Please see below article received from Brooks Macdonald this morning, which provides a global market update for your perusal.

What has happened

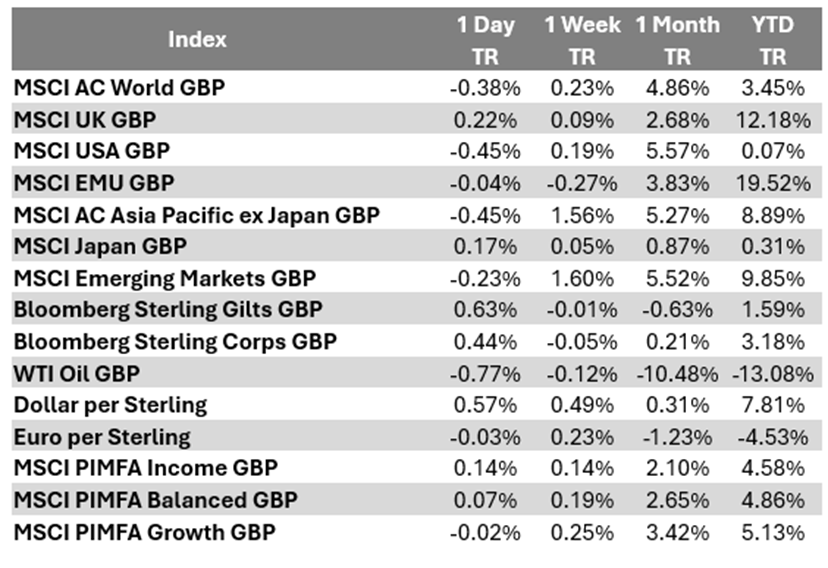

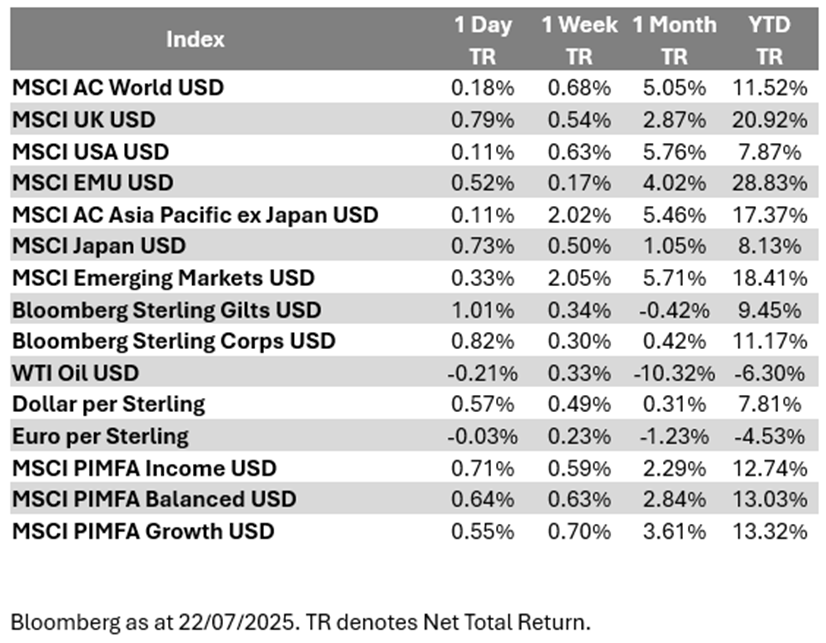

Global equity indices were up yesterday (in US dollar terms), once again led by mega-cap tech. While the day’s rally did fade a little at the end, Monday still marked fresh record closing highs for both the US S&P500 and tech-focused US Nasdaq equity indices. In contrast, this morning the UK FTSE All-Share equity index is struggling and UK government bond yields are up across the maturity curve, following a dire set of UK public sector deficit numbers – outside of the pandemic, last month was the highest net borrowing for a June month since records began in 1993.

EU trade-talks

With the 1 August tariff-pause deadline next week fast approaching, the lack of progress in European Union (EU)-US trade talks is becoming a concern. While talks are continuing this week, there is speculation that the EU are already planning retaliatory moves in case talks fall apart. Adding to tensions was a veiled threat from US Treasury Secretary Scott Bessent, who said yesterday “it doesn’t have to get ugly”, but “we are the deficit country, so the surplus country will always feel it more. We have a gigantic trade deficit with the EU, and so with the level of tariffs, it will affect them more”.

Middle East

News wires yesterday reported that Iran had agreed to hold talks with the UK, France and Germany to discuss Iran’s nuclear program, expected to take place this Friday in Istanbul, Turkey. However, there are low expectations for any meaningful progress. Ahead of those talks, Iranian officials are due to host a meeting with Russia and China representatives later today, while separately, Iran has yet to formally agree to fresh talks with the US.

What does Brooks Macdonald think

It is hard to argue with recent comments from US bank JP Morgan CEO Jamie Dimon that as regards tariff risks “unfortunately, I think there is complacency in the markets”. It is certainly impressive that global equities (in US dollar terms) are hitting record highs, while at the same time we are still yet to navigate a significant amount of near-term trade tariff uncertainty and risk. Should next week’s 1 August tariff-pause cliff-edge see talks with the EU and other countries unravel, it is not obvious that markets are greatly prepared for such an outcome.

Please check in again soon for further relevant content and market news.

Chloe

22/07/2025