Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 09/06/2026.

Equity markets split as AI trade stalls

The AI trade, while powerful, is not immune to gravity and the broadening of market leadership is beginning to materialise.

Key highlights

- The polarity of equity markets: AI stocks, which rallied sharply in May, hit a speed bump last week on the back of disappointing tech industry earnings results.

- The wait in the Strait: Progress towards reopening the Strait of Hormuz stalled as Iran made an Israel-Lebanon ceasefire a condition for continuing negotiations.

- U.S. jobs growth beats expectations: The number of new jobs created in May was double expert estimates.

The polarity of equity markets

The first week of June was shaped by two forces pulling in different directions: a frozen geopolitical standoff that refused to thaw, and a sharp rotation within U.S. equity markets that reminded us how quickly sentiment can shift beneath the surface of headline indices.

The impact of high oil prices on the economy, and concerns that this could continue, have left investors struggling with where to allocate their savings, pensions, dividends and corporate buyback capital. The area of the equity market least affected has been AI stocks, which rallied sharply during May – creating a divided market.

Last week, that trend hit a speed bump. Stocks were already looking extended on Wednesday evening, when Broadcom reported results that were strong in absolute terms but merely met rather than beat expectations.

In a market that has been leaning heavily on the AI narrative, that disappointment was enough to trigger weakness across the Nasdaq. Capital rotated into healthcare and financials, nudging the Dow Jones, which is rich in those sectors, to a new record closing high. It was a useful reminder that the AI trade, while powerful, is not immune to gravity – and that the broadening of market leadership we’ve been hoping for is beginning to materialise.

Source: RBC Brewin Dolphin estimates

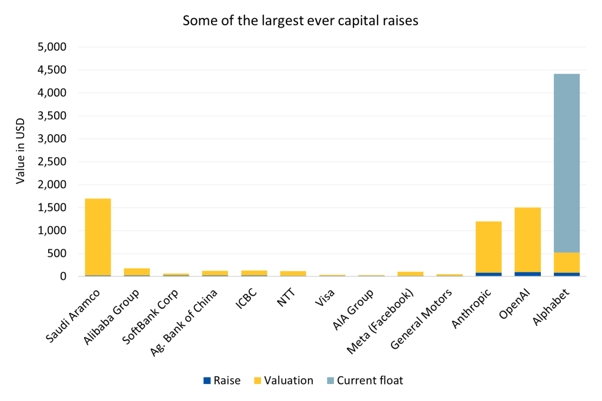

It also serves as a reminder that capital markets can be fickle, which is relevant as work continues on the blockbuster initial public offerings (IPO) planned for this year.

Perhaps opportunistically, Alphabet (which owns Google) used the accommodative market conditions to raise $85 billion of new equity. It’s a mere 2% of its $4 trillion market valuation, but enough to eclipse the mega IPOs still to come. Alphabet is specifically sneaking in ahead of other flotations over the coming weeks, taking advantage of the abundant liquidity environment.

Not everyone believes that environment will remain all year. Databricks confirmed that it won’t IPO this year because of the anticipated congestion from already planned issues.

One source of demand for these issues will come from tracker funds once they’re included within indices. S&P surprised the world by deciding not to update its index inclusion methodology. Nasdaq, by contrast, has fast-tracked inclusion and adopted an enhanced weighting to partially compensate for the low free float these companies will have at IPO.

The wait in the Strait

On the diplomatic front, progress towards reopening the Strait of Hormuz has stalled with the closure now approaching its hundredth day.

Iran pulled out of direct negotiations early last week, insisting on a resolution between Israel and Lebanon as a precondition. The U.S. duly brokered a ceasefire with Beirut, but Hezbollah rejected it, leaving the process stuck. By last Friday, there were no signs of meaningful progress.

What’s notable is how little this has moved markets. Brent crude oil held steady near $97.60 per barrel, and the broader ‘Gulf risk-off’ trade – higher oil, higher yields, weaker gold – flickered on and off through the week without gaining real momentum.

During the geopolitical stalemate, oil prices have settled into a predictable, elevated range of $90 to $100 per barrel. This is likely proving more uncomfortable for the 20,000 seafarers trapped in the Persian Gulf than it has been for investors. The high energy prices are unwelcome but no longer panic-inducing. Maintaining that level has been partly driven by the release of strategic reserves, and partly by economic measures that have been undertaken, particularly in emerging markets.

The other notable feature of the week’s Gulf inactivity is that President Donald Trump had a reportedly terse call with Israeli Prime Minister Benjamin Netanyahu. The call was in response to Iran’s demand that any reopening of the Strait of Hormuz would be conditional upon a ceasefire in Lebanon. Iran would seem to be a relatively tough negotiating partner.

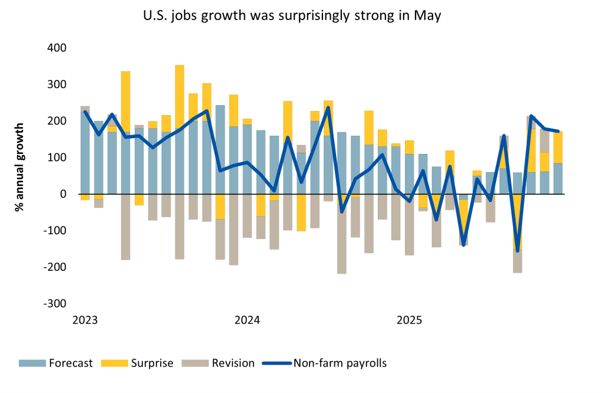

U.S. jobs growth almost doubles the forecast

Investors may be more focused on AI and geopolitics, but the economy is typically the most critical factor determining investment returns.

Expectations were modest for U.S. jobs growth given that consumers, who make up the largest share of economic growth, are under pressure from rising energy costs. An additional consideration is the larger structural risk to jobs stemming from AI. Thursday’s Challenger Jobs Report showed an accelerating trend of layoffs associated with AI.

Source: Bloomberg

As far as May was concerned, new jobs growth seems to have been very robust, coming in at 172,000 new jobs – almost double the consensus forecast. April’s jobs growth was also revised higher.

While there was no additional concern on wage growth, it still places pressure on the Federal Reserve (the Fed) to raise interest rates. There are two reasons for this: inflation remaining above target, and the robust labour market.

This pushed interest rate expectations higher, prompting a significant rotation away from the market’s former AI-related winners and back towards some of the previous laggards. The sell off seemed to be mostly a function of over-extended positioning rather than an obvious market top. We believe equity markets would be more susceptible to weak labour markets indicating weaker equity flows, than strong equity markets indicating higher interest rates.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Charlotte Clarke

10/06/2026