Please see below the latest ‘Markets in a Minute’ article from Brewin Dolphin received late yesterday afternoon – 02/03/2021

Equities slide as rise in bond yields sparks tech sell-off

Global equities fell sharply last week after a steep rise in long-term government bond yields led to the worst technology sell-off in four months.

In the US, the S&P 500 recorded its biggest weekly drop in a month, falling 2.5%. The Nasdaq Composite suffered its worst decline since October, down 4.9%, as investors continued to rotate out of highly valued growth stocks into value and cyclical stocks. A rise in oil prices saw energy shares outperform, whereas consumer discretionary stocks were weak.

Stock markets in Europe also fell, with the pan-European STOXX 600 ending the week down 2.4%. The FTSE 100 dropped 2.1% as the pound rose to its highest level in almost three years, fuelled by the rapid roll out of the Covid-19 vaccine and hopes of economic recovery.

The global sell-off fed through to Asia, where the Nikkei fell 3.5% and the Shanghai Composite tumbled 5%. China’s large-cap CSI 200 recorded its worst weekly performance since October 2018, falling 7.7% as profit-taking hit companies in sectors such as semiconductors and electric vehicles.

Last week’s market performance*

• FTSE 100: -2.12%

• S&P 500: -2.45%

• Dow: -1.78%

• Nasdaq: -4.92%

• Dax: -1.48%

• Hang Seng: -5.43%

• Shanghai Composite: -5.06%

• Nikkei: -3.50%

*Data from close on Friday 19 February to close of business on Friday 26 February.

Budget leaks boost FTSE 100

The FTSE 100 rebounded on Monday, gaining 1.6% following a series of leaks about Wednesday’s budget. Housebuilders rallied on news that the government will launch a mortgage guarantee scheme to help buyers, with small deposits, onto the property ladder.

In the US, the S&P 500 gained 2.4% in its best session since June 2020. The Nasdaq surged 3% after vaccine optimism boosted risk assets and Treasury yields retreated. The Bank of England echoed sentiments from the Federal Reserve about accommodative monetary policy.

The rebound began to falter on Tuesday, with the Hang Seng and CSI 300 both declining by around 1% overnight. A top Chinese banking regulator said he was ‘very worried’ about bubbles in overseas financial markets and in China’s property sector. The FTSE 100 opened flat, with energy and mining stocks among the worst performers amid fears of slowing demand for commodities in China. Taylor Wimpey was the biggest gainer, adding 3.4% after it revealed the 2021 selling season had started positively.

Economic data stronger than anticipated

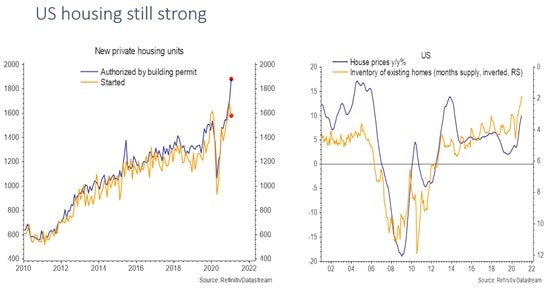

The yield on the ten-year US Treasury note increased to its highest level in over a year last week, as stronger-than-expected economic data fuelled fears about rising inflation. In the US, data revealed continued robustness in the housing market, with building permits hitting a new high and house prices continuing to surge.

Sales on new single-family homes increased by 4.3% in January to a seasonally adjusted annual rate of 923,000 units. Sales were helped by historically low mortgage rates and a shortage of previously owned houses on the market. The median new house price rose by 5.3% from a year earlier to $346,400.

The housing data added to solid PMIs published the week before, which showed a 1.3% increase in the prices that businesses receive for their goods and services – the biggest gain since the index was launched in 2009. Weekly jobless claims also hit their lowest level in three months at 730,000, while personal incomes increased by 10.1% in January following payments from the coronavirus relief package.

On Wednesday, Fed chair Jerome Powell sought to allay investors’ fears that stronger economic growth will result in monetary stimulus being removed sooner than expected. Powell said inflation remains soft and confirmed the Fed’s dovish stance. Stocks briefly recovered on Wednesday, but began their descent again the following day, suggesting Powell’s comments have done little to quell investors’ concerns.

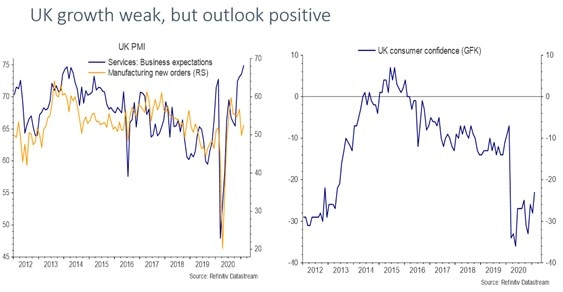

UK consumer confidence creeps higher

There is also optimism in some of the UK’s economic data. Manufacturing new orders remain in expansion territory, and the expectations component of the services PMI hit the highest level in over a decade. UK consumer confidence is also starting to creep higher.

Lockdown restrictions will start to ease in England from 8 March, with nearly all sections of the economy due to be reopened in late May. In Wednesday’s budget, Rishi Sunak is expected to announce that the furlough scheme will be extended until at least May. Around 20 million people in the UK have now received their first dose of the vaccine.

The vaccine rollout continues to lag in Europe, with just 6.4% of the European Union’s population receiving a jab. Despite this, the eurozone Economic Sentiment Indicator increased to 93.4 in February from 91.5 the month before – the highest level since March 2020. Fourth-quarter German GDP data was revised to a growth rate of 0.3% from an initial estimate of 0.1%, following strong exports and construction activity.

Over in Japan, the Reuters monthly Tankan Index, which tracks the Bank of Japan’s quarterly Tankan survey, recorded a positive reading among manufacturers for the first time since 2019, thanks to improving demand from overseas. Japan is also seeing a decline in the Covid-19 infection rate, which will see the state of emergency status being lifted for six prefectures a week earlier than planned.

Weekly updates like these from Brewin Dolphin help us keep up to date with what is happening within the markets. This week’s ‘Markets in a Minute’ article focuses on exploring some of the reasons behind the tech sell-off.

Please continue to check back for our regular blog posts and updates

Charlotte Ennis

03/03/2021