Please see the below article from Brooks Macdonald detailing their discussions on the US-Iran war and the ripple effect on markets. Received this morning 28/04/2026.

What has happened?

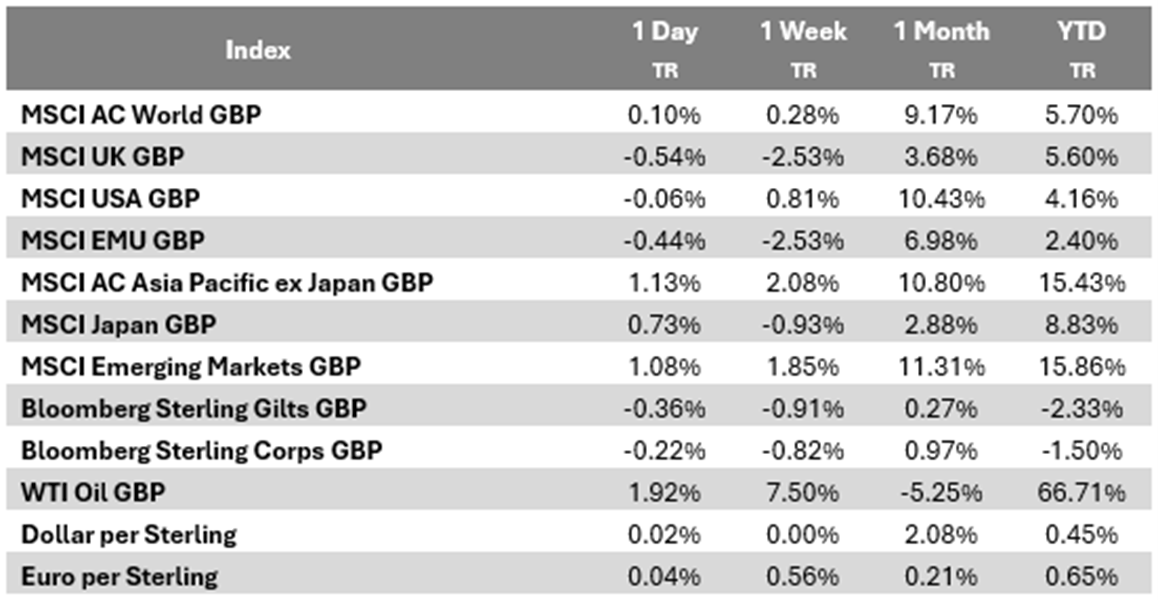

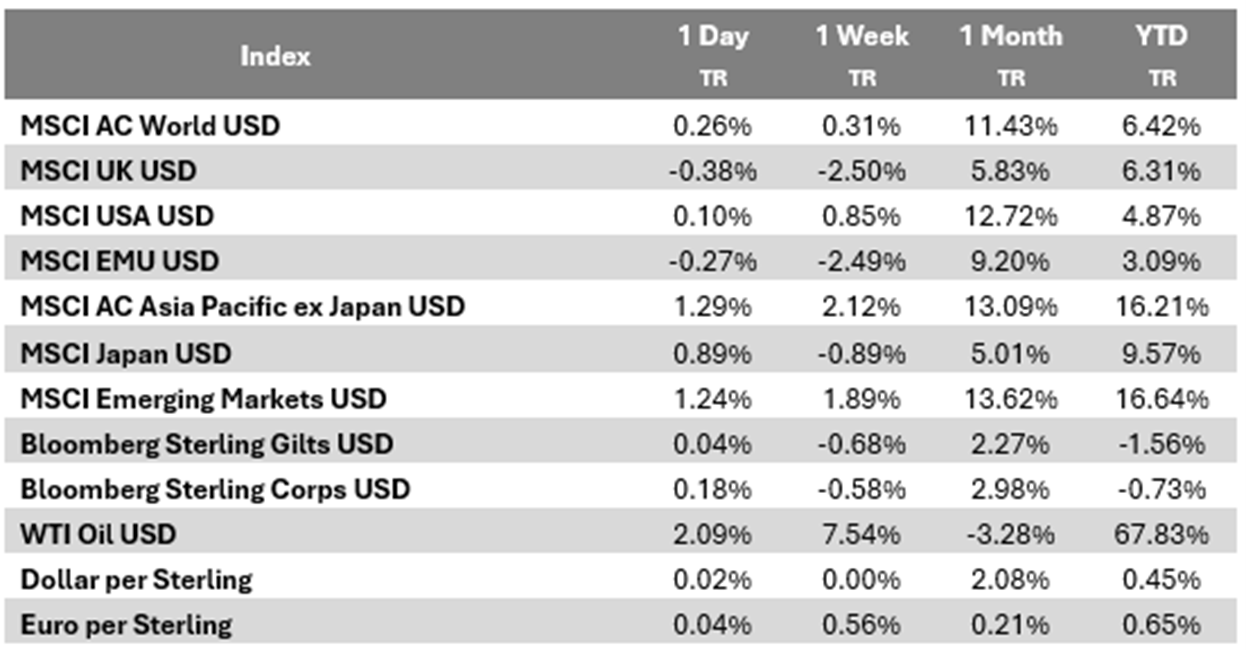

Two months into the Iran conflict, markets are in an uneasy stalemate. Brent crude touched $109/bbl overnight, a three-week high, after the White House signalled scepticism toward Iran’s proposal to reopen the Strait while deferring nuclear talks. Despite the backdrop, the S&P 500 and Nasdaq edged to fresh record highs, led by Nvidia.

The inflation clock is ticking

With Brent above $100/bbl for nearly a week, inflation is firmly back on the agenda. Equity markets are holding up on earnings and AI momentum, but fixed income is signalling that the longer the Strait stays closed, the harder it becomes for central banks to ease. Treasuries sold off with the 10-year yield rising to 4.34%, Gilts underperformed with the 30-year yield at a 7-month high, and the Bank of Japan held rates in a notably split 6-3 vote, raising inflation forecasts while cutting growth projections.

What does Brooks Macdonald think?

What began as an acute shock is increasingly being priced as a structural shift, oil markets are pricing extended disruption, inflation expectations are drifting higher, and the easing window is narrowing. US equity resilience is impressive but increasingly narrow, resting heavily on Mag-7 momentum which is facing its biggest test this week as Microsoft, Amazon, Meta and Alphabet all report. Disappointment on AI capex or forward guidance could remove one of the few remaining pillars supporting sentiment.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Alex Clare

28/04/2026