Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 06/05/2026

What’s driving market resilience?

We explore what’s driving continued market resilience as the war between the U.S. and Iran continues.

Key highlights

- New peace proposal? The U.S. began escorting vessels through the Strait of Hormuz over the weekend, leading to news of a potential peace plan with Iran.

- Interest rates held: Major central banks held interest rates, though they’re expected to start rising in June.

- Mixed stock market results: European indices fell around 1% on Thursday while the U.S. bucked the trend – driven by generally good earnings numbers last Wednesday.

Strait talking

Last week saw the Iran-U.S. war enter its ninth week, and what had been cautious market optimism around a negotiated resolution gave way to a more sober assessment.

Early last week, reports emerged via Axios that Iran had submitted a proposal to reopen the Strait of Hormuz. This would reportedly involve the U.S. lifting its naval blockade, agreeing to a new legal framework for the Strait and deferring nuclear negotiations to a later date.

The U.S. indicated the offer was insufficient, and by mid-week, reports suggested President Donald Trump was being briefed on new military operations and had told aides to prepare for an extended blockade.

Over the weekend, the U.S. began escorting vessels through the Strait, coming under fire in the process. The escort plan was dropped after just one day, but has been followed by news of a potential peace plan between the U.S. and Iran. The deal is expected to revolve around a moratorium on uranium enrichment by Iran, sanctions relief by the U.S., and both sides lifting restrictions on transit through the Strait of Hormuz.

These developments were reflected in the oil market. Futures prices are still sloping downward, suggesting that prices are high now but will fall in the future. Spot prices (the cost of buying an actual barrel of physical oil) fell on the latest news but remain elevated, above even the short-term futures prices.

