Please see below an article from Fidelity which was published late last week and received late yesterday afternoon and covers Fidelity’s views on the US Federal Reserve and its potential movements in 2022:

As you can see from the above, the Fed remains focused on inflationary pressures and some action is likely to be needed to help curb these pressures. However, now is the time for potential policy mistakes by moving too soon or too aggressively on interest rate hikes. This needs to be managed carefully. The Fed appear to have a good grasp of the key issues at the moment and their communication to date is better than the Bank of England’s.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please find below an article detailing the impacts of Covid on stock markets and investments, received from AJ Bell yesterday – 19/12/2021

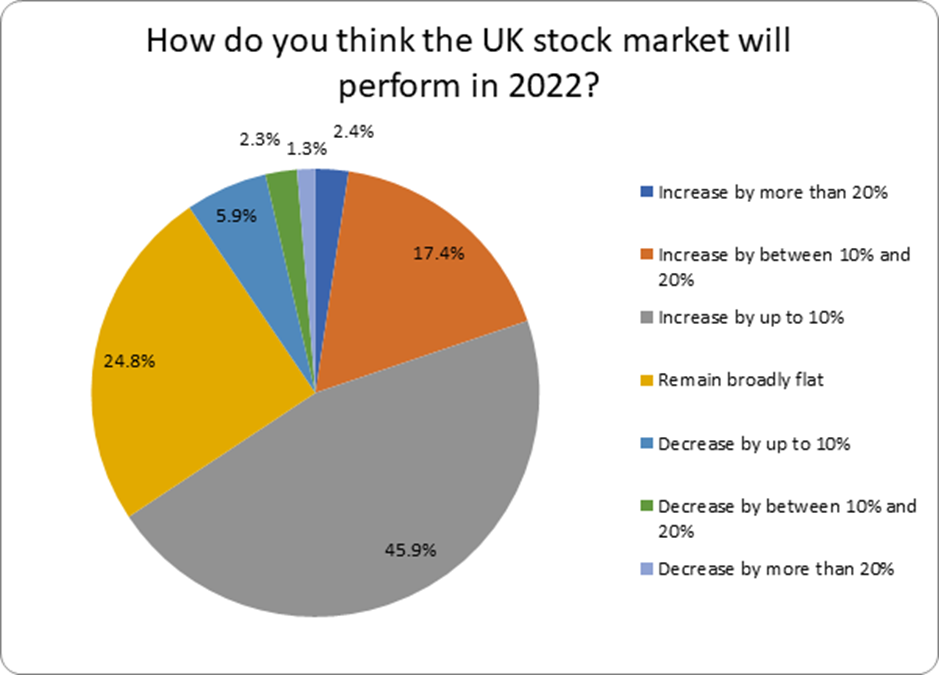

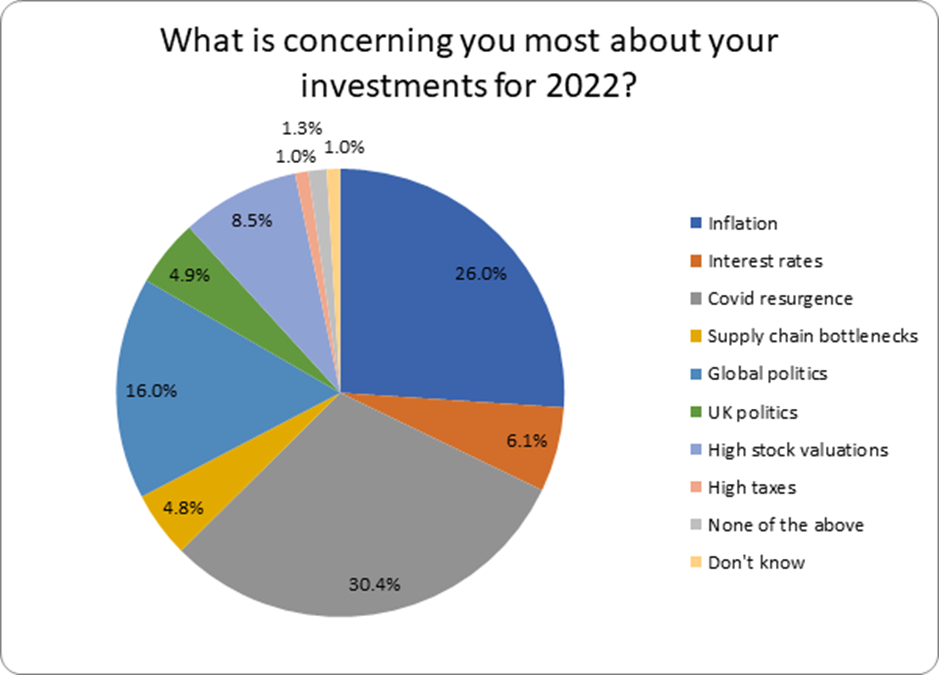

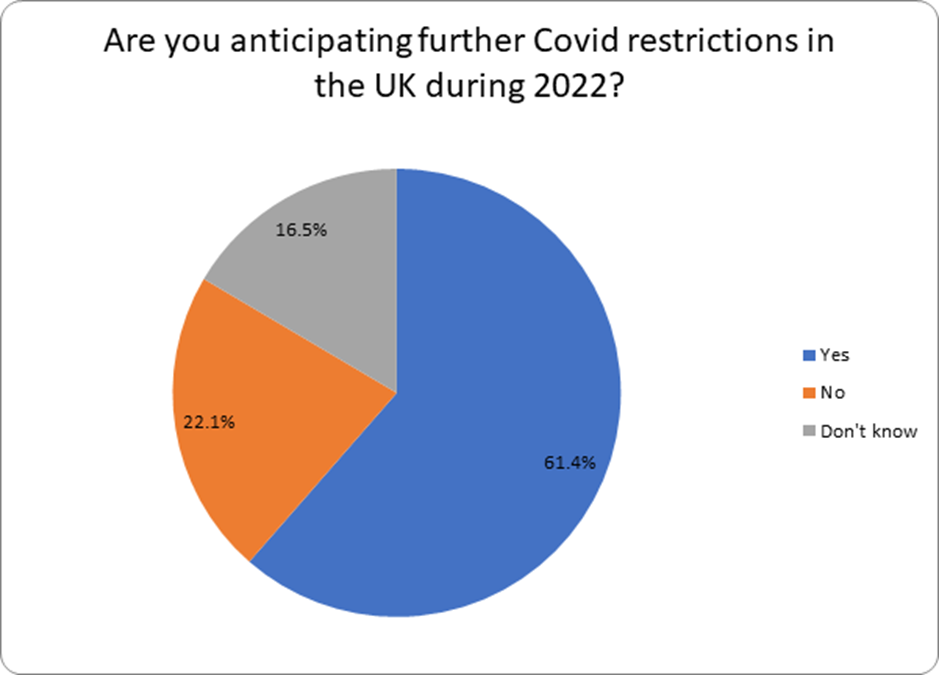

