Please see below article received from Brooks Macdonald this morning, which offers a global market update for your perusal.

What has happened

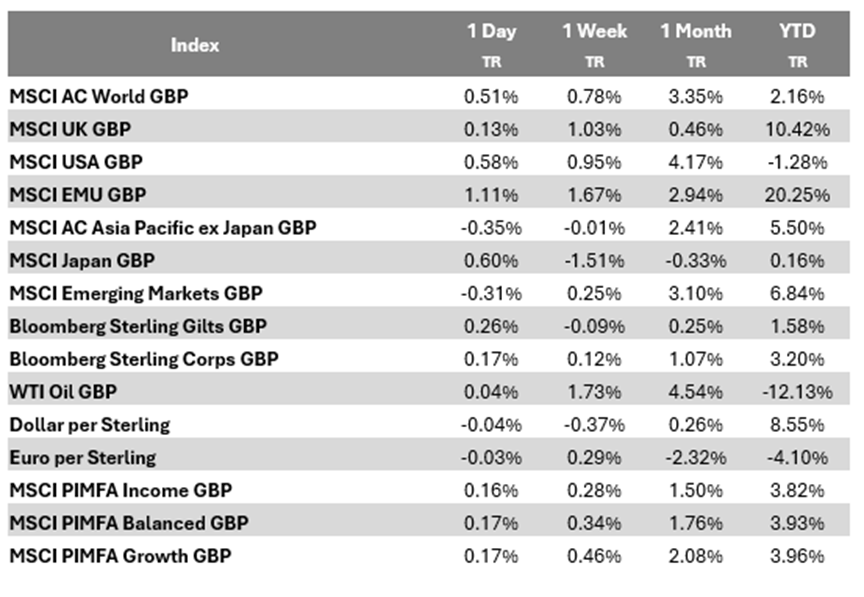

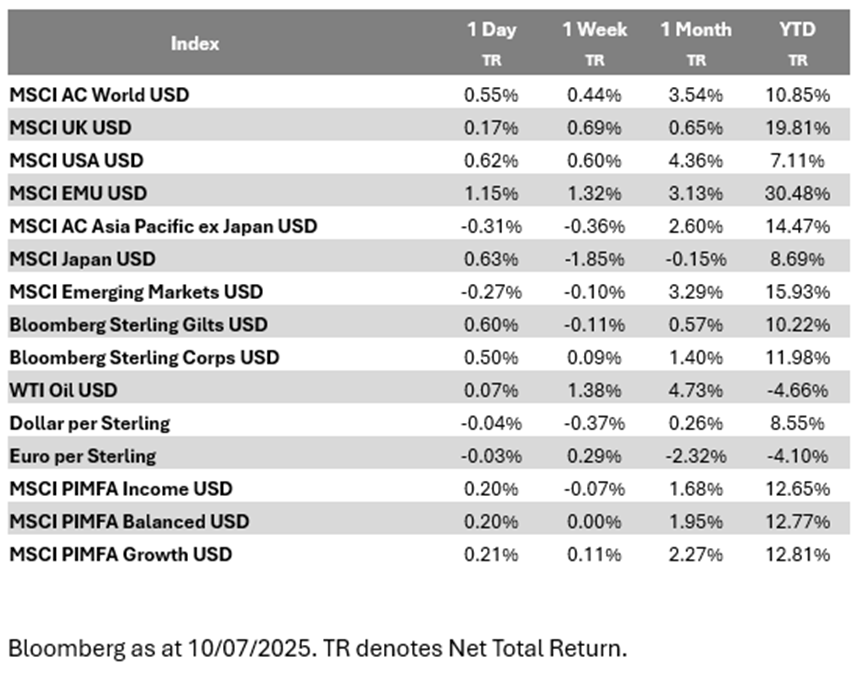

Markets had a good session yesterday, shrugging off August 1 tariff concerns. A tech-led rally pushed the S&P 500 (+0.61%) and NASDAQ (+0.94%) higher. The German DAX yesterday and the FTSE 100 this morning hit record highs. Notably, Nvidia (+1.80%) briefly topped a $4tn market cap, closing at $3.974tn. With everything else that is happening, AI remains the greatest hope for US exceptionalism to return. Falling bond yields eased fiscal worries, with the 10-year Treasury yield dropping -6.7 basis points after a strong auction, signalling robust investor confidence despite no clear catalyst.

Trump’s tariff developments

Yes, we have more tariff talks yesterday. President Trump unveiled a 50% tariff on copper imports starting 1 August, a big deal for industries relying on this metal. He also announced a 50% tariff on Brazilian goods, up from 10% on Liberation Day, escalating tensions with BRICS nations and weakening the Brazilian Real by -2.29%, its worst drop since early April. The Philippines got a 20% tariff, and other countries face varied rates, as Trump keeps the trade policy plot twisting.

Federal Reserve insights

The Fed’s June minutes, out yesterday, showed a split on policy and tariffs. A couple of officials hinted at a possible rate cut at the 29-30 July FOMC meeting if data supports it, while some see no cuts at all in 2025, noting the federal funds rate may be close to the neutral level. On inflation, some view tariffs as a one-off price bump, but most worry about longer term effects. This division echoes the ‘dot plot’ published last month: 10 of 19 officials expect two or more rate cuts this year, seven see none, and two predict one.

What does Brooks Macdonald think

The Fed meeting on 29-30 July, just before the 1 August tariff deadline, will see policymakers wrestling with trade levy uncertainties and their economic impact. With inflation’s path still unclear, the Fed is likely to hold steady on rates despite pressure from Trump for more aggressive rate cuts. In addition, oral arguments to the Court of Appeals on whether the International Emergency Economic Powers Act authorises the president to impose tariffs will be heard on 31 July, which adds another layer of complexity.

Please check in again with us soon for further relevant content and market news.

Chloe

10/07/2025