Please see this weeks ‘Weekly Market Performance Update’ from Invesco:

Momentum on the vaccine front continued last week with a stream of positive news flow from the three companies (Pfizer, Moderna and Astra) making up the first wave of the DM vaccination development programme. This is clearly supportive of an improving medium-term growth outlook. However, the near-term backdrop looks increasingly downbeat. With negative Q4 growth already forecast for the EZ and UK, the risks to the downside in the US are also increasing, as regional lockdown restrictions rise and close to 10 million US workers are expected to lose their unemployment benefits at the start of next year. With the two largest DM economies struggling, the risk of contagion into the rest of the global economy, where virus news flow remains mixed (Japan and Korea, for example, are seeing a third wave of new cases), has undoubtedly increased. And there continues to be an important risk imbalance here. The near-term headwinds are far more concrete and fast-approaching, while the medium-term supports are still conjectural and vulnerable to being watered down as the year progresses. This two-way pull between near-term risks and medium-term opportunity continues to dominate financial market sentiment, even while political uncertainty continues to fester in the background on a number of fronts (US election, Brexit, EU budget impasse).

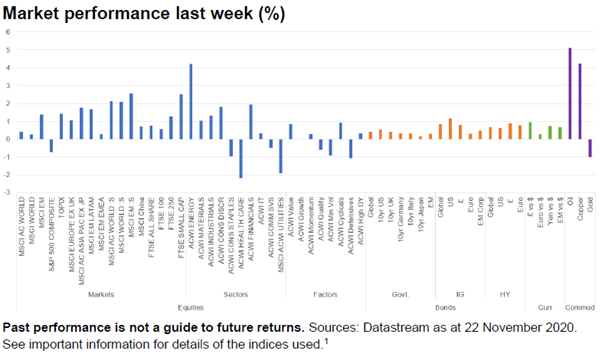

Vaccine just about held sway over virus in equity markets last week with the rotation trends of the previous week carrying through, albeit with far less momentum. Global equities hit a new high during the week (MSCI ACWI 0.4%), led by EM. Within DM, more cyclically exposed markets, such as Europe and Japan, led performance, with the US again lagging and ending down on the week. Small Caps outperformed and hit a new high, but still remain behind large caps YTD. Divergence in sector and factor performance continued. Energy and Financials retained their place at the top of the leader board, the former helped by further strengthening in the oil price. Defensives were the main laggards, with all four “defensive” sectors (Staples, HealthCare, Comms Services and Utilities) down for the week. The continuing rotation underpinned Value’s further outperformance relative to Growth. The UK (All Share +0.8%) benefitted from its Energy and Financials exposure, but that was partially offset by high exposure to defensive sectors, such as Staples and HealthCare. Small Caps continue to lead the market higher and they are now back in positive territory for the year, having been down 39% at one point in March.

Fixed Interest returns were positive across the asset class. Government bonds pushed lower with the 10yr Italian BTP hitting another record low of 0.6%. Spreads continue to narrow versus Bunds. IG edged ahead of HY in credit markets, with strength led by the US in the former and Europe in the latter. Yields hit record lows in both (1.51% and 5.31% respectively). Spreads narrowed marginally too.

The US$ resumed its weakness, falling against both DM and EM currencies. Combined with positive vaccine and supply news, this underpinned commodity markets, with both Oil and Copper rising, the latter to a new YTD high. Copper is now on course for an eighth straight monthly gain, the longest winning run in nearly a decade. A more positive economic backdrop is not necessarily helpful for Gold, which fell for the second week as ETF holders continued to reduce positions.

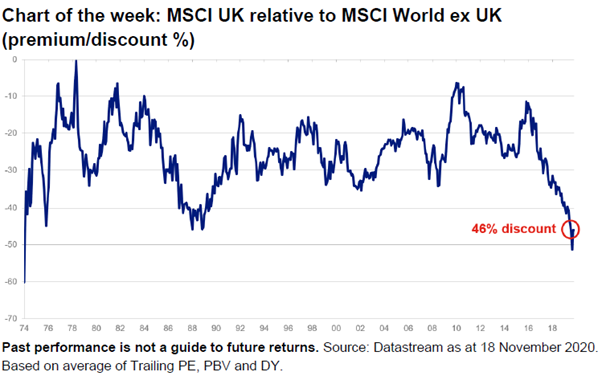

- According to the latest BofA Securities monthly Global Fund Manager Survey, the UK is by far and away the least loved major equity market, with a net 33% of respondents saying they are underweight. This dislike is hardly new. Only in a small period in 2013 since the GFC have investors been overweight. This has been a good call. While local currency TR have been decent for the MSCI UK over this period (120%), they have been dwarfed by returns from other DMs. MSCI World ex UK is up 329%. Even if you strip out the very strong US market, it has lagged. MSCI World ex US is up 165%. And with £ having weakened over this period, £ denominated relative returns have been even worse. Brexit risk, an unattractive sector mix (no tech), earnings underperformance and, more recently, the poor handling of the pandemic have all made it easy for investors to take their money elsewhere.