DIY investors are entering 2022 in a mood of constructive realism, recognising market risks, but also largely confident in their investments. Six in ten expect further covid restrictions in 2022, and a resurgence in the pandemic is the number one worry for investors as we head into the new year. Indeed, covid is seen as a greater risk than inflation, which makes sense seeing as the stock market provides some protection from price rises. Inflation comes a close second in the list of concerns for 2022 though, which shows investors are wary of price rises and the effect this may have on their portfolios. Global politics and high stock valuations are also cause for concern for some investors.

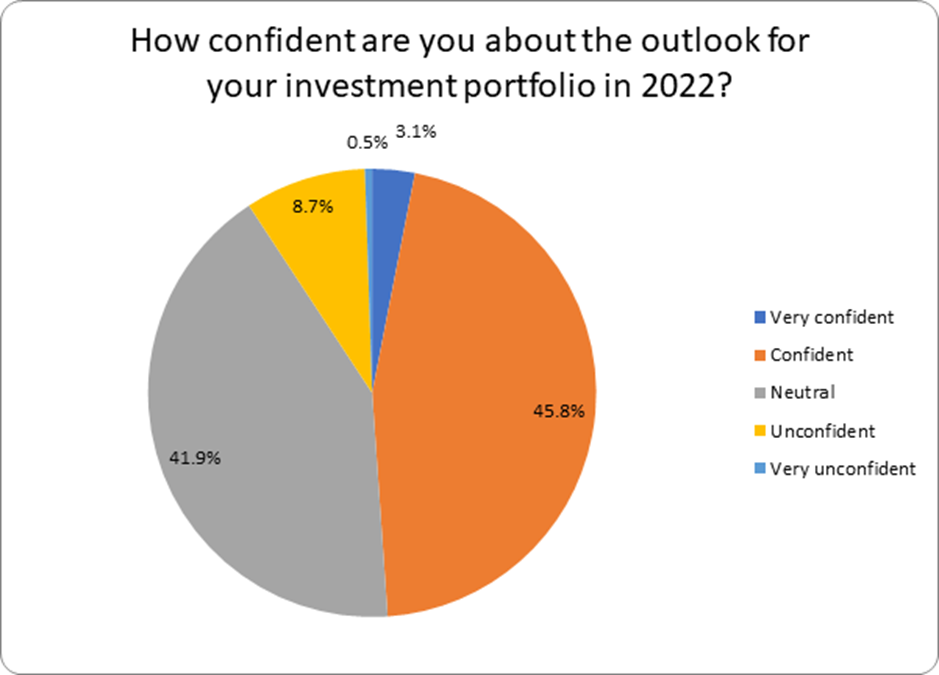

On the whole though, investors see the glass as half full rather than half empty. About 50% were confident or very confident about their investments in 2022, and around four in ten were neutral. That’s also reflected in forecasts for the Footsie, with two thirds of investors (65.7%) expecting the UK stock market to make further ground over the course of the coming year. Almost half of investors expect single digit returns in 2022, which suggests investors aren’t getting carried away, and are settling in for a more modest year for growth than 2021.

