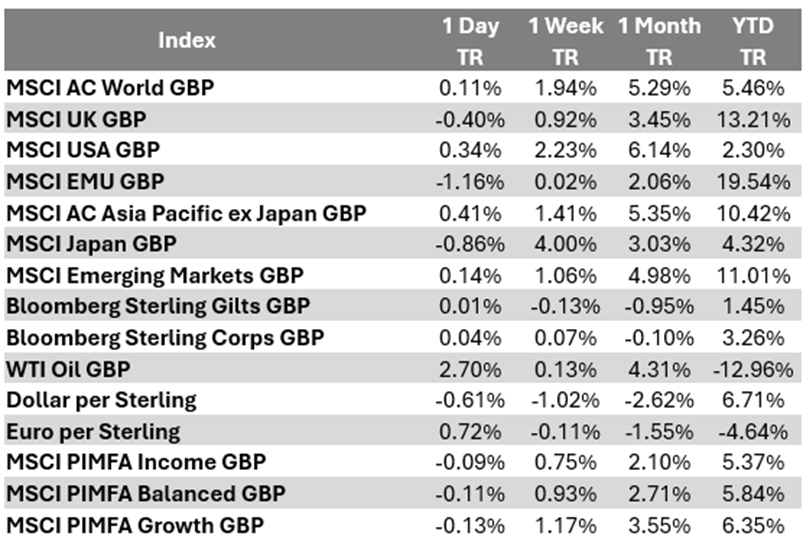

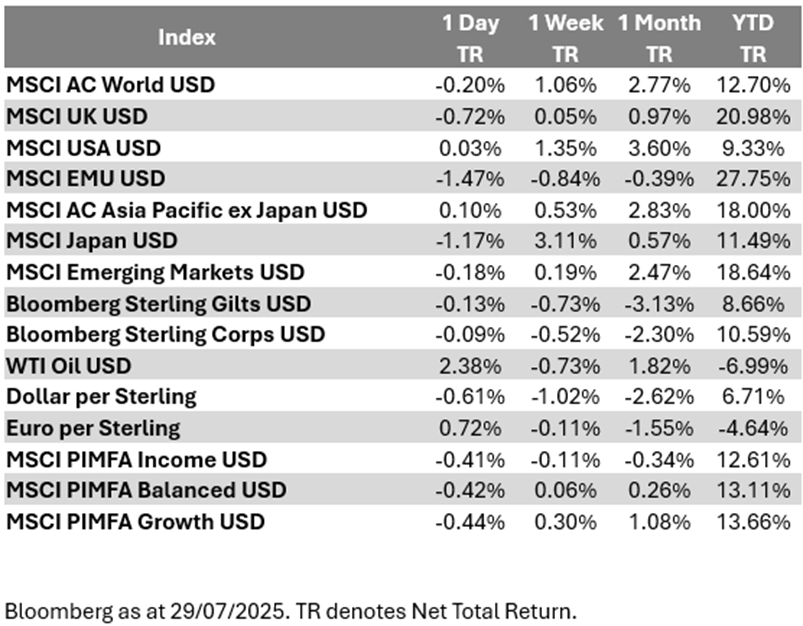

Please see below article received from Brooks Macdonald this morning, which provides a global market update for your perusal.

What has happened

Yesterday saw US and European equity markets largely unwind their earlier intraday-gains as investors focused on negative ramifications from the US-European Union (EU) trade deal that was announced over the weekend. The share prices of German auto makers, which are especially sensitive to US trade access, reflected the evolving investment mood that the EU had struck a weak deal: Volkswagen shares, which had surged over +3% in the opening minutes of yesterday’s session, ended up closing more than -3.5% down by the end of the day (all in local currency terms).

US-EU trade deal criticised

As we noted in our Daily Investment Bulletin yesterday, the 15% tariff rate that will now apply to most EU trade going into the US is significantly higher than the average trade-weighted pre-existing US tariff rate of under 2%. While European Commission President von der Leyen had previously conceded the deal “was the best we could get”, yesterday saw French Prime Minister (PM) Bayrou label it “a dark day” and a “submission” for the EU, while Hungarian PM Orbán called von der Leyen a “featherweight” negotiator, adding “[US President] Trump ate von der Leyen for breakfast’.

US Federal Reserve meets

Yesterday sees the US Federal Reserve (Fed), arguably the world’s most important central bank, kick off its latest two-day policy meeting. The Fed announcement on interest rates is due out 7pm UK-time tomorrow evening, with a press conference starting 7:30pm UK-time tomorrow. While no change in interest rates is expected (the Fed’s benchmark interest rate target range of 4.25-4.50% has been unchanged so far this year), markets will instead be on the lookout for any signalling around possible interest rate cuts later this year, not least given the huge pressure that Trump has put on Fed Chair Powell recently to cut interest rates.

What does Brooks Macdonald think

It is a big week for stock markets, with a lot riding on the latest US megacap technology results in particular. Microsoft and (Facebook parent company) Meta have results tomorrow, while Apple and Amazon results are on Thursday, all coming out after the US trading close on each day. High hopes for Artificial Intelligence has powered broader US and global equity index performance so far this year, but with the aforementioned four megacap tech stocks currently accounting for around a fifth of the market-capitalised weight of the US S&P500 equity index, there is significant near-term two-way performance risk.

Please check in again with us soon for further relevant content and market news.

Chloe

29/07/2025