Please see below article received from Brooks Macdonald this morning, which reviews yesterday’s Budget in more detail.

Chancellor Rachel Reeves has unveiled the much-anticipated Autumn Budget, outlining the government’s plans to address the nation’s financial challenges. As expected, the budget includes several significant changes. Here, we break down the key announcements and what they may mean for your wealth.

Major budget announcements that may affect your wealth

Capital gains tax reforms

Significant capital gains tax (CGT) reforms have been introduced. The lower rate of CGT will increase from 10% to 18%, and the higher rate from 20% to 24%, while the rate for residential property remains unchanged. The tax treatment of carried interest will increase to 32% from April 2025, up from 28%. The Business Asset Disposal Relief will remain at 10% this year, before rising to 14% in April 2025.

What it means for you: Investors will face higher tax bills on their gains, while business owners will see a phased increase in the CGT rate on the sale of their businesses, losing the benefit of the current reduced rate over the next few years.

Inheritance tax updates

The inheritance tax threshold is frozen until 2030 remaining at £325,000, with an additional residence nil-rate band of £175,000 for those passing on their home to direct descendants. The government is also removing the opportunity for individuals to use pensions as a vehicle for inheritance tax planning by bringing unspent pots into the scope of inheritance tax from April 2027, which will affect around 8% of estates each year.

What it means for you: If you are planning your estate, the unchanged thresholds provide some stability. However, the announcement that inherited pension pots will now be subject to inheritance tax will significantly impact estate planning strategies, especially for those with larger pension pots.

Income tax changes

The government has announced the freeze on income tax thresholds will not be extended beyond the 2028-2029 tax year and from this point, personal tax thresholds will be uprated in line with inflation.

What it means for you: The removal of a freeze will prevent more people from being pushed into higher tax brackets due to wage increases. This has the effect of reducing the tax burden on working individuals and preserving more of their income.

National Insurance rises

As expected there were big changes to employer National Insurance (NI) contributions, the UK’s second largest revenue stream after income tax. Effective immediately, the Employer’s National Insurance rate has increased by 1.2% to 15% raising £25 billion and the threshold at which companies pay the tax has been lowered. Employee and self-employed NI rates remain unchanged.

What it means for you: Employers will face higher NI contributions, while employees and the self employed have escaped any rises. This adjustment is expected to be the biggest revenue generator in the Budget.

Surprises on the day

Outside of the more anticipated moves, there were a few more surprising measures.

Windfall tax on energy companies

The latest budget includes significant changes to the taxation of energy companies. The Energy Profits Levy (EPL), initially introduced in May 2022, has been increased from 25% to 38% and will remain until March 2030.

Green investment incentives

New incentives for green investments have been introduced, including tax breaks for companies investing in renewable energy projects and electric vehicle infrastructure. This also includes a climate action mandate for the Bank of England, support for green technologies, and training programmes for green jobs.

AIM market changes

Under much scrutiny in the run up to the Budget, Reeves announced a 50% relief on Alternative Investment Market (AIM) shares for inheritance tax. This means the effective tax rate on AIM-traded shares is now 20%.

Stamp duty adjustments

The government has introduced new additional stamp duty rates, on top of the stamp duty paid for a first home, for second homes and buy-to-let properties by 2% to 5% from effect 31 October, to cool the housing market and make it easier for first-time buyers to enter the market.

Fuel duty freeze

Despite speculation, the government has decided to freeze fuel duty for another year, providing relief to motorists amid high fuel prices. What it means for you: These changes may impact your investments if you are an investor in the energy sector or investing in the AIM market. Prospective homebuyers may find it easier to purchase their first home due to the new stamp duty rates. Motorists will see no increase in fuel duty, maintaining current fuel prices.

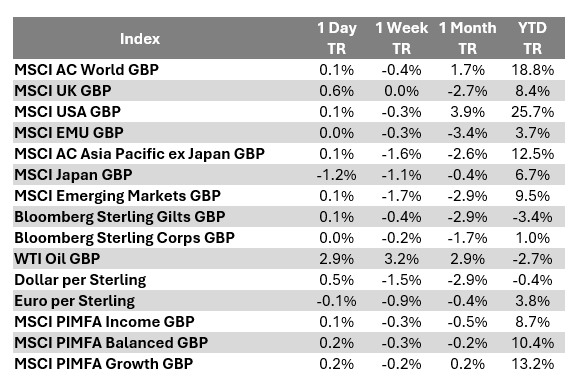

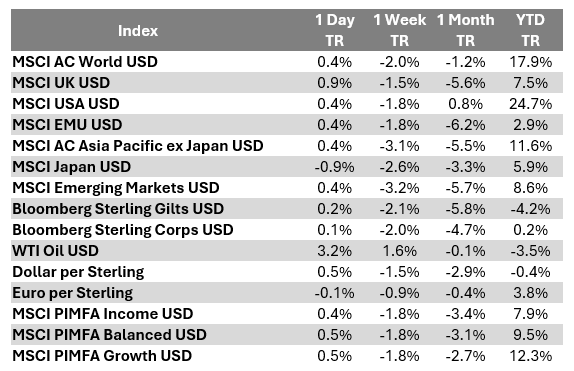

Investing implications

UK markets have shown a mixed response to the Budget, with investors carefully analysing the key announcements on tax policies, public spending, and economic growth measures. UK government bond markets initially appeared to react positively to the Budget announcement. Although, through the course of Wednesday, the day’s gains in gilt prices unwound.

That fluidity in bond market price action underscores the sensitivity with which markets are judging government efforts to manage the public finances. The key takeaway is that there remains a degree of concern around the potential effects of government borrowing and its implications for inflation and interest rates going forwards.

Meanwhile, in equity markets, perhaps the most notable moves today have been centered around smaller companies. Specifically, the UK’s Alternative Investment Market (AIM) equity index saw strong gains following the Budget, as the Chancellor’s move to apply a 50% relief from inheritance tax for AIM shares is better than some expectations had feared.

Businesses to shoulder the majority of the £40 billion tax rises

The sweeping tax reforms, aimed at supporting wealth creation for working people and fostering economic growth, mark the largest tax increases in decades at £40 billion of tax rises. Key measures affecting businesses include a 6.7% rise in the minimum wage and raising an expected £25 billion from an increase in employers’ National Insurance contributions.

The increased National Insurance rates are expected to hit small businesses hard, potentially leading to reduced staff, shorter operating hours, or even closures due to their limited ability to absorb increased costs.

However, in a measure to help small businesses Reeves unveiled an increase to the Employment Allowance from £5,000 to £10,500, which allows eligible employers to reduce their national insurance liability. This means 865,000 employers won’t pay any national insurance at all next year, and over one million will pay the same or less as they did previously.

Comment

I’ve read a lot of content and just spent 1.5 hours on a post-Budget technical webinar, the first of four over the next few days.

Now I understand more of the detail, and the proposed changes being consulted on, I’ve got a better view. This is a fairly typical ‘tax and spend’ Labour Budget. That is as anticipated, I’m just disappointed that growing the UK economy was not their main focus. Forecast growth is minimal. We really do need to grow our economy, this is the only viable option.

With regards to the changes on pensions and inheritance tax, we need more detail. This legislation won’t be implemented until April 2027. We will have time to consider it and alter course, change strategies.

For now, we need to wait for more information.

Steve Speed

31/10/2024