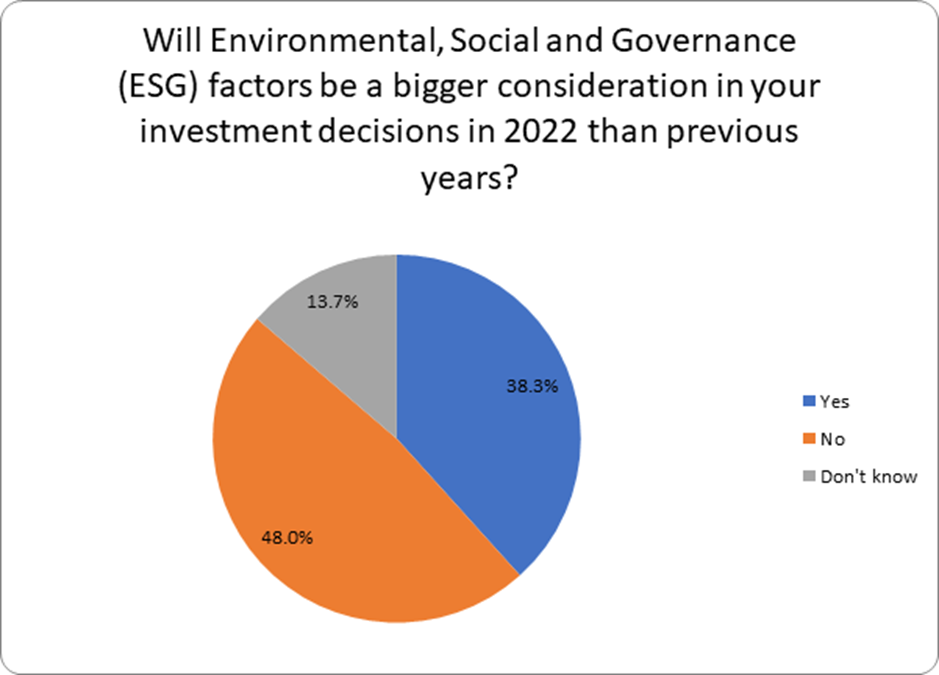

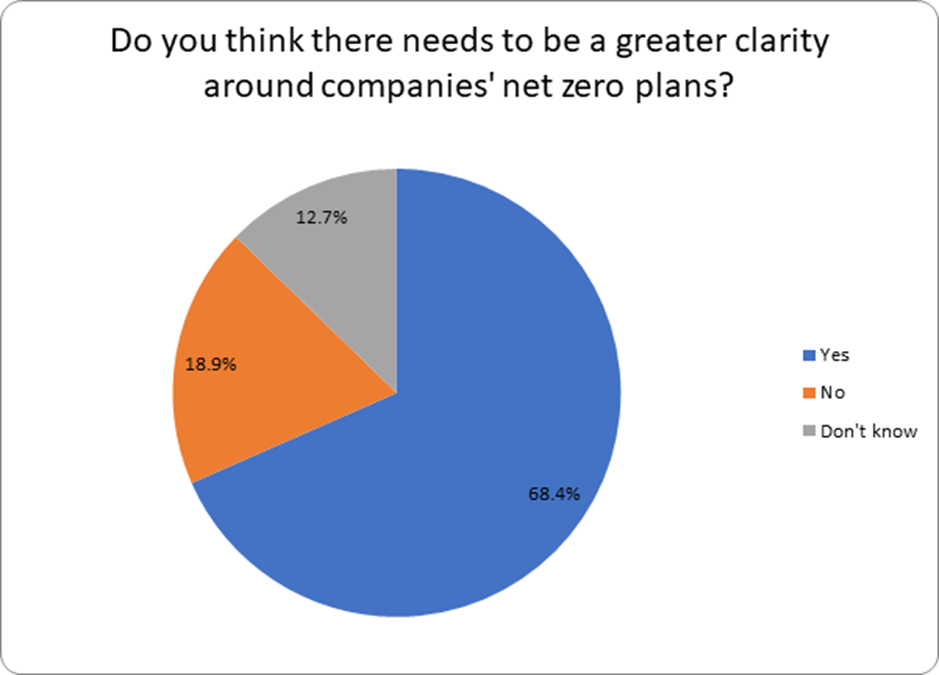

Investors are also becoming more attuned to ESG considerations, with four in ten (38.3%) saying these were going to play a bigger part in investment decisions in 2022. There’s already been a groundswell of interest in ethical funds in the last two years, and our survey suggests this isn’t going to abate in 2022. More than two thirds of investors also said they think there should be grater clarity over companies’ net zero plans.

The ESG agenda has developed so rapidly across the investment industry that the information available to investors is struggling to keep up. The FCA is formulating proposals on a new green labelling regime, expected in the first half of 2022, which should help make things a bit easier for investors seeking ESG investment options.

Please continue to check back for a range of blog content from us and from some of the world’s leading fund management houses.

Please see article below from Invesco received yesterday – 16/12/2021

Global Equities have nothing to fear

We are living in one of the most noteworthy periods of change in history. The internet and the digitization of nearly everything have created some massive new industries.

