymakers won’t want India’s purchasing power to increase too quickly, as that would undermine the cheapness that has boosted Indian trade and investment. A managed decline in the rupee is therefore reasonable.

The long-term case for India is strong, despite the recent decline in foreign investor sentiment. It’s based on long-term trends of domestic economic reform and global trade realignment – which both have room left to run.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Please see below article received from EPIC Investment Partners this morning, which provides a global market update.

Despite US Treasury yields suggesting higher growth and inflation in the years ahead, demographic trends tell a different story. By 2033, annual deaths in the United States will surpass births, leaving net migration as the sole driver of population growth, according to the Congressional Budget Office (CBO). Without sufficient immigration, the population would shrink, undermining economic growth, worsening fiscal pressures, and intensifying the challenges of supporting an ageing society.

Recent OECD data starkly illustrates the issue: the working-age population’s growth rate has fallen to just 0.15%, sharply down from its peak of 2.24% in July 2000. Declining birth rates and an ageing population are primary drivers, but restrictive immigration policies have further compounded the slowdown.

From 2017 to 2021, annual net migration averaged only 750,000, a significant reduction driven by stricter border enforcement, reduced refugee admissions, and tightened visa restrictions. The CBO projects net migration to average 1.4 million annually in the coming decades, but this estimate appears overly optimistic given persistent political resistance and growing global competition for skilled migrants.

The stakes are immense. Without sufficient immigration, the US faces a shrinking workforce and fewer taxpayers to support an expanding number of retirees. Social security and healthcare systems, already strained, will face widening funding gaps, increasing the fiscal burden on younger generations. Slower economic growth would further constrain the government’s ability to meet its obligations, driving the debt-to-GDP ratio even higher.

Demographic shifts also reshape inflation and interest rate dynamics. A shrinking population reduces demand, creating deflationary pressures akin to those seen in Japan, where decades of demographic stagnation have coincided with weak growth and persistently low inflation. In the US, these deflationary trends could partially offset upward pressures on interest rates caused by sustained fiscal deficits.

Immigration is the clearest solution. Migrants not only fill labour shortages but also sustain demand and drive innovation. Between 2000 and 2018, immigrants accounted for nearly half of the growth in the working-age population. However, countries like Canada and Australia are actively competing for talent, adopting aggressive immigration policies that threaten to outpace the US. To remain competitive, the US must streamline visa processes, expand pathways for high-skilled workers, and implement integration programmes.

The bond market’s pricing, reflecting expectations of sustained growth and inflation, conflicts with long-term demographic realities. Projections for net migration must be realised to avoid population decline. If migration fails to meet these expectations, the US risks slower growth, intensifying fiscal pressures, and reduced global competitiveness.

Given these demographic and fiscal constraints, long-term bond yields appear too high. A return to zero-bound interest rates is plausible as debt servicing and demographic stagnation exert downward pressure. Persistent budget deficits make the current debt trajectory unsustainable, underscoring the urgent need for deficit reduction and immigration reform. Without these changes, a disruptive market correction may ultimately enforce this reality.

Please check in again with us soon for further relevant content and market news.

Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 14/01/2025

We may never know whether former Prime Minister Liz Truss was thinking “this is my moment” while her chancellor delivered the government’s growth plan (known colloquially as the mini-budget) to the House of Commons. It has, however, been known ever since as the ‘Liz Truss moment’ and has become shorthand for markets dumping a country’s assets in protest of an unsustainable tax and spending plan.

‘Liz Truss moment’ ranks alongside ‘Lehman Brothers moment’ as a descriptor of a severe market reaction. But perhaps it bears more in common with the more dramatically named ‘Black Wednesday,’ which the UK suffered in 1992 when it was forced to devalue the pound and leave the European Exchange Rate Mechanism (ERM).

In that instance, the Bank of England (BoE) was charged with maintaining the pound’s level within a 6% band against other members of the ERM. The band was too high for the UK, and as the pound started to slide out of it, the BoE was charged with buying sterling to bolster it. The central bank couldn’t, however, hold back a tidal wave of speculative flows betting that the pound would eventually be allowed to fall. Inevitably, it eventually did.

In doing so, many argue, the markets caused a devaluation that enabled the UK economy to emerge from recession, which the government’s misguided exchange rate policy may have prevented.

The all-powerful market

The similarity between that event and Liz Truss and Kwasi Kwarteng’s mini-budget was that the market showed itself to be more powerful and influential than the government. This is something that motivated Bill Clinton’s political adviser James Carville’s famous quote: “I used to think that if there was reincarnation, I wanted to come back as the president or the pope or as a .400 baseball hitter. But now I would like to come back as the bond market. You can intimidate everybody.”

