Please see below, Brooks Macdonald’s ‘Daily Investment Bulletin’ which provides a brief analysis of the key factors currently affecting global markets. Received this morning – 19/01/2024

What has happened?

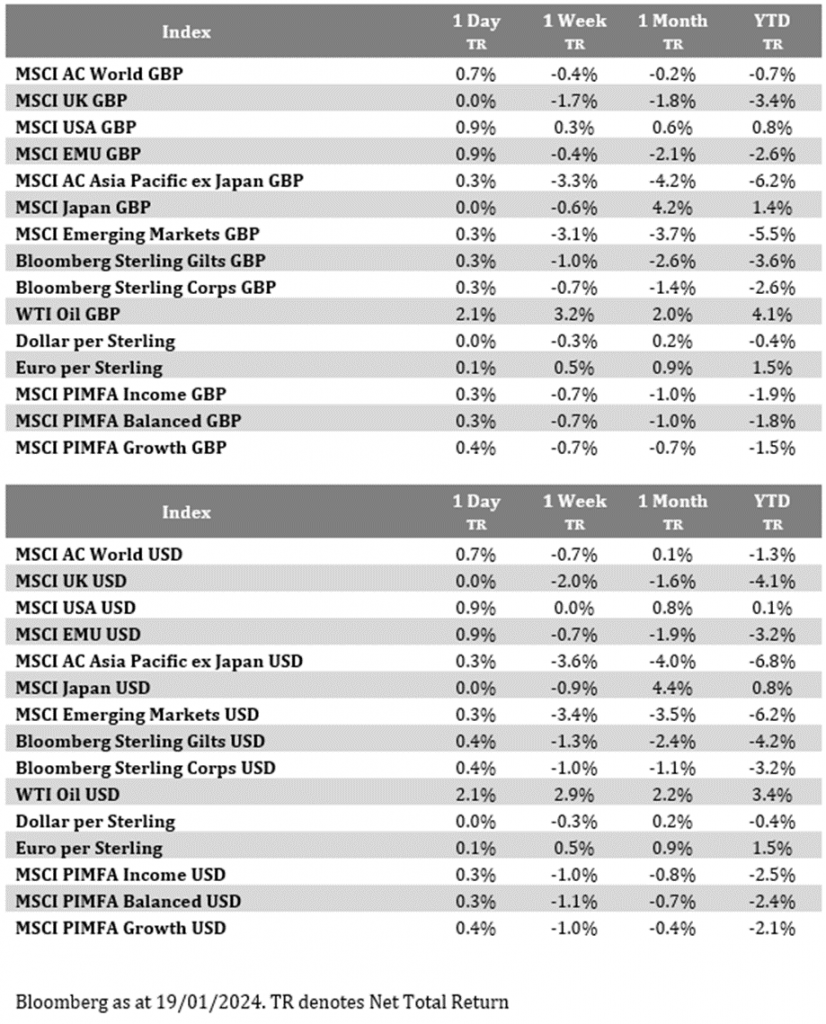

Equities saw a rebound yesterday as technology shares rallied in light of a positive 2024 outlook from chipmaker heavyweight, TSMC. The American Depository Receipts, which seek to track the share price of foreign listed companies, of TSMC rose by almost 10% yesterday. European equities also participated in this rally, rising over half a percentage point. This stock specific news helped buoy equity markets but the overall tone in bond markets remained downbeat as the interest rate cut narrative wilted in the face of further strong US economic data.

US economic data

The weekly initial jobless claims, which continue to help drive week-by-week sentiment, were stronger than expected with just 187k unemployment filings, versus the 205k expected. The 4-week average, which smooths out some of the larger moves, fell to the lowest level since February 2023 so it appears that labour market tightness is still a feature of the economy. After this data, the US 10-year Treasury yield continued to rise, hitting a one-month high of 4.14%. Longer dated bonds also moved in sympathy with the US 30-year Treasury up to 4.37%, the highest level in 6 weeks. Europe was not immune, with 10-year bund yields also rising on the day.

ECB

With the next ECB meeting less than a week away, the market has been focusing on the path of European interest rates. Yesterday saw the release of the December minutes which echoed the recent concern from ECB speakers that the de facto loosening of conditions caused by market interest rate cut expectations, is premature. The minutes that said ‘concern was expressed that the sharp market repricing threatened to loosen financial conditions excessively, which could derail the disinflationary process.’ The ECB appear to be committed to seeing disinflation embedded before endorsing the market’s pivot.

What does Brooks Macdonald think?

US political risk will start coming into the frame as the year continues and the US Presidential race hots up. Yesterday saw the US government avoid a partial government shutdown after a stopgap bill was approved. The can has been kicked down the road until March in order to allow lawmakers to agree to a politically contentious long term funding bill. Congressional leaders will be hoping to avoid several short-term bills as it increases the risk of a long-term bill being negotiated during the Q3 where the political pressure will be greatly heightened.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Alex Kitteringham

19th January 2024