In the scientific space, the mapping of the human genome at the beginning of the century has yielded new ways of treating some of our most challenging diseases, including Covid-19.

Our philosophy is focused on durable structural change. We don’t follow cyclical trends, instead the central themes in our investment strategy are for the long-term. As we head into 2022, we are not looking to what excites us just for the year ahead, but what excites us over the next 3-5 years.

The formidable networks of the tech giants

Alphabet, Facebook, Amazon, Mastercard and others in our Invesco Global Focus Equity Fund, are great companies with deep intellectual libraries and formidable network effects.

There is nothing temporal or fleeting about the size and scale of their advantage, these companies have created, or are operating within, economic ecosystems that have expanded structurally.

Perhaps the most important thing to understand about networks is that, once entrenched, they can only be displaced by the creation of an entirely new one. That’s a tough task. People are on Facebook, Google and Amazon because everyone else is, too.

Meanwhile, credit cards were the earliest iteration of digital payments. There are now a myriad of ways to send money to people to pay for things online or in a store. The use of these by consumers is only going to increase.

Companies are transforming IT functions

IT departments are planning to move much of their software from an on-premise platform to the cloud, facilitated by Amazon Web Services and Alphabet, along with other players in the world.

This is no small thing. It represents a huge shift in the IT stack that has a long way to go. Software in the cloud rids the enterprise of some of the big capital outlays and a lot of hardware that is costly to maintain. The best innovations, the ones that represent a structural shift, always deliver an outcome that is both better and cheaper.

As a part of the move to the cloud, cyber security in enterprises have undergone an overhaul. Instead of only having to secure a single premise, there are now a myriad of endpoints, and many things running in the cloud. This means a different toolkit is needed for network security.

That is a big evolving field that is growing in importance as networks get distributed and their workloads shift to the cloud. CrowdStrike has built the first fit-for-purpose cloud-based security software. It is not an adaptation of legacy on-premise software, it was designed to secure modern network endpoints, and modern threats and it is growing very rapidly.

The chart below shows that the growth of spending on security is significantly outpacing the growth of IT spending overall, a trend which should provide a continued tailwind for CrowdStrike in the years to come.

Source: Bloomberg Intelligence, IDC

Drug development evolving following the mapping of the genome

Elsewhere, the mapping of the human genome completed around 20 years ago has created new opportunities for drug development and clinical research.

We are now seeing its impact, both in the method of drug development and clinical research. The development and manufacture of the Covid-19 vaccinations is a direct result of that. The virus was quickly genetically sequenced on an Illumina sequencing machine, enabling it to get to market fairly rapidly by customary standards. Normally, commercialising a medicine usually takes a few billion dollars and 10 to 20 years to come to fruition.

We are, however, in the early stages of this theme. We have chosen to invest in companies such as Illumina, diabetes giant Novo Nordisk and Thermo Fisher Scientific, a provider of a wide array of diagnostic and lab equipment sold to research labs, hospitals and the biotech and pharma industry. Each is the leading global player in their respective arenas with strong intellectual property rights and substantial long-term opportunity.

Standing the test of time

The market narrative in 2021 was all about the cycle, even though there are some profound changes happening all around us. The thing about cycles is that they are just that, they are passing, reflecting a temporal change in preference.

Structural change, of the sort we look for, is much bigger than that. It doesn’t separate the world into cyclical or defensive, it separates it into winners and losers, and the losers fade into obscurity.

The portfolio we hold today was not assembled to perform only in a tailored environment. What drives our holdings isn’t complicated. Their growth rates and economic profitability have been going up together. The market is what it is, but we are invested in a portfolio of 35 businesses, with each holding a significant competitive edge in an expanding economic ecosystem.

Many pieces we read from the ‘outlook’ genre touch on subjects that keep the writer up at night, or challenges they expect in the year to come. The truth is, for us, there’s not a lot that scares us as we head into 2022 or the years that follow.

While negative headlines may drive a few bad weeks or a few bad months for your equity portfolio, they shouldn’t scare you as a long-term investor. In fact, negative headlines often create the temporary pullbacks in stock prices that can set you up for fantastic long-term returns in the years ahead.

In our years, we’ve seen all manner of inflationary scares, geopolitical tensions, terrorist attacks, currency crises and the like, but none of them have mattered to generating long-term returns for our clients.

As those that follow our strategy may recall, what we think matters most is buying durably advantaged companies at the right price, run by management teams we can trust to do the right thing with shareholders’ money. If we can find opportunities like that and invest in them with conviction, good outcomes will follow over a 3-5 year investment horizon. The rest is just noise.

Please continue to check back for our latest blog posts and updates.

Please see below an interesting article received from AJ Bell this afternoon, which offers key potential market-related scenarios for the 12 months ahead as we approach the end of this year.

No-one, not even central bankers, knows what is ahead of us in 2022, and whether inflation, stagflation or deflation will result from the combination of the pandemic, lockdowns and supply-chain chaos on one side, and massive amounts of fiscal and monetary stimulus designed to boost demand on the other.

