Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 12/05/2026.

What’s driving market optimism?

We explore what’s driving market sentiment as U.S. stocks soar to record highs despite continued Middle East tensions.

Key highlights

- Potential U.S.-Iran deal rallies equities: Equities saw a boost as the U.S. initiated discussions towards a potential deal to reopen the Strait of Hormuz.

- UK political changes are afoot: UK elections saw a substantial swing from the Labour Party to Reform – could this lead to the departure of the prime minister and chancellor?

- The U.S. jobs market holds up: Job openings have plateaued and a significant number of people are still quitting their jobs – despite this, job cuts increased in April.

Potential U.S.-Iran deal rallies equities

The Iran-U.S. war dominated proceedings once again last week. It began with the fallout from a U.S. operation to force the Strait of Hormuz open by facilitating the transport of tankers with naval escorts. The convoys came under fire and investors were concerned that this would trigger a collapse of the ceasefire, providing a downbeat start to the week.

The operation was halted after a day. By mid-week, President Donald Trump used it as the basis for a reattempt at negotiation. Secretary of State Marco Rubio stated in exceptionally direct terms that “the combat phase is over” – language that was unusually conciliatory.

The Trump administration confirmed it had sent a proposal for the reopening of the Strait of Hormuz to Iran. This triggered a substantial rally even though Iran was initially cool towards the proposed terms, particularly any moratorium on uranium enrichment.

The possibility of a deal saw equities – particularly European equities – rally, with government bond yields falling sharply. But at the beginning of this week, negotiations have only highlighted how far apart each party is.

The broader picture remains one of an energy shock, with compounding implications for Europe, such as:

- Elevated gas prices (materially above U.S. levels)

- Fiscal constraints, with debt-to-GDP ratios converging on, or exceeding, 100% in several countries

- The additional burden of increased defence spending

These challenges are connected rather than isolated.

So, when the U.S. and Iran re-engaged in ballistic operations following assaults on U.S. ships, and even as the U.S. awaits a response on its offer, equities have retreated, cyclical sectors have underperformed, and the more defensive corners of the market – including technology – have held up relatively better.

We believe both sides would like to see the Strait reopened, so while there have been several false dawns, eventually one of these potential agreements is likely to take hold

