Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 31/03/2026.

Economic uncertainty continues amid Iran war

With inflation above target and limited fiscal room, policymakers face tough choices ahead.

Key highlights

- Mixed signals over the Iran war: Contradictory statements coming from the U.S. and Iran, along with the capricious nature of President Trump, continue to make it challenging to predict outcomes in the Middle East.

- The economic impact is yet to be fully felt: Anticipated inflationary pressures and predictions of interest rate rises are set against a backdrop of general uncertainty and reduced opportunity for fiscal stimulus, leaving investors in something of a holding pattern until more clarity emerges.

- Input prices start to rise: Some indicators, most notably the purchasing managers indices, show that businesses are beginning to feel the pinch as the cost of inputs has started to rise, with a potential knock-on effect on outputs to follow.

The Iran war

The dominant theme of the last week was the Iran war and its far-reaching consequences for global energy markets, risk assets and central bank policy. Europe saw sharp equity declines as escalatory rhetoric from both Washington and Tehran rattled markets.

This followed President Trump issuing a 48-hour ultimatum, demanding the reopening of the Strait of Hormuz (the Strait) and threatening strikes on Iranian power plants. But markets rallied as this was later extended to a five-day deadline and subsequently a ten-day deadline, reflecting the president’s assertion that progress is being made in negotiations between the two parties. Iran, however, was characteristically defiant: issuing counterthreats targeting U.S. military bases, energy infrastructure of nations perceived to be assisting the U.S. war effort, desalination facilities and – notably – financial institutions holding U.S. Treasury bonds.

As the week progressed, a familiar pattern emerged: brief risk-on rallies on hints of diplomacy, followed by renewed pessimism as the facts on the ground failed to improve. Last Tuesday, President Trump posted a lengthy statement claiming “advanced negotiations” with Iran toward a “complete and total resolution of hostilities.” Iran’s foreign ministry acknowledged that messages had arrived via intermediary countries but denied any direct negotiation with Washington, stating that its stance on the Strait “has not changed.”

By last Wednesday, a 15-point plan had reportedly been transmitted via Pakistan, prompting a modest risk-on session. Iran eventually confirmed it had rejected a U.S. proposal. By Friday, the consensus among the geopolitical experts remained decidedly pessimistic regarding the scope for near-term de-escalation.

Helima Croft, Managing Director and Head of Global Commodity Strategy and MENA Research at RBC Capital Markets, noted that despite a minor uptick in vessels transiting the Strait, she doesn’t expect anything close to a normalisation of flows. The appointment of hardliner Mohammad Bagher Zolqadr, the former commander of the Islamic Revolutionary Guard Corps (IRGC), to head Iran’s Supreme National Security Council could signal a further coalescence within the regime around an uncompromising stance.

Helima Croft, Managing Director and Head of Global Commodity Strategy and MENA Research at RBC Capital Markets, noted that despite a minor uptick in vessels transiting the Strait, she doesn’t expect anything close to a normalisation of flows. The appointment of hardliner Mohammad Bagher Zolqadr, the former commander of the Islamic Revolutionary Guard Corps (IRGC), to head Iran’s Supreme National Security Council could signal a further coalescence within the regime around an uncompromising stance.

Escalation and leverage

A consensus exists among many observers that Iran does need to end the conflict, as it’s inflicting considerable pain on both the regime and the populace. However, the Iranian leadership wouldn’t accept a deal if they can avoid it, without first demonstrating their ability to inflict economic pain through their control of the Strait. The ability to frustrate that waterway would be the strongest means of discouraging further acts of aggression against the regime.

Historically, energy spikes and erratic acts by President Trump have been good entry points into markets ahead of what can be sharp rallies as conditions normalise. But the signs are not yet there that this is a great buying opportunity. While classic risk gauges such as the VIX have risen, they aren’t excessively elevated given the severity of the downside scenario – a possible sign that investors are reluctant to abandon their positions ahead of a possible rebound.