Going ‘all in’ on one scenario is probably not going to be good idea and portfolio construction will need to address range of outcomes, as frankly anything is possible (especially given the likelihood of central bank and government interference action). Keeping an eye on the following charts – and investment decisions – may help investors sense which way the wind is blowing so they can try to obtain the best possible risk-adjusted returns for their portfolios

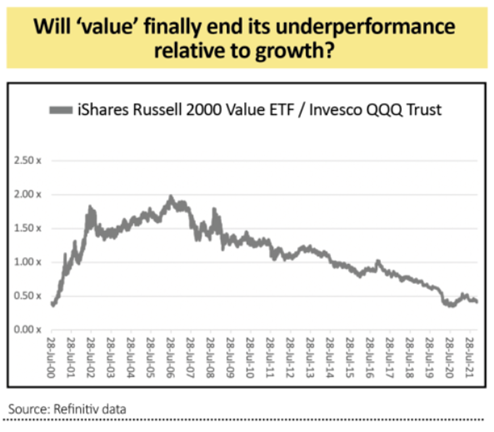

‘Value’ versus ‘growth’

For want of a better turn of phrase ‘growth’ has outperformed ‘value’ for the thick end of a decade, thanks to the prevailing, low-growth, low-interest-rate, low-inflation fog which has enveloped the globe.

If that environment persists, firms which are seen as capable of providing secular trend increases in sales, profits and cash flows (or maybe even just the first one) will remain highly prized. If it changes, and inflation and strong nominal GDP growth take over, then there would be no reason to pay high multiples for secular growth when cyclical growth (or ‘value’) would be available at much lower valuations. Industrials and banks could then lead the charge.

One way of measuring whether this shift in leadership is happening is by comparing the performance of the Invesco QQQ Trust, packed with growth stocks, against the iShares Russell 2000 Value ETF. If the line goes up, value is doing better, and vice-versa. Value’s latest attempt for glory is petering out a little, perhaps owing to worries over Covid variants and the effects of higher prices and clogged supply chains on economic activity.

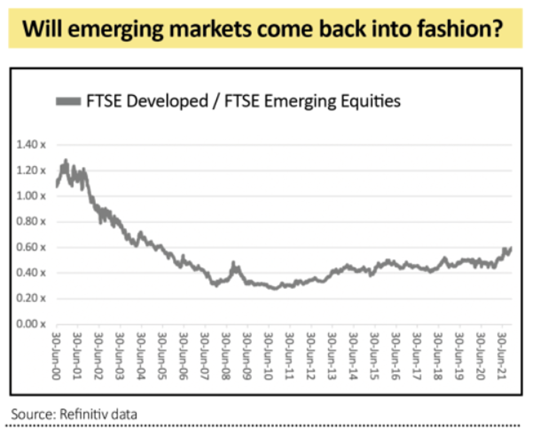

‘Developed’ versus ‘emerging’ markets

Emerging markets dominated for the first decade of this millennium but developed ones have subsequently ruled the roost. Demographics, debt-to-GDP ratios and the possible trend toward ‘onshoring’ in the West are all factors here but it seems reasonable to expect export-driven emerging markets to fare relatively well if global growth rates pick up. Any attempts by China to loosen monetary policy and stoke growth could also help emerging markets, where the Shanghai market has a big weighting.

Real and paper assets

Looking at the relative performance of the Bloomberg Commodity and the FTSE All-World (equity) index, commodities and ‘real’ assets outperformed between 2000 and 2010 but equities and ‘paper’ assets have dominated since.

Again, this trend could be reasonably expected to continue if we stay stuck in a low-growth, low-rate, low-inflation world. But if inflation (or maybe stagflation) take hold, ‘real’ assets could come to the fore for three reasons: they could be stores of value; central banks may keep printing money but they cannot print oil, gold or property; and investment in finding new resources is dwindling thanks to pressure from politicians, investors and the public alike amid environmental concerns.

All that glitters

The subject of ‘stores of value’ and ‘haven assets’ can lead to heated debate. It is hard to argue that Bitcoin is a store of value, given the wild price swings of the last five years, and the same accusation can be levelled at gold. Neither produces a yield. And both trade way above their marginal cost of production.

Yet rampant deficit creation by governments and money printing by central banks (in an attempt to effectively monetise and fund the extra debt) do persuade many to make an investment case for one or the other (although rarely both).

Gold did next to nothing and underperformed Bitcoin again in 2021. But its role as a haven during times of great uncertainty – when it looks like the authorities are not in control – could come into play if inflation gallops higher. The gold price relative to Bitcoin makes for an interesting chart but the metal may remain dormant if inflation fizzles out.

