Please see below the Daily Investment Bulletin from Brooks Macdonald, which was received on 06/08/2024:

What has happened

What a difference 24 hours makes. The big takeaway coming into today’s trading session is that markets, for the time being at least, appear to have found their footing. This comes after markets over the past week hit by a triple whammy of weaker economic data, mega-cap US technology results disappointments, and the surprise interest rate hike out of Japan. Much of the rebound from yesterday’s lows is stemming from a better-than-expected US ISM (Institute for Supply Management) Services PMI (Purchasing Managers’ Index) which has in part pushed back some of the fear that the US economy was about to tip into recession. Arguably the epicentre for the wave of selling over the last few days, Japan’s TOPIX has this morning posted a gain for the day of +9.30% and has as a result pushing the index for the whole of 2024 to date back into positive territory (just) of +2.33%. Otherwise, the other news out overnight is that Australia’s central bank (the RBA), has left interest rates unchanged at a 12-year high (of 4.35%) for the sixth meeting in a row.

A better US services PMI pushes back on fears of impending recession

After the weaker US manufacturing PMI and weaker US non-farm payroll jobs data last week, the markets were desperate for good news. For near-term investor sentiment, coming to the rescue was yesterday’s US services PMI print. The July reading saw a rise to 51.4 from 48.8 in June (and better than the 51 expected). Importantly, it put the index into expansionary territory (over 50). Beneath the headline, the ISM employment sub-component saw a bounce up to 51.1 (against 46.4 expected) and reaching its highest level since September 2023. While the data also showed some degree of sustained inflationary pressure, with the ‘prices paid’ sub-component up to 57 (versus 55.1 expected), markets were yesterday understandably more focused on the economic growth side of the equation.

Latest US Fed survey on credit conditions sees continued improvement

Also supporting a more constructive picture yesterday was the latest (calendar-quarterly) US Federal Reserve Senior Loan Officers’ Opinion Survey (SLOOS). While credit standards for commercial & industrial loans were still tightening, they were doing so at their slowest pace for 2 years, since Q2 2022, while standards for mortgages moved back to neutral. Reflecting the more market-friendly nuance, the US S&P500 banks sector index marginally outperformed the wider market yesterday. Historically, there is quite a good correlation between the SLOOS and trailing 12-month corporate earnings growth, so as the SLOOS continues to see a turn away from relatively tighter credit conditions, so this might bode positively for the earnings picture more broadly.

What does Brooks Macdonald think

Yesterday’s wild swings in markets has seen volatility return with a vengeance. At one point intraday yesterday, the so-called ‘fear gauge’ (the VIX index which measures the volatility of the US S&P500 equity index) was trading at 65.73, up 42.34 points and up +181% from Friday’s close. To put that in context, the largest full day move since the VIX index was first calculated back in 1990 was the 21.57-point increase on 12 March 2020 at around the time of the initial Covid-19 wave. After yesterday’s part-recovery in investor sentiment, last night the VIX index closed at 38.57. Whether the latest 24hours marks a slow return to some degree of relative market calm, or whether it is just the opening bout of more volatility to come, it is impossible to say. However, what we do know is that, as we said in our recent July edition of our Quarterly Market Overview, in an uncertain world, diversification remains key, enabling us to position our asset allocation settings for more than just one central forecast economic and market scenario.

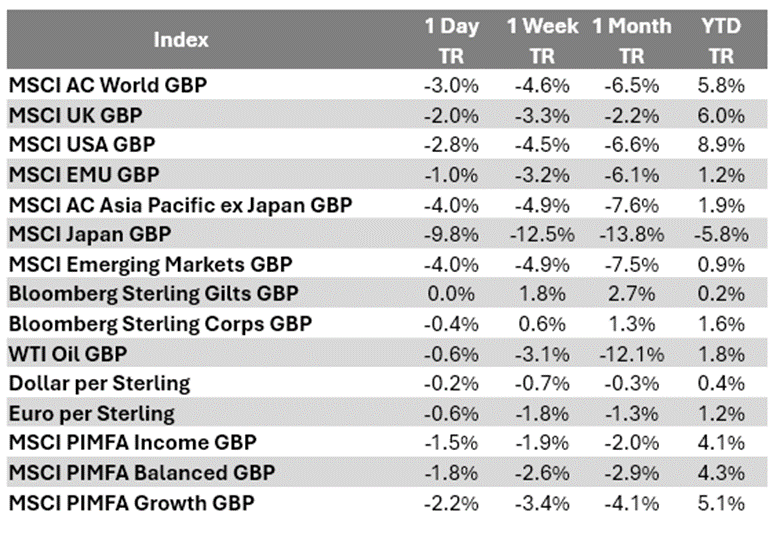

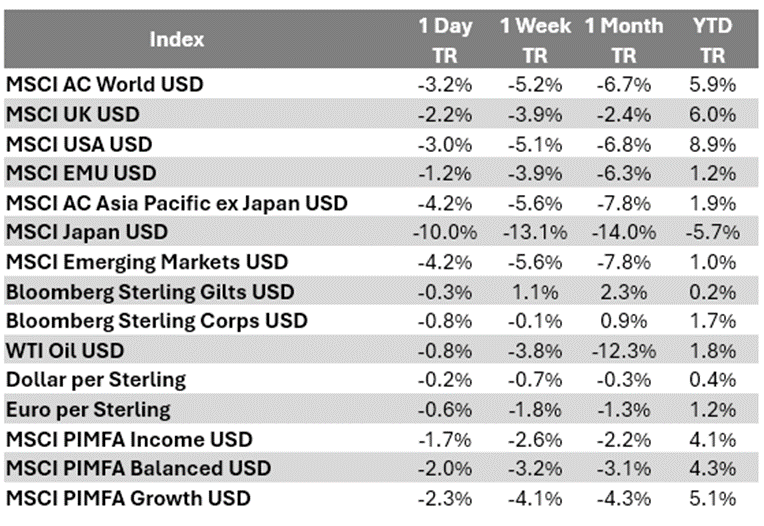

Bloomberg as at 06/08/2024. TR denotes Net Total Return.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Charlotte Clarke

06/08/2024