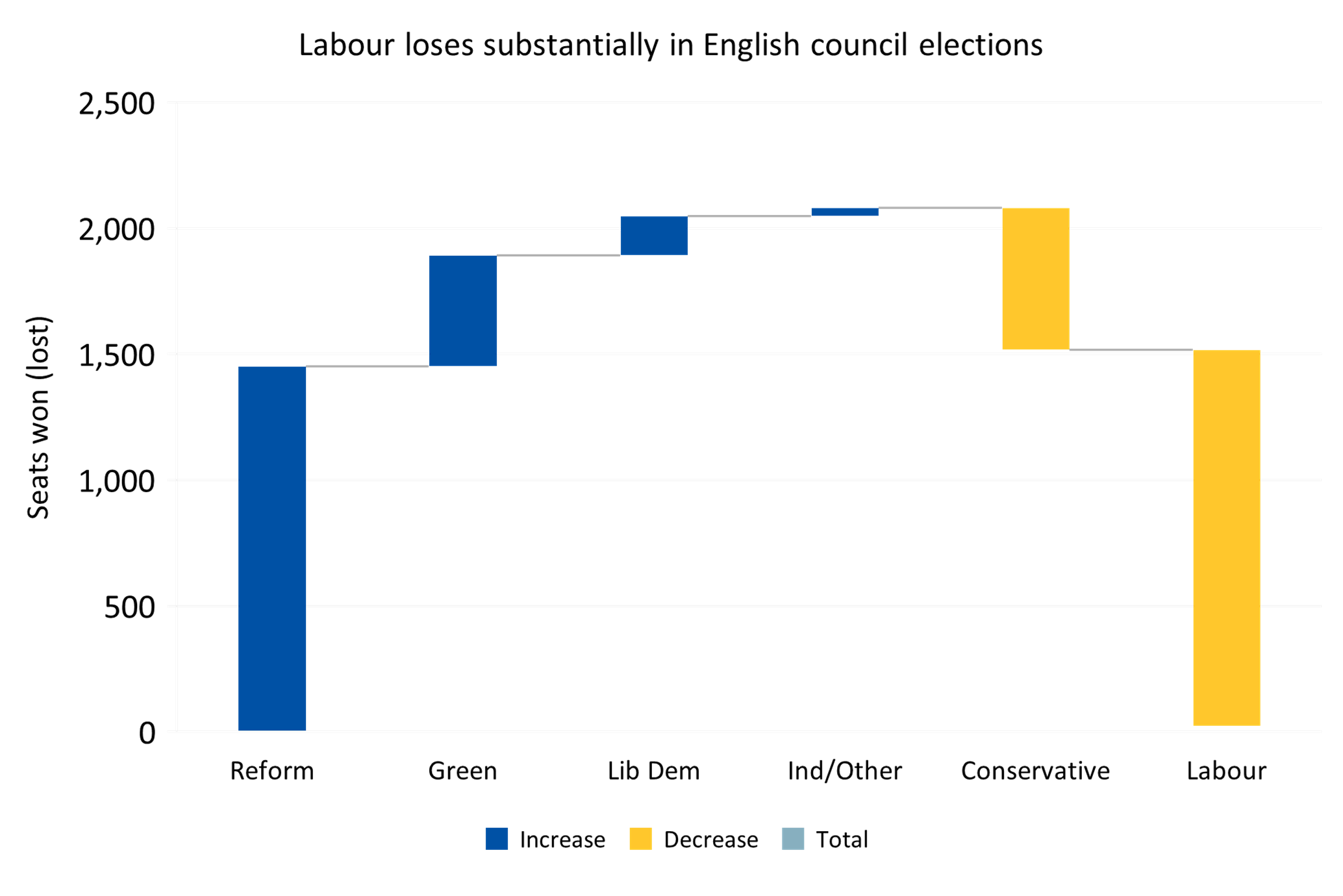

UK political changes are afoot

Last week also saw the UK hold local elections.

The results showed a remarkable swing from the Labour Party towards Reform. To a substantially smaller extent, the Conservatives and independent councillors lost out to the Liberal Democrats and Green candidates.

