Please see the below article from Brooks Macdonald detailing their discussions on UK and US markets. Received this morning 10/02/2026.

What has happened?

Global equity markets extended their rebound yesterday, with the S&P 500 (+0.47%) closing just shy of a record high and the STOXX 600 (+0.70%) reaching another all time high. Technology stocks led the move, reversing much of their recent weakness, and the S&P 500’s software segment (+3.36%) registered its strongest daily gain since May last year. The recovery in sentiment also lent support to other asset classes, including gold (+1.88%), while broader newsflow remained relatively muted. US Treasury yields drifted lower following comments from NEC Director Kevin Hassett, who suggested that markets may see “slightly lower jobs numbers” in tomorrow’s delayed January employment report, though he cautioned that such an outcome “shouldn’t trigger any panic.”

Political unease pressures UK markets

UK assets came under renewed pressure as domestic politics returned to the spotlight. Gilts weakened from the open after weekend news of the Prime Minister’s chief of staff stepping down. The selloff intensified as Labour’s leader in Scotland publicly called on PM Starmer to resign, prompting concerns that any change in leadership could lead to looser fiscal rules and higher borrowing. At the intraday peak, 10 year gilt yields were more than +8bps higher and 30 year yields around +9bps, though both moves eased significantly after the full cabinet expressed support for the Prime Minister. Even so, UK markets lagged global peers, with the FTSE 100 (+0.16%) delivering only a modest gain.

What does Brooks Macdonald think?

Hassent’s comments were framed as part of a broader discussion around slowing population growth and improving productivity, rather than a warning about imminent weakness. However, markets remain cautious heading into tomorrow’s delayed January jobs report, given its potential influence on expectations for the Federal Reserve’s policy path. While one data point is unlikely to shift the overall narrative meaningfully, any moderation in job creation or wage growth could reinforce the case for a gradual cooling in labour market conditions.

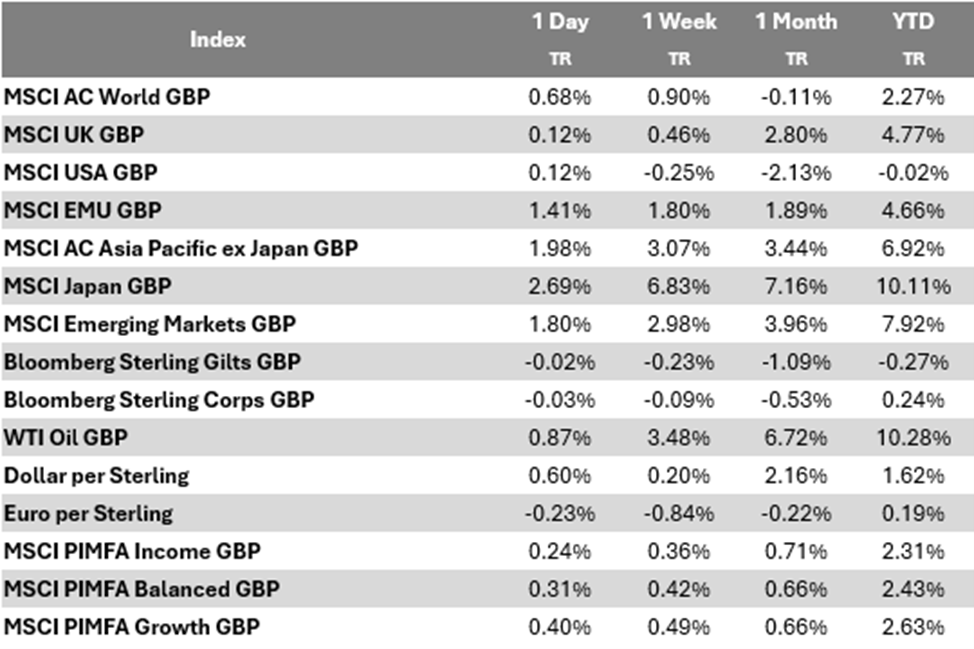

Bloomberg as at 10/02/2026. TR denotes Net Total Return.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Alex Clare

10/02/2026