- So where does this leave UK relative valuations? The chart shows the long-term premium/discount for the MSCI UK (it has a much longer valuation history than the FTSE indices) relative to the MSCI World ex UK based on a composite average of Trailing PE, DY and PBV. Interestingly it has never traded at a premium. But the size of the current discount is material. At 46% it has only ever been surpassed in late 1974 and earlier this year. As you can see there has been a substantial de-rating in recent years from a 12% discount at the end of 2016, a function of the de-rating of the UK and a re-rating of the World ex UK during that period. The re-rating of tech and tech-related stocks, where the UK has little exposure, has largely driven the latter, while a de-rating of overweight sectors, such as Consumer Staples (Tobacco in particular), Financials and commodities, has been behind the former.

- Has a large discount historically led to subsequent relative outperformance from the UK? Over the long term the relationship between the starting relative valuation and subsequent relative performance over both 5- and 10-year periods has been weak, with an R Squared of just 26% and 4% respectively. However, if you look at periods when the discount has been over 35% the UK has historically always outperformed over both time periods. Of course history is not necessarily a good guide to future returns and valuations on their own are rarely enough to drive a sustained period of outperformance. But it is a good starting point to be revisiting the UK market even if the fundamental backdrop for many of its leading companies remains a challenging one. And of course its relative performance fate may be out of its hands if tech (and tech-related stocks), where it has limited exposure (MSCI UK IT 1.4%, MSCI World ex UK IT 22.5%), were to continue to dominate the performance rankings.

Key economic data in the week ahead

- It’s a relatively quiet week on the data front, with Preliminary PMIs the main area of interest, providing timely insight into the varying impact of virus containment measures on a number of major DM economies. With Brexit negotiations on tenterhooks (and now in a virtual format just to add complications) and the deadline for concluding them fast approaching, every smoke signal from the two negotiating teams will be even more closely watched. Financials markets expect a deal, even if it is likely to be of the “skinny” variety.

- In a Thanksgiving shortened week in the US on Monday we have Preliminary PMI data, with both the Manufacturing and Services components expected to decline around a point to 52.5 and 55.8 respectively, still close to their post-recession highs. Declining confidence will also likely be reflected in a decline in the Conference Board Consumer Confidence Index on Tuesday to 98. This measure has yet to show any meaningful recovery off its Q2 lows. Initial Jobless Claims on Wednesday are forecast at 733k, up from last week’s 742k, as the US see a significant rise in Coronavirus cases. And on the same day we have the Fed’s preferred inflation measure, the Core PCE Deflator, which is expected to be unchanged month-on-month and down slightly to 1.4%yoy.

- A very quiet week in the UK, with Monday’s PMI data the only announcement of note. Unsurprisingly, given the ongoing virus containment measures, a sharp decline in sentiment is expected, with Manufacturing falling from 53.7 to 50.5, the more lockdown sensitive Services sector falling from 51.4 to 43, leaving the Composite at 43, down from 52.1. On Wednesday there is the Chancellor’s Spending Review, which will just cover department budgets for the next Financial Year, having been downgraded from a multi-year review due to virus-related uncertainty around the public finances. But still plenty of interest for investors, with the OBR publishing its latest economic forecasts at the same time.

- An equally quiet week in the EZ with just the PMIs to focus on. A similar profile to the UK expected here with Services (42.2 from 46.9) taking more of a hit than Manufacturing (53.1 from 54.8), leaving the Composite at 45.5 from October’s 50.

- Nothing of note this week from either Japan or China.

This week starts off with more good news on the vaccine front. It will be interesting to see how this week pans out as Boris announces the governments plans for the end of the nationwide lockdown and the plans for the rest of the winter.

Please keep checking back for further market updates from a range of fund managers and investment houses.

Andrew Lloyd

23/11/2020