The bond market, in these instances, is sometimes referred to as a group of bond vigilantes; individuals who enforce the law despite having no authority to do so. They differ, of course, from true vigilantes, who would be motivated by civic duty. This is because bond vigilantes are motivated by self-interest alone, with occasional policy improvements being a happy consequence rather than an objective.

Is this a ‘Liz Truss moment’?

That was then, this is now. After the mini-budget, UK ten-year borrowing costs reached 4.5%; they are 4.8% now. So, is Chancellor Rachel Reeves now having her ‘Liz Truss moment’?

The most obvious similarities are the adjacency to a budget, and the unusual phenomenon of a falling currency more-or-less coinciding with rising bond yields (which would normally attract foreign bond buyers).

The last UK budget was the end of October. In it, the chancellor, who had criticised Truss for having crashed the economy with a debt-fuelled tax-cutting programme, announced a debt and tax-fuelled spending programme. It was poorly received by the market, although the dominant emotion was probably disappointment rather than shock.

Here was a former BoE economist, who had been the shadow chancellor of the exchequer for three years. Reeves came with the endorsement of former Bank of England Governor Mark Carney and had committed to not raise taxes on working people. So, a budget that delivered a big increase in borrowing, and a big increase in employment taxes was very underwhelming.

However, it was less shocking because Reeves had at least allowed scrutiny by the Office for Budget Responsibility (OBR), and there was some recognition that she was facing an almost impossible task (improving public services whilst maintaining any semblance of fiscal credibility).

Therefore, there wasn’t the same dramatic reaction as to the Truss budget, but borrowing costs have risen and now eclipse those seen during the crisis. A lot of that reflects rising yields globally, particularly since the U.S. election. In fact, the degree to which the UK stands out is small but significant.

Why is the UK in the crosshairs?

There are a few possible reasons. It could reflect the UK’s higher inflation during 2022/3, although in truth it wasn’t much worse than the Eurozone. The UK’s budget deficit is wide relative to many developed economies, but not the U.S. or France, whose bonds have been less weak. Wage growth has been more persistent in the UK than in the U.S., which makes it harder for the BoE to cut interest rates.

It may partly reflect the political system and budget process in the UK. As the government has an enormous majority, it’s in a much stronger position to pursue a tax and spend policy if it desires. Other countries tend to see protracted periods of negotiation amongst different parties, allowing the markets to absorb and respond to proposed spending increases more gradually.

It could be argued that the Labour government is faced with relatively few institutional constraints due to its parliamentary majority. However, political and market constraints remain. Ensuring the market gains or regains confidence in the government is a function of maintaining the right rhetoric. The Treasury stated on Wednesday that, “no one should be under any doubt that meeting the fiscal rules is non-negotiable and the government will have an iron grip on the public finances”. Then it needs to ensure that actions follow that rhetoric.

The chancellor has set fiscal rules that, at current interest rates, she seems on course to break. Therefore, she may need to consider government spending cuts or tax increases if interest rates don’t drop by March when the next OBR forecasts are prepared.

Will UK taxes be rising again?

Whether UK taxes will be raised depends on a few factors.

The most obvious is the outlook for the UK economy. If the economy remains strong, interest rates will remain high, and the government’s headroom will be diminished. If the economy were very weak, welfare payments would increase. Ideally, continued positive growth with an ebbing of inflation is needed.

In the UK, a rise in government bond yields has a fairly direct impact on the economy. It means that swap rates, and therefore mortgage rates, are likely to continue to increase, which is a headwind for housing market activity. The outlook for house prices has been quite strong in recent months, so it’s unlikely we’ll see price declines – but as mortgage rates creep up and affordability becomes more stretched, there must be some impact on housing market momentum.

Jobs growth is also expected to be weaker because of last year’s increase in employment taxes. If the current trend of weaker jobs growth continues, the BoE will be more willing to cut interest rates and bond yields will decline accordingly. A slowdown in wage growth would be particularly beneficial, as this has been the Achilles heel of the UK economy.

And beyond the UK?

There are external factors to consider here as well. If OPEC (the Organisation of the Petroleum Exporting Countries) countered the increase in U.S. oil production with a price war, inflationary concerns would ebb away quite quickly, but that doesn’t currently seem to be on the cards.

Another external factor would be a global economic slowdown.

Friday’s U.S. payroll growth figures suggest the world’s largest economy is still performing well, perhaps a bit too well. 256,000 new jobs were created during December, well above the forecast. These numbers could be revised but they indicate strength.