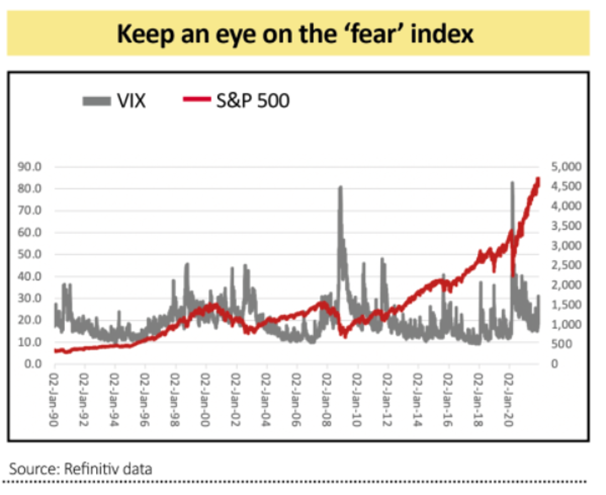

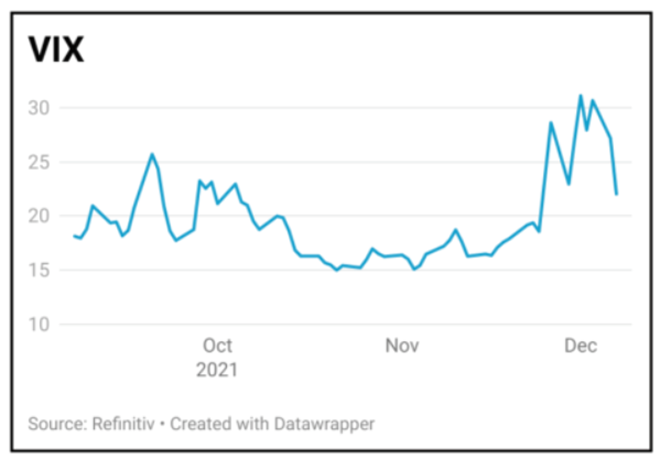

Chop and change

After a brief foray to 30 on news of the Omicron variant, the VIX, or ‘fear,’ index which gauges future volatility in the US stock market, is trading pretty much in line with its long-run average of 19. If markets retain their faith in central bank control, inflation remains subdued and the variant passes by, fear will likely dissipate. But if inflation takes hold and confidence in policy makers ebbs, volatility may make its long-awaited comeback.

Please check in again with us shortly for further relevant content and news as we countdown to Christmas and the New Year.

Please see below, the weekly market commentary from Brooks Macdonald, providing an update on monetary policy and the ongoing risk of the Omicron variant – received yesterday afternoon – 13/12/2021.

Equities rallied strongly last week as Omicron fears eased

This week sees the Federal Reserve, European Central Bank and Bank of England announce their latest monetary policy

Existing vaccines are shown to provide good protection against Omicron, accelerating the importance of booster jabs

Equities rallied strongly last week as Omicron fears eased

Last week saw an uptick in optimism around the Omicron variant with equities benefitting from a broad rally early in the week that favoured cyclical and tech sectors. The rally lost steam by the end of the week, but this is more of a reflection of the sharp gains on Monday/Tuesday rather than a sudden bout of fear.

This week sees the Federal Reserve, European Central Bank and Bank of England announce their latest monetary policy

This week could be pivotal for central bank policy, with eight of the G20 central banks reporting on their latest policy. Those eight contain the Federal Reserve (Fed), European Central Bank (ECB) and Bank of England, with all of those banks expected to be considering a change to their monetary policy. Starting with the Fed, with the Consumer Price Index number last Friday in line with (elevated) expectations, an acceleration of the Fed’s tapering programme looks likely. Should the speed of asset purchase tapering double, for example, this would lead the current process to conclude in March and leave some room for the Fed to consider the timing of their first rate hike. This week’s Fed meeting will also provide the latest ‘dot plot’ of interest rate expectations so there is a lotto focus on. The ECB was expected to unveil a shift in policy towards rates guidance rather than liquidity guidance, in essence a slight pivot towards tightening policy. Given Omicron, this may be delayed until the New Year but it is a close call. In the UK, the Bank of England is expected to raise interest rates by 0.15% to 0.25%but again this is dependent on how the bank interprets the latest Omicron risk which has certainly grabbed headlines this weekend.

Existing vaccines are shown to provide good protection against Omicron, accelerating the importance of booster jabs

On Friday, the UK released a report looking at the efficacy of three Pfizer vaccine doses (two initial, plus a booster) which showed a c.75% effectiveness against symptomatic disease. The data underlined the importance to governments of the booster campaign and plans were announced to offer all adults in England a booster by 31 December. Omicron’s growth rate appears to be significantly higher than delta and this is causing governments to release some quite daunting predicted case numbers.

With each day that goes by, financial markets are building confidence that Omicron will be less severe than delta but that it will spread rapidly, leading to some nervous moments. Short term restrictions are likely across the world as governments buy time for their booster rollout. Looking forward though, investors are more sanguine.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below an article which was recently published and received early this morning from J.P. Morgan and cover their views on sustainable investments:

As you can see from the above, ESG factors are becoming more prevalent for everyone and to start the decarbonisation process, this will require a significant amount of investment globally. The level of investment required to start this shift will present opportunity for investors and we think ESG investing will become more mainstream in the future.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below article received from AJ Bell yesterday afternoon, which suggests that investors appear to have decided the new Covid-19 variant won’t derail economic growth.

Stock markets hate uncertainty, and the arrival of Omicron has created an information vacuum which is likely to persist until scientists and economists get to grips with the likely health and economic effects caused by the latest variant of concern.

