Please see below article received from Brooks Macdonald this morning, which provides a global market update for your perusal.

What has happened

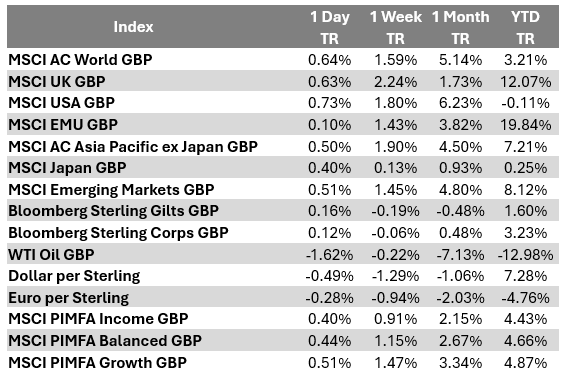

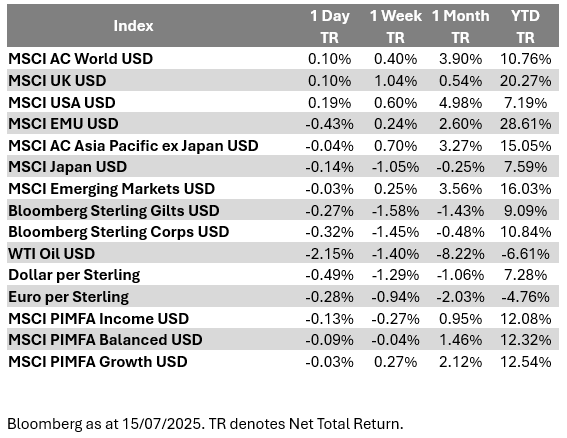

Markets yesterday proved once again that they are sensitive to the latest twists and turns in tariff news. With US President Trump late in the day yesterday saying that on tariffs he was “always open to talk”, that proved enough for markets in afternoon trading to edge higher. The US S&P500 equity index finished up +0.14% yesterday to close within 0.2% of last week’s record high, while closer to home the UK FTSE100 equity index gained +0.64% to notch up a fresh record high, all in local currency price return terms.

Mixing tariffs and geopolitics

US President Trump arguably broke new ground yesterday, mixing tariffs with geopolitical deadlines. Trump said yesterday that as well as resuming supplies of US-made Patriot air-defence missiles and other weapons to Ukraine, the US would impose “secondary tariffs” of 100% on countries doing business with Russia unless Russia agreed to a ceasefire within 50 days. While thin on details, it appears that the planned action by Trump would effectively represent additional levies on countries (such as India and China) that buy, amongst other things, oil from Russia.

Gauging Trump’s tariff impact

Today provides another opportunity to gauge what impact Trump’s tariffs are having on both the economy and corporate profits. Later today, we get the most recent monthly Consumer Price Index (CPI) reports from the US and Canada, as well as the calendar Q2 corporate earnings results season kicking off led by the biggest US bank JP Morgan’s results (JPM’s numbers are due out before today’s US market open). On the US inflation front specifically, if the US CPI print is higher than expected (Bloomberg’s consensus estimate is for a US annual all-items CPI rate of +2.6% and a core ex energy and food rate of +2.9%), that could derail US Federal Reserve (Fed) interest rate cut hopes – currently markets (implied from US Fed Funds Futures derivative contracts) are pricing in close to two lots of 25-basis-points of interest rate cuts by December.

What does Brooks Macdonald think

US President Trump yesterday showed that that he is willing to broaden his use of tariffs. Up until now, tariffs have been rationalised by Trump as a means to correct perceived trade unfairness and imbalances. Yesterday saw geopolitics added to the mix, with Trump threatening secondary tariffs on countries that buy from Russia. While this might force Russia to the negotiating table, in doing so it might further cement tariffs as a policy tool that Trump can use across a wide range of other policy ambitions that we have yet to see – as such, tariff policies and tariff uncertainty, even if just a negotiating tactic, could be something of a long-term feature of Trump’s presidency that investors will have to get used to.

Please check in again with us soon for further relevant content and market news.

Chloe

15/07/2025