There are some lasting concerns too. Policymakers have significantly less bandwidth to provide support than in previous crises. Inflation has been above target in both the UK and the U.S. for approximately five years. Higher-for-longer energy prices risk de-anchoring inflation expectations, constraining central banks from easing even as growth deteriorates. There’s now an expectation that central banks will raise interest rates.

Meanwhile, elevated government indebtedness in many countries limits the scope for fiscal stimulus. In a recession, falling tax revenues and rising automatic stabiliser spending (welfare benefits) would compound the debt problem further. For now, back-channel talks continue with the hope of de-escalating the tensions.

Troop movements, however, suggest that the U.S. could be prepared to seize some territory (perhaps Kharg Island, through which most of Iran’s oil exports flow) or enriched uranium supplies, or to clear the coastal areas from threats to shipping. This could just be posturing, but recent history has suggested that troop movements do tend to precede deployments.

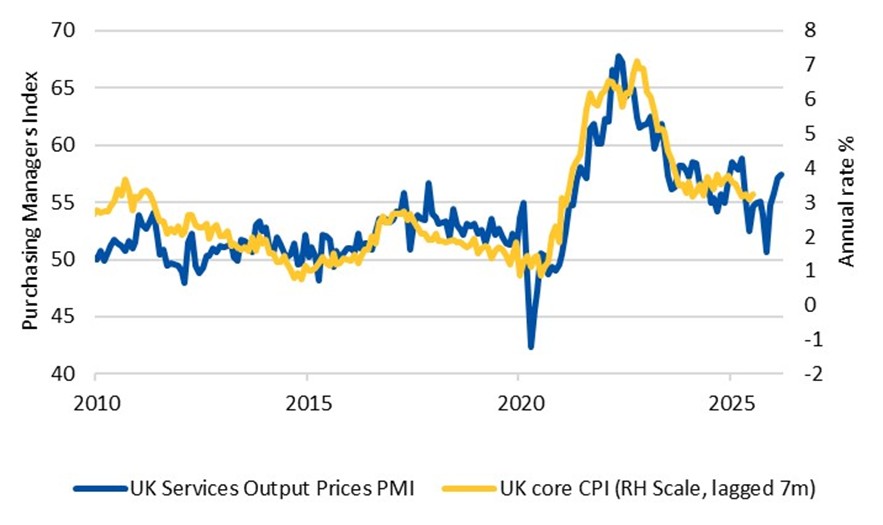

UK firms start to feel a costs pinch

European markets remain understandably pre-occupied by the Middle Eastern conflict, and specifically the impact on energy prices, which makes the UK’s official consumer price index statement seem less important overall. However, some data, such as the purchasing managers indices (PMIs), remain relevant.

Because they’re based upon companies’ surveyed responses since the outbreak of the conflict, the PMIs confirm that businesses are experiencing the fastest acceleration in input prices since 2023. This was most pronounced in manufacturing, but services output prices were affected too, although not enough to immediately offset the higher input costs.

The tone from policymakers has remained hawkish. Bank of England Chief Economist Huw Pill discussed how uncertainty shouldn’t be used as an excuse not to act to contain inflation. Fellow Monetary Policy Committee member Megan Greene discussed how there will be lasting inflationary effects from the conflict even in a “best-case” scenario.

More UK firms raised output prices in March

Source: Bloomberg

By contrast, Deputy Governor Sarah Breedon did acknowledge that second-round effects would be less likely now than in 2022, due to the weaker labour market. That is unquestionably true, but, having spent most of the last four years missing the inflation target materially to the upside, policymakers feel compelled to err on the side of the hawks.

Sectors to be impacted differently?

Throughout Europe, the pass-through of higher energy prices affects companies via changes in monetary policy and more directly as well. High bond yields mean lower real estate valuations as well as less deal flow, because the financing costs for new deals have risen. European real estate sector yields, which had fallen to their lowest since 2022, have risen to their highest since 2023.

Sectors such as consumer services and retail, on the other hand, will see less volume growth because of the real income compression from energy price inflation. Price earnings ratios are at the lower end of their range but don’t currently stand out.

All these factors combine to affect auto sales, where financing costs, running costs and general economic confidence are all relevant considerations.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Charlotte Clarke

01/04/2026