On 26 November, the so-called fear gauge, the VIX index, spiked higher as investors scrambled to hedge their portfolios, sending US markets down by around 2%.

UK and European markets dropped by more than 3% with travel related shares and economically sensitive stocks, such as banks, taking the brunt of the fall.

British Airways owner International Consolidated Airlines dropped by as much as 20% and Lloyds dropped by close to 10%.

Commodities like oil and copper sank as markets moved to price in lower global growth, while interest rates dropped.

Comments from Moderna chief Stephane Bancel prompted another sell-off in markets on 1 December after he predicted a ‘material’ drop in effectiveness from current vaccines against the new variant.

Fed chairman Jay Powell added to uncertainty on the same day after he surprised markets by saying the US central bank would discuss an increase in tapering (removing stimulus) at the December meeting, which sent bond yields higher and prices lower.

Elevated volatility saw the VIX index climb from 18.58 on 24 November to 31.12 on 1 December. Historically, large spikes in the VIX index have been associated with ‘market capitulation’ and higher future stock prices.

Sentiment already appears to be shifting. The VIX has since dropped back to 22.02 and at the time of writing (7 Dec), the FTSE 100 index had recovered all its losses since the variant first dominated the headlines, and was trading slightly above pre-Omicron levels.

The index has been helped by a strong rebound in index heavyweights Royal Dutch Shell and BP.

After falling as much as 15% on Omicron worries oil prices have staged a recovery rally following a meeting of oil producers’ cartel Opec+ (Dec 2) where Saudi Arabia and its allies agreed to press ahead with efforts to increase production by 400,000 barrels a day each month.

Opec+ also hinted it would adjust production if necessary, which seems to have provided support to prices. Brent Crude has risen by around 8% to $71.70 per barrel since the meeting.

Before the Opec+ meeting several countries including the US, China and the UK had indicated they would release supplies from their strategic oil reserves to help curb prices.

We endeavour to publish relevant content and market news regularly throughout the festive period, so please check in again soon.

Please see investment bulletin below from Brooks Macdonald received yesterday – 08/12/2021

What has happened

The rally in US and European equities continued on the back of renewed optimism that Omicron may be less of a headwind to the broader reopening narrative than previously feared. The headline US and European equity indices were both up over 2% with cyclical sectors and technology outperforming. The quid pro quo of this optimism is that bond markets are pricing in an earlier hike from the Fed and other central banks. Indeed, the market is now fully pricing in a June hike and an over three-quarter probability of a hike as soon as May next year.

US/Russia

The call between President Biden and President Putin took place yesterday amidst heightened tensions over Ukraine. During the two-hour call President Biden warned Russia of ‘strong economic and other measures’ if the country was to send troops into Ukraine. The US is also preparing a package of sanctions to deploy if Russia was to invade regardless, these include blocking the Nord Stream 2 pipeline and conversion access to US Dollars. The US is building this consensus sanctions package with European leaders, particularly Germany, to convince President Putin of the economic risks of military incursions at the Ukraine/Russia border.

COVID

Whilst investors are taking a more positive medium-term view, global COVID cases are rising. Governments continue to roll out tougher restrictions including an extension of Canada’s vaccine mandate and Sweden introducing COVID passports. Mirroring the actions in the previous 2021 waves, governments have been eager to preserve the freedoms for the vaccinated whilst providing further incentives to those who are not jabbed, to come forward. Austria, which went into lockdown a few weeks ago, is beginning to gradually reopen shops to the vaccinated next week with hospitality opening the week after.

What does Brooks Macdonald think

In a more normal week, the end of Chancellor Merkel’s 16-year tenure would be major news but with Omicron grabbing most of the headlines, this has been demoted. Chancellor Merkel has been a powerful force domestically as well as within the EU, helping navigate the financial crisis, Eurozone debt crisis and COVID. Today the Bundestag will vote on the next Chancellor with Olaf Scholz set to take over which will be a formality now that the fresh coalition has been agreed.

Another quick update from Brooks Macdonald, these regular investment bulletins help us keep up to date with what is happening in the markets.

Please continue to check back for our latest blog posts and updates.

Please find below a ‘Markets in a Minute’ update, received from Brewin Dolphin, yesterday evening – 07/12/2021

The S&P 500 has surged over the past 20 months. Could the spread of the Omicron variant spark the first correction of the bull market? Paul Danis, our Head of Asset Allocation, provides context and discusses the outlook.

Last Friday saw a sell off in higher risk asset classes when the Omicron variant of Covid-19 suddenly landed on everyone’s radars. The news was poorly received as many investors had become quite relaxed about the virus. The S&P 500 fell 2.3% – its biggest one-day loss in nine months – while the pan-European STOXX 600 slumped 3.7% in its worst session since June 2020.

Economic growth-sensitive plays like small caps underperformed. At the industry level, it was the travel[1]sensitive airline, hotel, restaurant and leisure sectors, oil-sensitive energy plays, and yield-sensitive banks that were among the worst hit.

Where do we stand now after the Omicron[1]induced sell off?

