Please see below this week’s Markets in a Minute update from Brewin Dolphin – received late yesterday afternoon – 10/08/2021

Stocks rise on encouraging labour market data

Global stock markets rose last week on the back of promising US labour market data and strong corporate earnings reports.

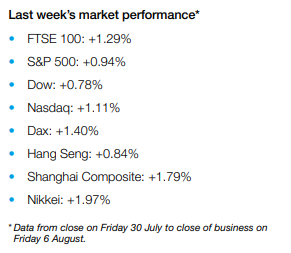

After a shaky start, US indices finished the week at new record highs following a better-than-expected July jobs report. The S&P 500 rose 0.9%, with an increase in longer-term interest rates boosting financial shares. The Dow added 0.8% while the technology-heavy Nasdaq climbed 1.1%.

The upbeat mood fed through to Europe, where the STOXX 600 surged 1.8% and Germany’s Dax added 1.4%. The UK’s FTSE 100 gained 1.3% after the Bank of England increased its 2022 gross domestic product (GDP) growth forecast from 5.75% to 6.0%.

Strong earnings reports boosted Japan’s Nikkei 225, which rose almost 2.0% despite the International Monetary Fund downgrading its 2021 GDP growth forecast for Japan from 3.3% to 2.8% amid the country’s tighter coronavirus restrictions.

China’s Shanghai Composite bounced back from last week’s rout to end the week up 1.8%.

Equities mixed as oil prices tumble

Equities were mixed on Monday as oil prices slid amid concerns that rising Covid-19 cases could result in a slowdown in demand for fuel.

The FTSE 100 edged up 0.1% whereas Germany’s Dax slipped 0.1% after data showed that while German exports rose by 1.3% in June from the previous month, imports fell by 0.6%. Miners underperformed after figures showed China’s export growth unexpectedly slowed in July, which weighed on commodity prices.

In the US, the Dow and the S&P 500 slipped 0.3% and 0.1%, respectively, as last week’s strong payrolls figures led to further speculation about when the Federal Reserve might begin tapering its support for the economy. The lacklustre performance on Wall Street resulted in a muted start for the FTSE 100 at Tuesday’s market open, with the blue-chip index flat at 7,133.8.

US payrolls report beats forecasts

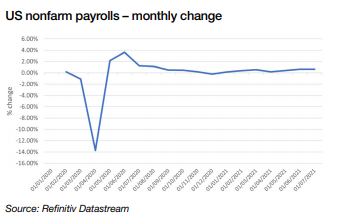

Last week’s economic headlines focused on the latest US jobs report, which revealed nonfarm payrolls increased by 943,000 in July from the previous month, better than the 845,000 new jobs expected by economists in a Dow Jones poll. The leisure and hospitality sector led job creation, adding 380,000 positions in July.

The figures from the Labor Department also showed the rate of unemployment declined from 5.9% in June to 5.4% in July. Economists surveyed by Dow Jones had forecast an unemployment rate of 5.7%. The unemployment rate has tumbled from a pandemic high of 14.8% but remains well above the 3.5% rate seen before the crisis hit.

The employment report led to a rise in longer-term Treasury yields, which had already been boosted earlier in the week by hawkish comments from Federal Reserve vice chair Richard Clarida, who suggested interest rate hikes could start in 2023.

US manufacturing growth cools

On a less positive note, data from the Institute for Supply Management (ISM) showed US manufacturing activity grew at a slower pace in July, thanks to a continuing shortage of raw materials. The index of national factory activity fell to 59.5, the lowest reading since January and down from 60.6 in June. Economists polled by Reuters had forecast the index would be little changed at 60.9.

Meanwhile, the measure of prices paid by manufacturers fell to 85.7 from a record 92.1 in June as commodity prices eased. This was the largest fall since March 2020.

BoE lifts GDP and inflation forecasts

Here in the UK, the Bank of England lifted its 2022 GDP growth forecast to 6.0% from 5.75%. The Bank said GDP is expected to grow by 3.0% in the third quarter of this year, which is weaker than its May forecast because of the recent surge in Covid-19 cases and the number of workers isolating.

The Bank also increased its inflation forecasts following two consecutive months of higher-than-expected readings. It now expects inflation to temporarily reach 4.0% in the fourth quarter of 2021 and the first quarter of 2022 because of higher energy and goods prices. These increases are expected to moderate in the medium term “as commodity prices stabilise, supply shortages ease and global demand rebalances”, the Bank said.

The base interest rate is anticipated to reach 0.5% in the third quarter of 2024, after hitting 0.2% in the third quarter of 2022 and 0.4% in the same period in 2023. Members of the monetary policy committee agreed to start tapering their support for the economy once the base rate has risen to 0.5%.

Japan’s service sector shrinks further

Over in Japan, a key measure of services sector activity contracted for the 18th consecutive month in July as the country introduced further restrictions to try to combat the resurgence in Covid-19 infections. The final au Jibun Bank Japan services PMI fell to a seasonally adjusted 47.4 in July from 48.0 the previous month. A reading below 50.0 signals contraction.

Household spending in Japan also fell in June by 5.1% from the previous year as the state of emergency reduced domestic demand and cuts to summer bonuses hit consumption. Economists had expected spending to rise by 0.1% from a year ago.

Please continue to check back for our latest blog posts and updates.

Charlotte Ennis

11/08/2021