Please see below the Brooks Macdonald Daily Investment Update, received this morning – 16/07/2026

What has happened?

Markets rallied yesterday after a softer-than-expected US producer price inflation (PPI) report reinforced expectations that the Federal Reserve is unlikely to raise interest rates at its upcoming meeting. The S&P 500 rose +0.38%, closing less than 0.5% below its record high, while strong corporate earnings provided additional support, with BlackRock gaining +6.6% after beating expectations. Oil prices also stabilised following their recent surge, with Brent crude rising just +0.26%. By contrast, European markets were more mixed. The STOXX 600 edged up +0.10%, but Germany’s DAX (-0.59%) and Italy’s FTSE-MIB (-0.85%) declined as bond yields moved higher amid lingering inflation concerns. Despite the pullback in oil prices, European natural gas futures climbed to a fresh three-month high of €54.35/MWh.

US PPI reinforces a disinflationary picture

June US PPI fell -0.3% m-o-m, compared with expectations for no change, while May’s reading was revised down sharply. As a result, annual producer price inflation slowed to 5.5%, below the 6.2% consensus forecast. Importantly for investors, there were also no obvious signs of inflation pressure from the components that feed into the Fed’s preferred PCE inflation measure. The data helped reinforce a dovish repricing across markets, with the probability of a Fed rate hike at the next meeting falling to around 10%, its lowest level since speculation about an imminent hike first emerged.

Political clarity boosts UK assets

The UK was a notable outperformer following reports that Shabana Mahmood is expected to become Chancellor under incoming Prime Minister Andy Burnham. The announcement was closely watched by investors and helped lift sterling 1.1% against the US dollar. Gilts also outperformed, with the 10-year yield falling 3.8bps to 4.94%, moving in the opposite direction to most continental European bond markets.

What does Brooks Macdonald think?

The latest US inflation data provides some reassurance that underlying price pressures remain more contained than headline energy moves alone would suggest. That said, investors should be careful not to draw too many conclusions from a single data point. Energy markets remain vulnerable to disruption. For now, however, markets appear increasingly comfortable with the view that policy rates will remain stable.

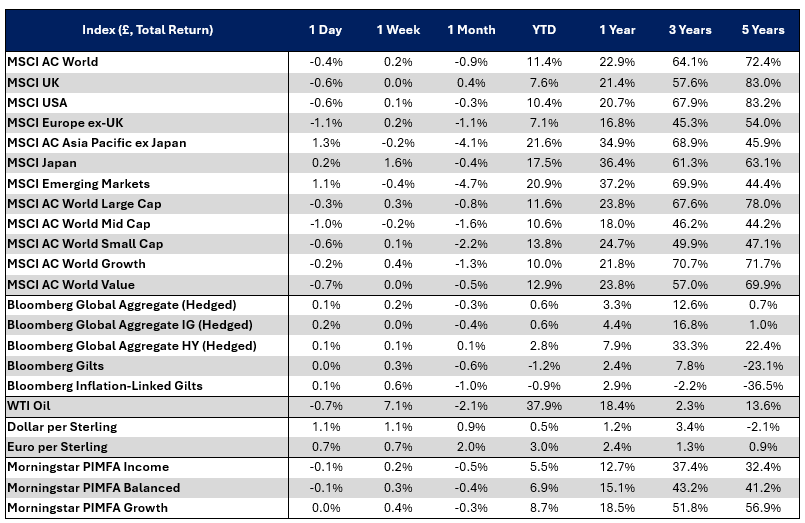

Bloomberg as at 16/07/2026.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Alexander James Roberts

16/07/2026