Please see the market update below received this morning from Brooks Macdonald.

What has happened

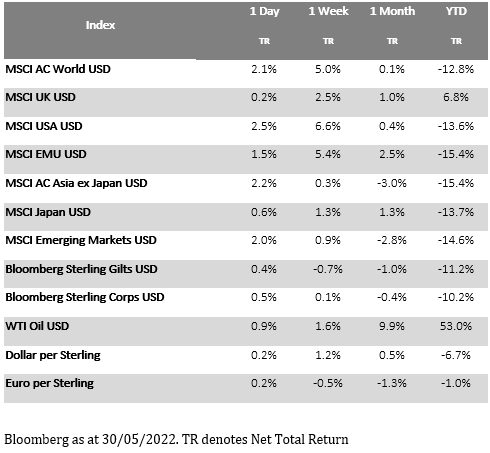

US equity markets broke their 7-week losing streak last week, seeing a strong rally which was led by consumer discretionary stocks as discount retailers posted better earnings than expected. Bond markets also shared this rally as investors priced in a less aggressive pace of tightening from the Federal Reserve in the face of declining economic momentum. This week is likely to be quieter with the US on holiday today for Memorial Day and the UK off on Thursday and Friday for the Queen’s Platinum Jubilee.

Economic data

Despite the week being truncated on both sides of the Atlantic, there are plenty of data releases for markets to interpret. In the US we will see the latest industrial activity metrics as well as the ISM manufacturing data which comes after the misses in the PMI surveys last week. The Conference Board will also update their consumer confidence survey which will give an insight not only into current consumer confidence but also expectations around the future. The main event however will be the US jobs report which is released on Friday. Last month’s reading came in ahead of market expectations at 428,000 new jobs created, this month the market is predicting a more subdued 320,000 but the unemployment rate is expected to tick down from 3.6% to 3.5%.

Central banks

Wednesday will see the beginning of the Federal Reserve’s balance sheet run off as it commences its quantitative tightening programme. The process ramps up in September with the Fed re-investing an even smaller proportion of maturing Treasury and mortgage securities. The Fed’s logic is that by not re-investing a proportion of maturing funds from current holdings, the shrinking of the balance sheet can be open and transparent to market participants, reducing the risk of bond market turmoil. There is undoubtedly a communication and liquidity challenge posed by the combination of rate hikes and balance sheet run-off however and that will keep risk assets on their toes until the process is bedded in.

What does Brooks Macdonald think

Equities have edged higher on Monday, buoyed by a fresh round of stimulus in China and the more optimistic tone that ended the US session last week. This week is likely to contain a focus on the ECB with the central bank increasingly positioning for a July rate hike. Expect the market to focus on German inflation data as well as the specific wording adopted by ECB speakers.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please keep safe and healthy.

Carl Mitchell – Dip PFS

Independent Financial Adviser

30/05/2022