Please see the below article from Brooks Macdonald detailing their discussions on global markets. Received this morning 16/12/2025.

What has happened?

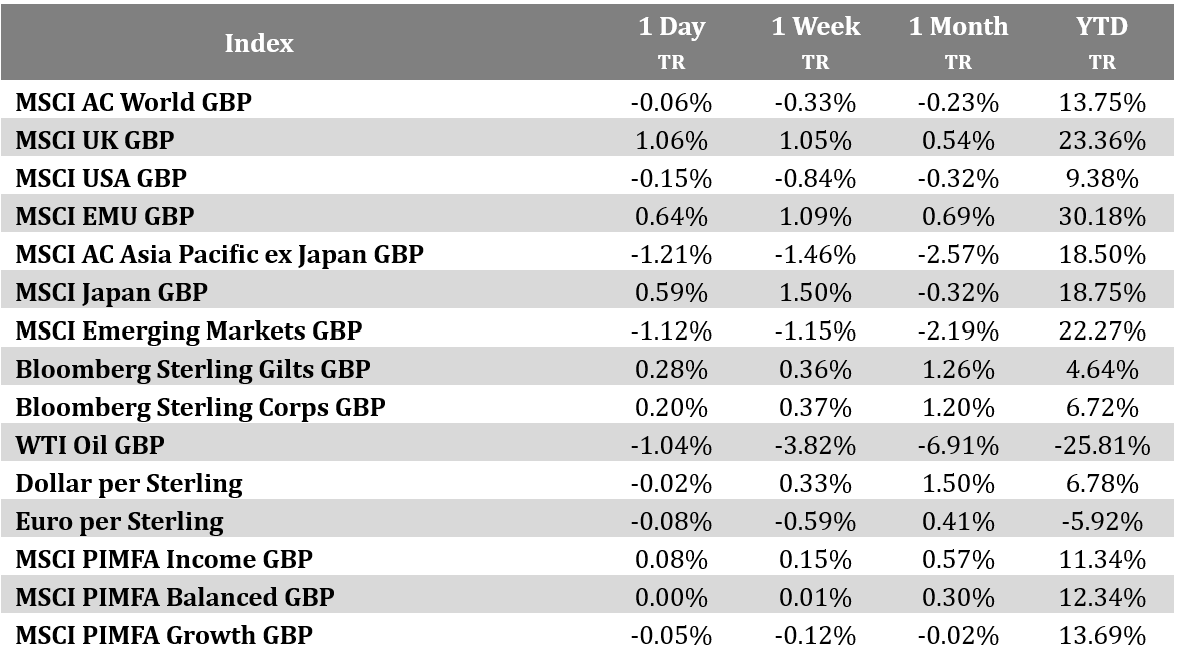

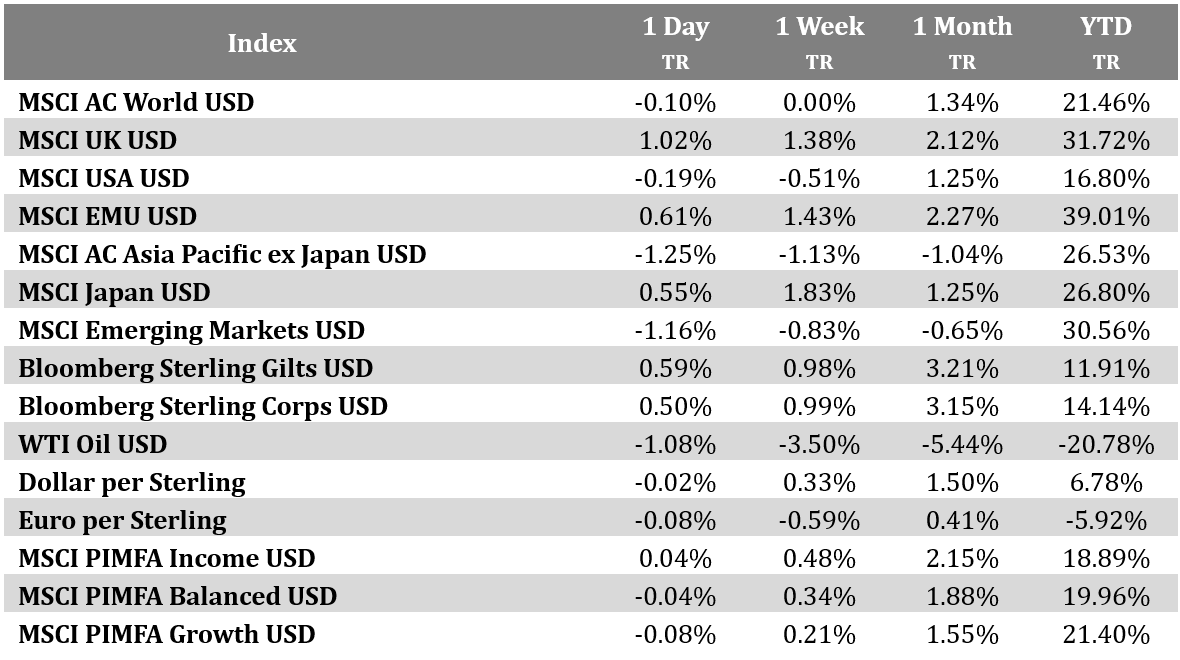

Yesterday saw divergent returns in European equities relative to US equities. European exchanges were buoyed by the positive rhetoric around the Russia/Ukraine conflict and a fall in energy prices (Brent crude oil closed at a 7 month low), whilst the US market was on the backfoot due to some softer economic data. Although most of the key data comes out from today, with the focus on the latest employment reports, the release yesterday of the Empire State manufacturing survey challenged sentiment. This lead indicator fell by more than expected to -3.9 in December (vs. 10.0 expected), which was beneath every economist’s estimate on Bloomberg. Asian markets are weak this morning. Indices that have the greatest exposure to Tech are seeing the biggest drops as nervousness around the AI theme persists, with the Hang Seng down -2.09%, followed by the KOSPI at -1.85%, and the Nikkei at -1.47%. Chinese markets, including the CSI (-1.41%) and Shanghai Composite (-1.25%), are also falling for a second day after yesterday’s weak November activity and real estate data releases.

Payrolls data in the US will be the focus

As noted yesterday today sees the beginning of a raft of data that may give investors and policy makers greater clarity on the state of the economy and hence policy as we move into the new year. The US employment report has not been available for several months due to the Federal Government shutdown and todays release may still be somewhat clouded by the fact that several of the recent monthly releases are not being referenced. Although we will get the payrolls numbers for both October and November, there’s only going to be an unemployment rate for November. What will be key is the markets interpretation of future policy as this will help shape sentiment – markets have been pricing 2 further rate cuts from US rate setters in 2026 with the expectation of a march easing gaining momentum yesterday on the back of the softer data.

What Brooks Macdonald think

We remain relatively optimistic but with a heightened degree of caution around our positioning in risk assets. Policy makers in the US, and the UK to some extent, are getting close to a point where late cycle economic data may determine further policy easing but this maybe offset by concerns around stickier price inflation, especially as the effects are Tariffs may begin to filter into the inflation data in coming months. Therefore we feel a prudent, selective and balanced approach to asset allocation is merited.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Alex Clare

16/12/2025