It was perhaps fortunate that there was little impact on wage growth, which has slowed over the last year. However, strong jobs growth raises concerns about how the labour market might react if the Trump administration is successful in taming immigration and thereby restricting labour supply.

As far as the balance of risks and opportunities is concerned, the most frequent challenge to the stock market, that of a recession, seems a distant prospect right now. Whether inflation continues to come down is increasingly in doubt.

We shall get a window into that this week, with inflation data for most major economies, including the UK and the U.S, due on Wednesday. Earnings season also begins this week. Earnings growth is expected to be strong over the next year.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Please see the below article from Brooks Macdonald detailing their thoughts on the latest economic data. Received this morning 14/01/2025.

What has happened

Markets have seen a small reprieve from inflation nerves overnight, with Bloomberg reporting that the incoming US Trump-administration is considering a slower ramp-up in international trade tariffs, rather than a ‘one-and-done’ increase. While thought to be better at helping Trump and his team in negotiating global trade concessions, markets have taken it as a potential sign of a slighter softer trade tariff outlook – following this thinking through, with hopes of less tariff pressure and less inflation risk, the US dollar has edged lower overnight while equity futures are up currently.

UK prime minister has “full confidence” in Chancellor Reeves

Monday saw continued pressure on sterling and Gilt bond yields. As the government tried to shore up sentiment, prime minister Starmer announced yesterday that he has “full confidence” in Chancellor Reeves. With the recent jump in borrowing costs eroding most if not all of the financial cushion against her fiscal rules according to some estimates, the risk is that Chancellor will be forced into cutting public spending and/or raising taxes – the next scheduled fiscal update, the Chancellor’s Spring forecast, is due to be held on 26 March.

Rising oil prices add to inflationary concerns

Brent crude oil prices yesterday briefly tipped above US$81 per barrel intraday, reaching their highest levels since August last year. The catalyst was a new round of US sanctions announced at the end of last week, targeting Russian oil revenues – in the crosshairs were Russian oil producers Gazprom Neft and Surgutneftegas as well as Russia’s shadow-fleet of vessels for shipping Russian oil principally to India and China. Investors were left to weigh up the fall-out, with the risk of higher oil prices ahead adding to broader inflation worries in financial markets.

What does Brooks Macdonald think

Tomorrow, we have two sets of consumer inflation data due: US and UK Consumer Price Index (CPI) readings, both for December. For the US, annual core CPI (excluding energy and food prices) inflation was running at +3.3% in November, and for the UK it was higher at +3.5%, both still stubbornly above US and UK central bank inflation targets of 2%. Should this week’s inflation data show a hotter number, that would heap pressure on an already nervous bond market.

Bloomberg as at 14/01/2025. TR denotes Net Total Return.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see below, an article from Tatton Investment Management analysing the key factors currently affecting global investment markets. Received this morning – 13/01/2025

UK bond yield surge – more than meets the eye

Bond markets took centre stage again last week. Globally, yields went up thanks to US economic strength – but UK media focussed on UK bond turmoil, as yields spiked more sharply than elsewhere. The sell-off in UK government bonds (Gilts) was not a ‘Liz Truss moment’ but it was similarly driven by structural selling pressures from UK pension funds. Despite all the talk about Britain’s weak economy, the rise in long-term real (inflation-adjusted) yields should reflect higher growth expectations – even though no one actually thinks growth has improved. The pension fund adjustment helps explain this discrepancy, but it doesn’t help explain why yields also spiked in other bond markets.

We think the global sell-off is a broader story about political uncertainty. Gilt traders don’t trust what the UK treasury says, and we have argued for a while that risk measures for US bonds have been increasing. The latter reflects perceptions of potential instability in the world’s largest economy – both in terms of public debt and the health of US institutions more broadly. Donald Trump’s military threats against NATO allies are clear examples, as are the attempts of his adviser Elon Musk to install preferred far-right candidates in the UK and Germany.

This uncertainty can impact markets. Government bonds being seen as more risky, for example, suggests investors are generally less keen to take on long-term risks. That is a problem for risk assets like equities, and it’s notable that recent bond turmoil coincided with increased volatility in US tech stocks. There is no sign of a broad equity sell-off yet, but this is a warning sign.

Higher real yields means less market liquidity, which increases the ‘gap risk’. UK bond problems are only partly UK-specific. Global yield increases reflect waning risk appetite, in the face of political uncertainty. Politicians should heed bond market signs – regardless of their electoral mandates. If they don’t, the chance of an equity market shakeout increases.