Source: Associated Press

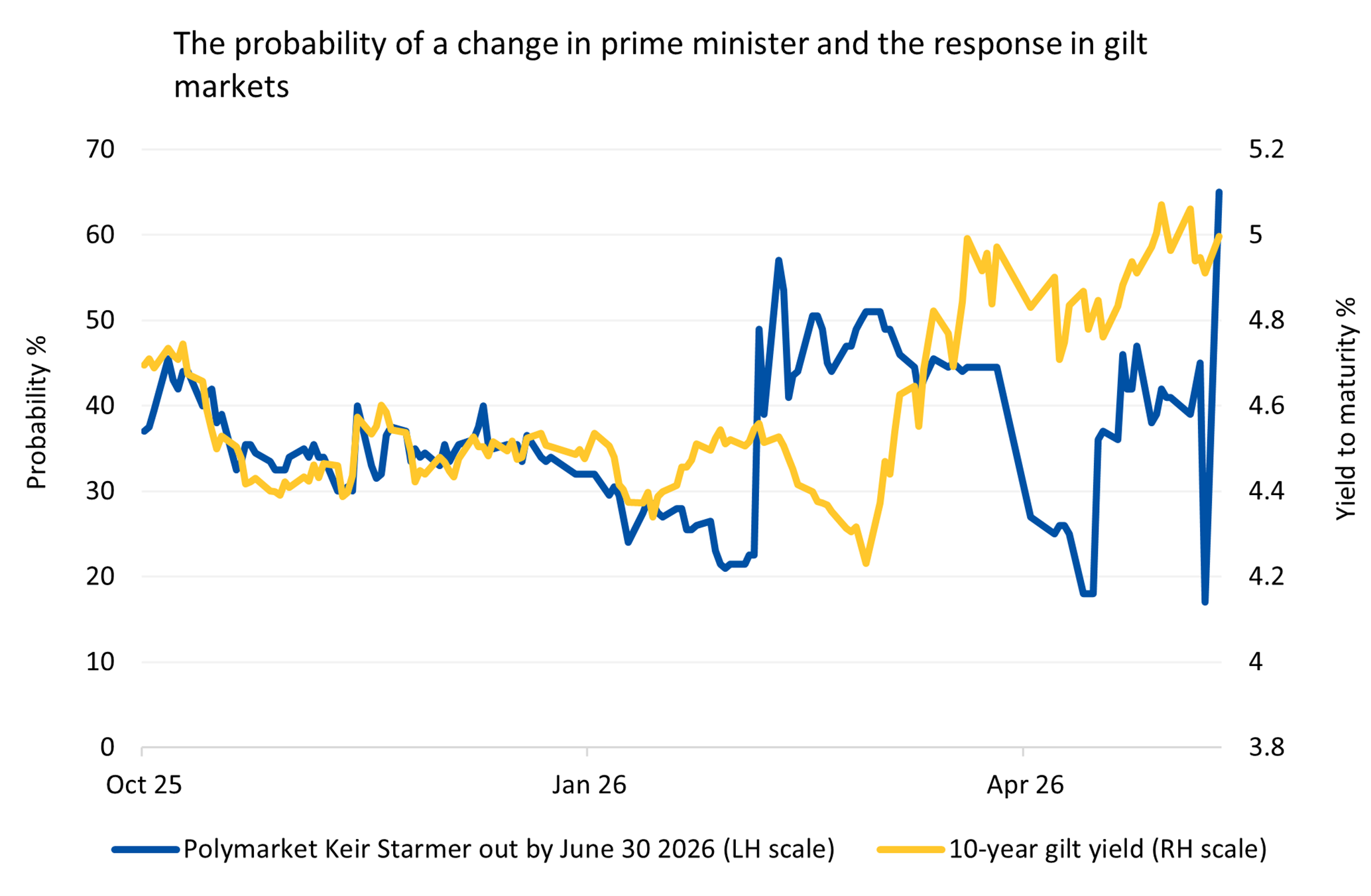

The results were not hugely surprising and there was little reaction in the bond market. However, there is now a concern that these poor results could bring about a leadership challenge resulting in the fall of Prime Minister Sir Keir Starmer and, more specifically, Chancellor Rachel Reeves.

Potential candidates could be more inclined to increase spending, leading to more bond issuance and possibly higher inflation.

Prediction markets place approximately a 45% probability on the prime minister departing by the end of June, and a 60% to 70% probability of him departing by year-end – a number that fell when he vowed not to resign, but rose once more as signs of rebellion from the party, and even within the cabinet, started to grow.

The gilt market has been concerned about the impact of a new prime minister as they may feel compelled to jeopardise fiscal sustainability to meet their political objectives. It seems likely that any future leader will be aware of how important it is to respect the bond market – however, they’ll also need to cope with external factors (such as the U.S.-Iran war), which put additional pressure on the government finances.

In recent weeks it’s been made clear that the Persian Gulf war has been the most significant bond market concern.

Source: Bloomberg

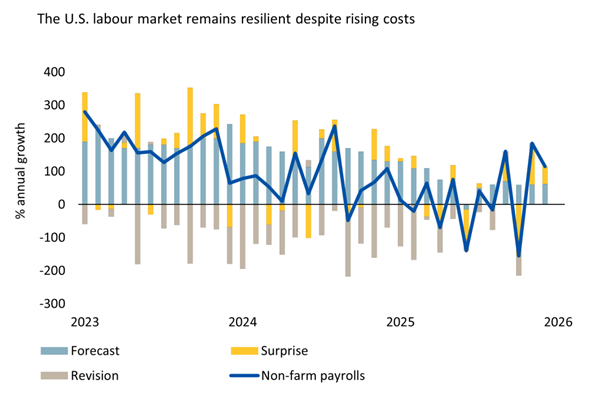

The U.S. jobs market holds up

In the U.S., frustration continues to grow with the economy.

Polling suggests that attitudes towards the war are fairly static, but attitudes towards the inflation it has created are becoming increasingly uniform.

Earnings reports cited the increasing pressure on the lower income cohorts, but so far, the jobs market is holding up. Job openings have plateaued, and there are still a significant number of people quitting their roles (implying they’ve found better employment elsewhere).

The latest jobless claims data remains subdued. Last month, 100,000+ new jobs were created in the U.S. Jobs growth has been slowing in recent years, but recent months have seen it stronger than anticipated.

Source: LSEG Datastream

The only concern is the increase in the number of job cuts in April, which the monthly Challenger Jobs Report attributed to AI. Jobs growth can slow due to cyclical factors, such as interest rate or gasoline price increases. But it can also slow due to structural factors, such as the roll-out of labour-replacing technology-driven investment.

So far, this is the second consecutive month we’ve seen AI mentioned as the reason for U.S. jobs cuts. It has been cited as the reason for 49,135 job cuts – about 16% of all job cuts this year. The numbers are very modest, but the trend is one that will be scrutinised.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Charlotte Clarke

13/05/2026