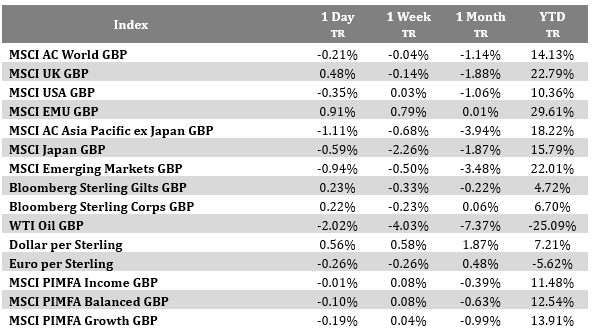

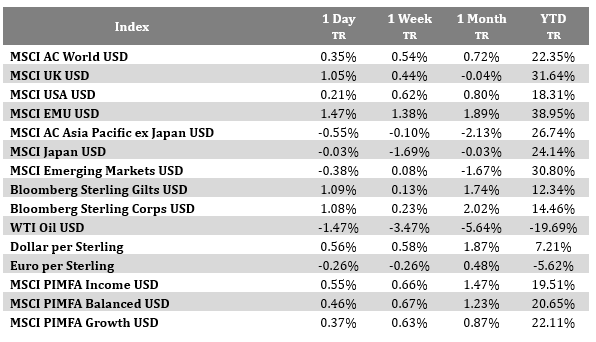

Please see below, Brooks Macdonald’s Daily Bulletin which focuses on the US equity market and today’s data release for UK growth. Received today – 12/12/2025

What has happened?

The headline event yesterday centres around the US equity market again hitting new highs. The S&P 500 rose 20bp on the day pushing it through the 6900 level. This though masks a continued pick up in volatility within stocks related to the AI theme. The market is beginning to differentiate more and more on perceived winners and losers rather than a “rising tide lifts all boats” mentality. We touched on the disappointing results from Oracle yesterday, and the softness in their share price continued to weigh on the sector throughout the trading day. In addition, we had results from Broadcom, a company that has very much increased its stature within the AI cohorts of stocks this year. Initial earnings releases showed current quarter revenue guidance ahead of expectations, causing their share price to rally c.4% initially. However, failure to give further guidance for the next 12 months, specifically around AI revenues saw the shares flip over 8% to be down c.4.5%. This volatility in the tech sector is likely to continue into 2026 as markets digest the outcomes from the lofty capex spend firms are undertaking.

UK Growth disappoints (again)

The Office for National Statistics this morning released October GDP data showing a 0.1% decline, repeating the previous months decline. This is in fact the 4th monthly reading in a row where no growth has been logged. Many economic forecasters were expecting a slight tick up of 0.1%. Given the uncertainty in the run up to the November budget it is probably not surprising that the data was on the weaker side. The GDP figures are the first in a run of data that sets the stage for the BOE’s final meeting of the year on December 18th. Policymakers, heading into what’s expected to be a knife-edge call on a rate cut, will get fresh jobs and inflation readings in the days leading up to that meeting.

Brooks Macdonald’s thoughts

Whilst the momentum behind the AI trade has been a major force during 2025 the last few weeks has seen the market recalibrate and become more discerning within the theme. We still believe this is a multi-year structural theme but investors will have to be more selective in asset or stock selection, particularly as we are yet to see the outcomes from the interplay of the huge amounts of capital expenditure within the sector. Volatility will remain within this space as the market reacts to perceived winners and losers of the AI theme.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Alex Kitteringham

12th December 2025