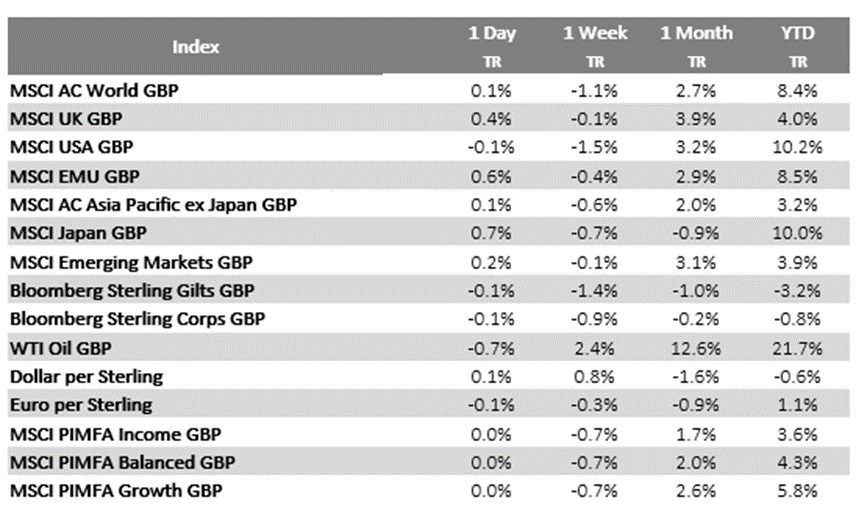

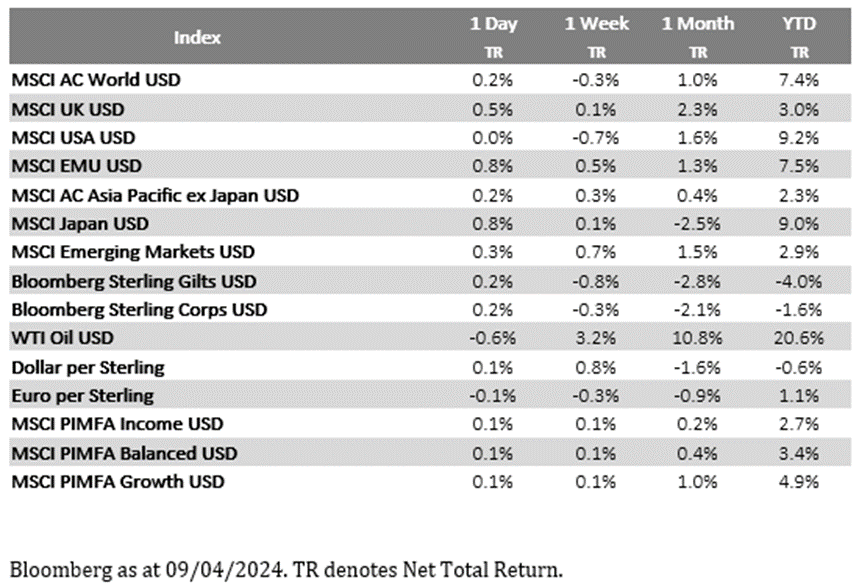

Please see below article received from Brooks Macdonald this morning, which provides a global market update for your perusal.

What has happened

Government bond pricing in both the US and Europe fell back (with bond yields rising) on Monday, as markets moved to cut hopes for the number of interest rate cuts this year. For context, at the start of the year, markets were pricing in more than six quarter-percentage-point cuts this year from the US Federal Reserve (Fed) – on Monday, this number was standing at less than three. Adding to the latest shift in view, US bank JPMorgan CEO Jamie Dimon said in his annual letter to shareholders, that the US economy “is being fuelled by large amounts of government deficit spending and past stimulus … this may lead to stickier inflation and higher rates than markets expect.” Staying with inflation, ahead of tomorrow’s US consumer inflation data, yesterday we got the latest New York Fed Survey of Consumer Expectations – to be fair it showed a bit of a mixed picture on inflation expectations, though the good news is that 5-year expectations fell by -0.3% points on the previous month, down to +2.6%,

Markets now fully pricing in just two rate cuts from the Fed

Market confidence around the number of interest rate cuts out of the Fed looked to wane further on Monday. Verus the Fed’s ‘dot plot’ of its members which showed last month a median expectation of three quarter-percentage-point cuts this year, markets on Monday moved to price in 61.5 basis points (bps) of cuts by the Fed’s December 2024 meeting, a fall of -3.3bps on the previous day – it implies that only two 0.25% rate cuts are currently being fully discounted.

Middle East tensions take a breather, but China fills the geopolitical gap

Oil prices saw a modest dip down from a five-month high on Monday after Israel said it would remove some troops from Gaza, helping to cool some of the previous week’s geopolitics-led gains. Instead, China looked to be filling the geopolitical gap on Monday- it emerged that US President Biden is expected to warn China about its increasingly aggressive activity in the South China Seas later this week during planned summits with Japan and the Philippines. According to newswires yesterday, a senior US official was quoted as saying that “China is underestimating the potential for escalation … China needs to examine its tactics or risk some serious blowback.”

What does Brooks Macdonald think

There is debate currently as to whether we might see some interest rate policy divergence between the Fed and the European Central Bank (ECB). In the case of the Fed, the probability of an interest rate cut by the US central bank’s June meeting is down to just 52% currently (the lowest since October last year), and the total number of Fed cuts priced by the December 2024 meeting is now just 61.5bps. Contrast that with the ECB where the probably of a cut by June is higher at 91% currently, and the total number of cuts by December 2024 is also higher at 80.5bps currently. All in all, it points to a contrast in the differing economic backdrops with the US showing relatively stronger economic growth currently, but with it, the risk of relatively stickier inflation as well.

Please check in with us again soon for further relevant content and market news.

Chloe

09/04/2024