December asset returns review

There was no ‘Santa Rally’ in December, but thankfully none was needed. Global stocks lost 0.9% in sterling terms on the month, but finished 2024 up 19.6% overall, and every major stock market was in the black. Last month’s troubles were mostly down to the US Federal Reserve signalling fewer interest rate cuts. Bond yields rose, making equities relatively less attractive. Big US tech stocks fell in the aftermath – which is strange, as they are cash rich and therefore immune to higher interest rate costs. That suggests a valuation pullback reaction to the Fed, rather than changing economic expectations, and for the month overall tech stocks gained 2% in sterling terms versus a 0.9% loss for broader US equities.

European also dropped 0.9%, but had a tougher 2024 overall, gaining just 1.9% through the year. UK stocks performed the worst in December, losing 1.3% after the Bank of England kept rates steady. Japan was one of the few positive performers last month, gaining 1.1% thanks to the Bank of Japan’s stimulus plans and upwardly revised growth figures. China was the best performer – up 3.6% through December. This was again due to government stimulus expectations, but there were also signs of economic improvement. Incredibly, China was the second best performer in 2024 overall, gaining 18.8% in sterling terms.

December was a drab end to a great year for globally diversified investors. However, after two years of strong returns, some might wonder whether this can be repeated in 2025, and whether December’s wobble might be the start of something worse. We don’t think last month’s troubles say much about the market mood (it looked more like year-end rebalancing) but there is a lot of economic activity expectations ‘priced in’ to markets. Assets aren’t under threat, but returns might not live up to recent standards.

Global earnings growth

Stock markets are at the moment more sensitive than usual to earnings growth expectations. Analysts think US earnings will yet again power ahead of other regions in 2025, and investors seem to agree. This is largely about Donald Trump: markets think tax cuts and deregulation will help American companies, while tariffs will hurt global companies. Business sentiment indicators back this up, as does recent retail sales data – suggesting US consumers buy the American exceptionalism story. Some worry that tariffs might undermine confidence, but they could also mean that a larger share of US consumption filters through to US corporate profit.

US outperformance is also about underperformance elsewhere. European companies are suffering from weak demand and high energy costs. UK profit expectations are gently improving, but from a low base. Japan’s corporate earnings have been relatively strong, but are stable rather than growing. We have argued before, however, that markets are overly pessimistic about growth outside the US. This negativity is probably clearest in Europe, where investors are arguably ignoring the upsides that might come from more accommodative monetary (and perhaps even fiscal) policy.

We’re less convinced about US dominance. There is a worrying divergence between the ‘soft’ sentiment data and the ‘hard’ economic data. It is hard to see how smaller companies can improve while interest rates are still high – and Trump’s policies have already pushed the Federal Reserve into a tighter stance. This might not be a problem if the biggest US tech stocks can maintain their stellar profits, but that would be doubtful if their customers are less healthy than hoped. US earnings growth will likely outperform for the first half of 2025, but the current projections seem too optimistic. Markets could be setting themselves up for disappointment. We will keep a close eye on earnings expectations in the months ahead.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Please see the below article from EPIC Investment Partners received this morning 10/01/2025:

The dreaded congestion charge has finally made its way across the pond with New York City drivers now being charged $9 (£7) to enter parts of Manhattan during peak hours. The Metropolitan Transportation Authority (MTA) expects the scheme, the first of its kind in the US, to reduce traffic by 10-20% and raise USD 15bn for transit infrastructure improvements. The programme, launched on Sunday 5th January, aims to decrease vehicle traffic by 80,000 per weekday in an area that typically sees 500,000 to 700,000 vehicles daily.

According to traffic-data analysis firm INRIX, in 2024 New York suffered some of the worst traffic in the world, with drivers losing 102 hours resulting from peak commuting congestions, only to be topped by Istanbul at 105 hours. For context, Londoners are fourth on the list, having lost 101 hours. It seems INTRIX hasn’t made it into Lagos yet.

The congestion pricing initiative faces several challenges, including safety concerns about public transit alternatives, ongoing legal battles, and potential opposition from the incoming Trump administration.

The MTA plans to use the revenue for crucial infrastructure projects, including extending the Second Avenue subway to Harlem and modernising train signals. Critics worry about the economic impact on businesses and commuters, while supporters emphasise the environmental and transit benefits. The programme includes various discounts and credits, with fees set to increase to $12 in 2028 and $15 in 2031.

If New Yorkers think they are getting a raw deal, spare a thought for London drivers who shell out more than double their NY counterparts (£15), seven days a week. By 2028, most Londoners will be listing their kidneys on eBay just to make the daily commute. Driving in big cities is looking to become a luxury activity, right up there with buying a house or affording avocado toast.

Please continue to check our blog content for advice, planning issues and the latest investment market, and economic updates from leading investment houses.