Notwithstanding Friday’s selloff, global equity markets have surged over the past 20 months, led by the US. As of the end of November, the MSCI All Country World Index is up 89% (in US dollar terms) from the March 2020 low. The US large cap benchmark, the S&P 500, is up 104%. We focus on the S&P 500 in this article because it represents over 60% of the global equity market cap, it acts as a bellwether for equity bourses around the world, and US equities constitute our largest overweight position.

Although there have been several US equity bull markets that have seen much greater total price appreciation than what has occurred so far this cycle, what has made this cycle’s bull market stand out is the intensity of the rally. This cycle, the S&P 500’s annualised performance since the bull market began is just over 62%. Looking at all the bull markets where the total gain has been at least 100%, one must go back to the early 1940s to find rallies that have been as intense.

What’s more, we have now gone much longer than the average length of time without seeing a 10% correction in the S&P 500. Since the late 1920s, the average time between the start of a bull market and an S&P 500 decline of 10% or more is about a year and two months. This cycle, we’ve gone about a year and eight months without a 10% correction. The worst we’ve had was a 9.6% decline in September last year, and a milder 5.5% pullback in September this year.

Is Omicron enough to spark the first 10% correction of the bull market?

It’s possible. How much downside we get will be determined by what the data show in terms of Omicron’s ability to evade vaccines and natural immunity, as well how dangerous it is. The good news is that a lot of work has already been done to find solutions to Covid-19. As such, if it turns out that Omicron poses a new serious challenge, the world is in a better place now to address it.

Preparing new vaccines is not trivial, but it would be a shorter and more certain process than the development of the original vaccines. Furthermore, we also have some effective treatments for Covid-19. These are not expected to be impaired by the new variant.

When compared to the historical averages cited above, the S&P 500 bull market is looking long in the tooth. Other concerns include extended valuations, profit margins that are at risk of turning lower, and the likelihood that we may soon enter a slower growth phase in the global economic cycle. With all this in mind, the next 12 months are likely to prove bumpier than the past 20 months for equity investors. Nevertheless, it looks like the equity bull market is still on a solid foundation. Importantly, The S&P 500 has surged over the past 20 months. Could the spread of the Omicron variant spark the first correction of the bull market? Paul Danis, our Head of Asset Allocation, provides context and discusses the outlook. Could Omicron derail the US equity bull market? 01 December 2021 we believe the economy will continue to expand at a healthy pace. Based on cycles from 1990, the S&P 500 peaks on average two months after the unemployment rate begins to rise.

Is there continued scope for the labour market to improve?

The US unemployment rate has already dropped a lot. It is currently at 4.6%, significantly lower than the April 2020 high of 14.8%. The Omicron variant creates new uncertainty, but most of what we are seeing suggests it will go down further. Importantly, US households are still sitting on roughly $2.5trn in excess savings built up during the pandemic. True, there have been signs of weakness from the all-important US housing market, such as housing starts. But that does not appear to be because of weak demand. Rather, supply bottlenecks appear to be the problem, with homebuilders struggling in terms of hiring workers and with the high price of building materials. Housing units authorised in the US have attained new highs, which likely indicates some pent-up demand.

Is there anything else supporting the equity market?

There are some silver linings to the Omicron-induced sell off. On the greed and fear spectrum, the Omicron news turned the dial meaningfully toward the latter. On that front, the market’s ‘fear gauge’, the VIX index, hit the highest level since February on Friday. A healthy level of fear in the market tends to be more supportive of future gains compared to a backdrop of greed/complacency.

In addition, the market is now pushing back expectations of Federal Reserve interest rate hikes. The Fed’s continued willingness to stimulate the US economy, by keeping interest rates low, is also something that should support equities.

Aren’t equities now just too expensive?

It is true that equities are expensive by historical standards. But so are bonds, and investors are disincentivised to hold cash, thanks in large part to the Fed’s accommodative policy stance. The inflation-adjusted ‘federal funds rate’ is currently below -4%. This means investors’ cash holdings are depreciating in real terms at an annualised rate of over 4%. These low real yields on cash and bonds combined with solid corporate profits growth are keeping the yields on equities at relatively attractive levels even after such a strong rally.

So, you remain bullish – what are the risks?

Omicron is clearly a big one. Another is that the Fed will end up tightening policy sooner than most expect. This could happen if long-term inflation expectations change. While ten-year inflation expectations implied by US inflation-linked bonds are elevated, they are not at extreme levels. Other measures of inflation expectations also suggest the market is not overly concerned about inflation over the longer-term. While there’s no room for complacency on inflation, the data are not behaving in a way that would make one believe the Fed will imminently pull the rug out from under the equity market.

Conclusion

The emergence of the Omicron variant is undoubtedly a concern. Nevertheless, on a 12-month view, we believe that a continued overweight in equities and underweight in bonds is appropriate. Equity investors are likely to be in for a bumpier ride over the next year. But with the economic outlook still largely positive and given the Fed’s currently supportive policy stance, it looks like the equity bull market remains on a reasonably solid foundation.

Please continue to check back for a range of blog content from us and from some of the world’s leading fund management houses.