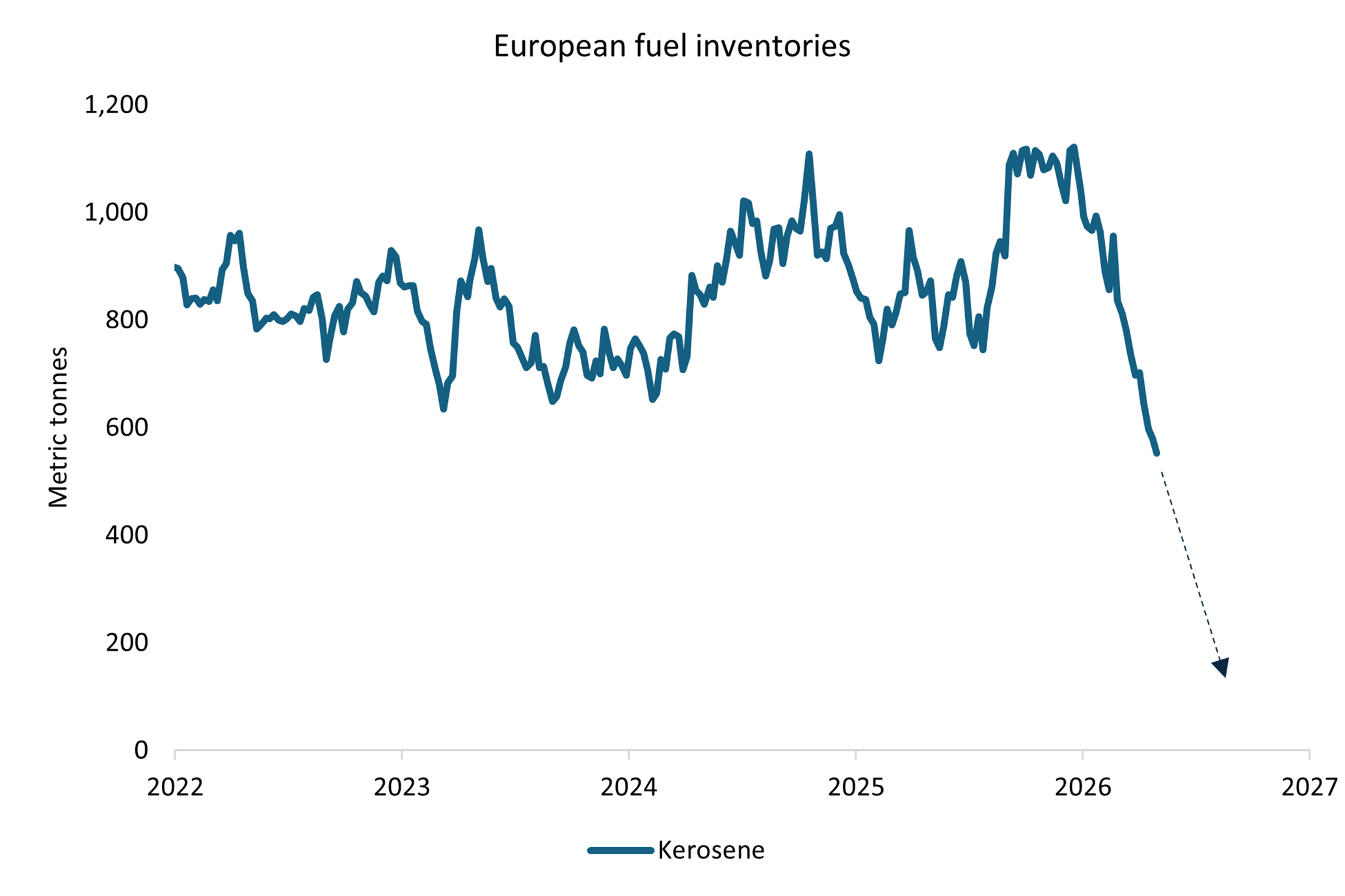

As supplies of crude have been slow to arrive at the refineries, companies have drawn down on inventories of oil products, which have been declining. For example, kerosene inventories in Europe have dropped sharply, leading airlines to cancel flights.

There’s growing optimism that these inventories will begin to be replenished through an eventual return of Gulf supplies. If not, the European market will end up buying kerosene and other oil products from other regions, allowing oil to flow through the markets that are prepared to pay the highest price. For example, a supply decline of 10% would necessitate a 10% reduction in energy consumption, but this may not happen in the regions with the lowest inventories. Therefore, the most obvious implication is the inflationary impact. This was something for policymakers to ponder last week, when all the major central banks were reporting.

Source: Bloomberg

Central banks: Hawkish drift and no action

As anticipated, none of the central banks changed their policies last week.

The Federal Reserve (the Fed) held rates at its final meeting under current Chair Jerome Powell. He will almost certainly be replaced as chair by Kevin Warsh, who’s in the process of being confirmed by the Senate.

RBC Wealth Management (U.S.)’s Tom Garretson, a senior portfolio strategist specialising in fixed income, points out that there hasn’t been much pushback on Warsh. Blanket statements that he’s an ‘impressive’ and ‘outstanding’ candidate who used to be at the Fed have been nearly universal.

Tom questions that appraisal: “The highlight of his entire CV is basically his time at the Fed during the Global Financial Crisis, but his only notable accomplishments were seeking to raise rates when unemployment was still around 8%, and then warning about the potential hyperinflationary impact of quantitative easing, which he ultimately resigned from the Fed over, and which ultimately never occurred.”

Kevin Warsh is President Trump’s selection because the president was frustrated that Jay Powell’s Fed wasn’t cutting rates fast enough. But now that Warsh is about to arrive, he’ll find it hard to persuade the Fed to cut given that inflation is on an upward trajectory due to the Iran-U.S. war.

It wouldn’t be surprising if his relationship with President Trump were to become a tense one from the start.

Elsewhere, the European Central Bank, Bank of Japan (BoJ) and Bank of England (BoE) all held interest rates. However, these are expected to start rising in June.

The key development was a hawkish shift in market pricing. At the start of last week, UK and Eurozone markets were discounting approximately two rate hikes by year-end. By Friday, this had edged towards the possibility of three – reflecting the inflationary impulse from elevated energy prices.

The Bank of England’s Monetary Policy Report laid out three scenarios:

A – energy prices follow the futures curve lower, with no second-round effects – still justifying roughly two rate hikes.

B – prices remain elevated between current levels and the curve, with moderate wage effects.

C – prices rise further with significant second-round effects, implying rates will rise by over one percentage point to 5.25–5.50%.

Even the benign scenario now appears to justify further tightening. This contrasts with comments made by BoE Governor Andrew Bailey over the past month – for example, when he described how the market’s “still pricing us to raise rates… I think they’re getting ahead of themselves.”

Additional anxiety over the direction of interest rates and oil prices was a headwind to markets but the earnings season was a tailwind.

Equity markets adopted a risk-off tone as last week progressed, with European indices falling around 1% on Thursday. U.S. equities bucked that broader move, driven by generally good earnings numbers on Wednesday, when the four hyperscalers of the ‘Magnificent Seven’ mega cap stocks (Microsoft, Meta, Amazon and Alphabet) reported their Q1 earnings.

The results were mixed, with Alphabet’s impressive results seeming to validate the full stack vertically-integrated model (infrastructure, language model, tools and applications). Meta, on the other hand, disappointed due to the costs of investment.

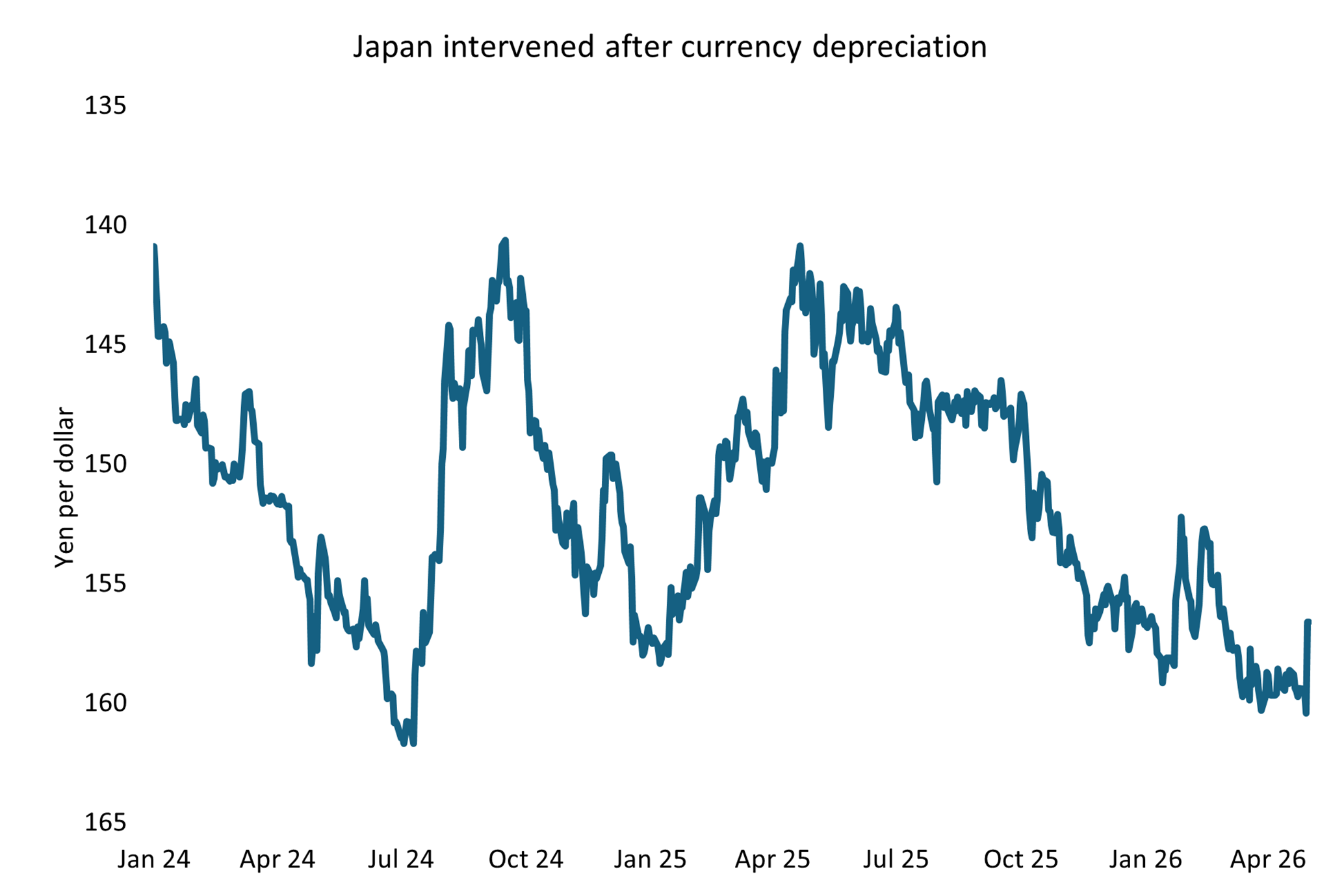

The dollar strengthened gradually, and Japanese government bonds sold off across the curve, with the yen breaching the 160-per-dollar level before an intervention by the BoJ to stabilise it.

Energy importers like Japan have suffered downward pressure on their currencies from the rise in energy costs and resulting higher import costs. Others include Turkey and India, which have also used reserves to attempt to stabilise their currencies. At the same time, Gulf states that would normally accumulate reserves, especially at times of high energy prices, haven’t done so while their cargoes can’t reach the market.

Source: Bloomberg

Taken together, these two groups have reduced the pace of reserve accumulation and, therefore, the structural demand for gold. This creates short-term pressure on the gold price, which will continue until reserve accumulation can return to normal.

Thereafter, the case for holding gold seems as strong as ever. The U.S. runs a large and persistent current account deficit and a deeply negative net international investment position, consuming more than it produces and financing the difference by accepting dollar-denominated loans from the rest of the world.

It’s understandable why other countries would balk at holding the majority of their foreign exchange reserves in dollars, and gold benefits as result.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Charlotte Clarke

07/05/2026